A Guide to Cash Flow Real Estate for Investors

- Ryan McDowell

- Sep 3, 2025

- 11 min read

Reading Time: 8 min | Good for: Novice Investors (A), Family Offices (B)

TL;DR: The Bottom Line on Cash Flow Real Estate

Cash flow is king. It's the net profit left after all expenses and mortgage payments are made, providing a reliable income stream and a buffer against market downturns.

Metrics matter. Net Operating Income (NOI), Cash-on-Cash Return, and Debt Service Coverage Ratio (DSCR) are the core metrics that reveal a property's true financial health and its appeal to lenders.

Today's market favors cash flow. With new construction slowing, particularly in multifamily housing, existing properties are well-positioned for strong rental demand and occupancy, directly boosting income potential.

Maximizing returns is an active process. The best operators increase cash flow by both driving revenue (strategic upgrades, ancillary income) and cutting expenses (tax appeals, energy efficiency).

The next step. For accredited investors, understanding these principles is the first step toward building a resilient portfolio. The next is finding a sponsor who lives by them.

At its core, cash flow real estate is simple: it’s an investment property that brings in more money from rent than it costs you to own and operate. That difference is your net profit, and it's the tangible, spendable proof that your asset is truly working for you. Think of it as the financial heartbeat of a healthy real estate portfolio.

The Foundation of Durable Wealth

For sophisticated investors and family offices, chasing cash flow isn't just a strategy—it's the foundation for building durable, long-term wealth. Unlike market appreciation, which is the unpredictable rise in a property's value, cash flow isn’t speculative. It's a reliable, consistent income stream that delivers immediate returns while acting as a powerful buffer against economic swings.

While the thrill of a big sale is hard to deny, disciplined investors know that appreciation is the bonus, not the main event. Consistent positive cash flow is the engine that keeps a portfolio running. It lets you cover all your expenses, build up reserves for the next great opportunity, and take distributions without ever being forced to sell.

Why Cash Flow Is a Critical Metric

If you want to understand the true health of a real estate investment, you have to look at its cash flow. It cuts through all the market noise and gives you a clear, unvarnished picture of how the asset is actually performing.

Financial Stability: Positive cash flow means the property pays for itself. The mortgage, taxes, insurance, and maintenance are all covered without you ever needing to reach into your own pocket.

Risk Mitigation: When the economy takes a downturn and property values flatten out or even dip, a cash-flowing asset keeps generating income. That's what protects your investment from distress.

Proof of Concept: It proves you made the right call. When a property generates positive cash flow, it’s confirmation that your analysis of rents, expenses, and market demand was spot-on.

The Current Market Advantage

In today's economic climate, focusing on cash flow has become more important than ever. The current market dynamics are creating compelling openings for investors who prioritize income-producing assets.

Market Signal Box (Data as of Q1 2024) The Data: Projections for 2024 show a stunning 30% year-over-year drop in new multifamily housing deliveries, according to data from RealPage. This slowdown in construction, driven by higher financing costs and economic uncertainty, is creating a supply crunch in many markets. Investor Take: With less new competition, well-located existing properties can command strong rents and maintain high occupancy. This supply-demand imbalance is a direct driver of robust, reliable cash flow for disciplined investors. You can read more about the new economy of real estate investing.

How to Calculate Real Estate Cash Flow

Moving from an idea to a spreadsheet is where a deal's true potential—or its hidden flaws—comes to light. Mastering the math behind cash flow real estate is non-negotiable for any serious investor. It's how you transform abstract opportunities into concrete financial projections.

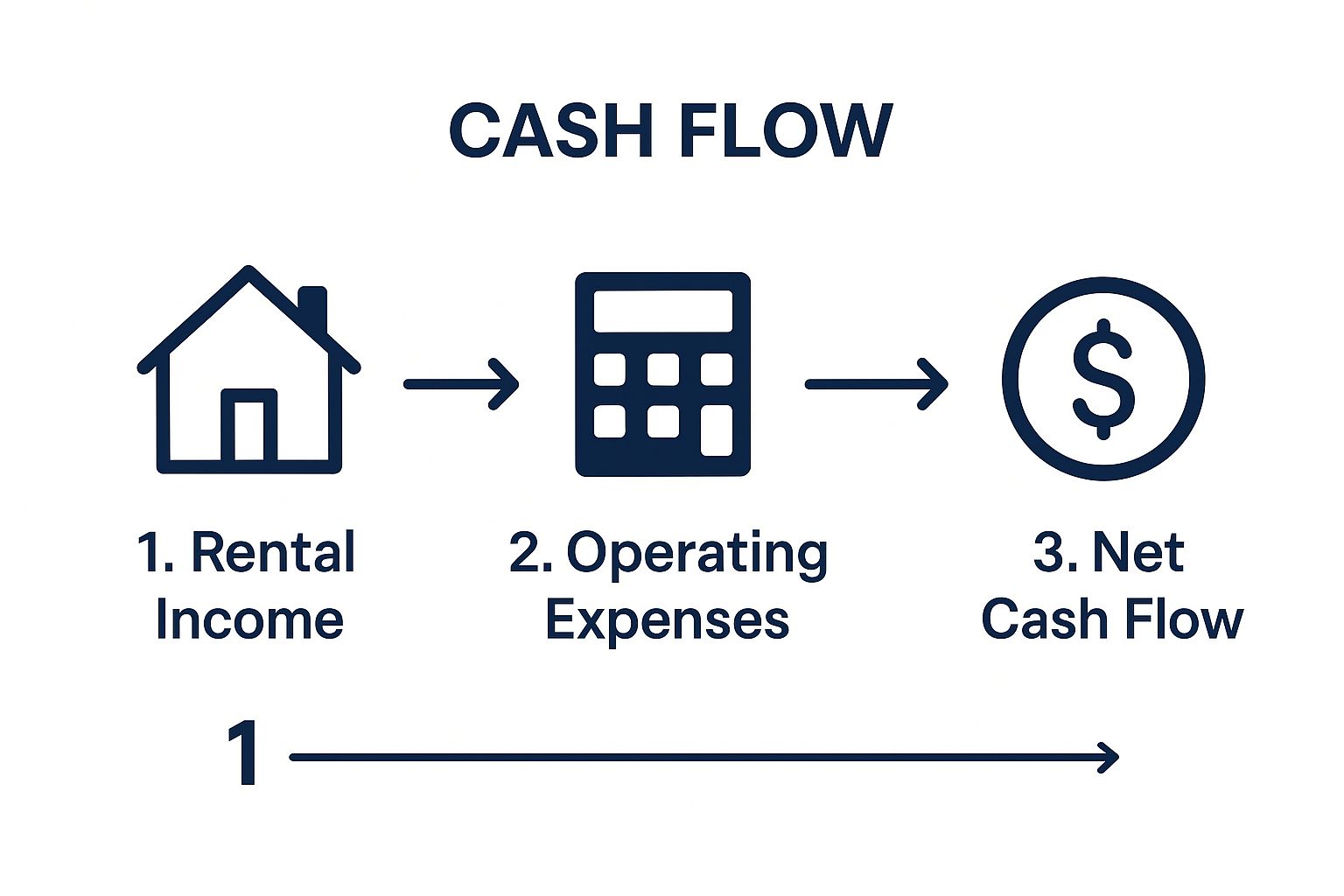

The process is essentially a logical waterfall. You start with the absolute most a property could earn, and then you systematically subtract the real-world costs to land on that final, all-important number: the cash in your pocket.

This diagram shows the three core stages, walking you from top-line income down to your net cash flow.

As you can see, each step sharpens the financial picture by factoring in the realities of owning and operating a property. Let's break down each stage with a practical example.

The Cash Flow Waterfall Step-by-Step

Think of calculating cash flow as a simple subtraction problem with a few key milestones. It all begins with what the property could make in a perfect world, then gets real by deducting the actual costs of running it.

Start with Gross Potential Income (GPI): This is the maximum rental income your property could generate if every single unit were rented for the entire year at the full market rate. It's your ceiling.

Account for Vacancy and Credit Loss: Reality check—no property stays 100% occupied forever. This line item accounts for the inevitable gaps when units are empty between tenants or when someone fails to pay. A standard assumption is often 5-10% of GPI.

Determine Effective Gross Income (EGI): Subtract those vacancy losses from your GPI. Then, add any other miscellaneous income (think parking fees, laundry machines, or pet fees). This gives you the EGI, a much more realistic picture of your annual revenue.

Subtract Operating Expenses (OpEx): These are the unavoidable, day-to-day costs of keeping the lights on and the property running. This includes property taxes, insurance, management fees, utilities, and routine maintenance.

Calculate Net Operating Income (NOI): EGI minus OpEx equals your NOI. This is a critical metric because it shows you the property's raw profitability before you factor in any loan payments.

Deduct Debt Service: This is simply your total mortgage payment for the year (which includes both principal and interest).

Arrive at Net Cash Flow: NOI minus Debt Service is your final Net Cash Flow. This is the money that actually hits your bank account. It’s the profit.

An Example: A 10-Unit Multifamily Property

To make this tangible, let’s run the numbers for a hypothetical 10-unit apartment building where each unit rents for $1,500 per month. Here's how the waterfall calculation plays out, turning our assumptions into a clear financial snapshot.

Illustrative Cash Flow Calculation for a 10-Unit Multifamily Property

Metric | Calculation/Note | Annual Amount |

|---|---|---|

Gross Potential Income (GPI) | 10 units x $1,500/mo x 12 months | $180,000 |

Less: Vacancy Loss | 5% of GPI, a typical market assumption | ($9,000) |

Effective Gross Income (EGI) | GPI - Vacancy Loss | $171,000 |

Less: Operating Expenses (OpEx) | Assumed at 40% of EGI (taxes, insurance, etc.) | ($68,400) |

Net Operating Income (NOI) | EGI - OpEx | $102,600 |

Less: Debt Service | Annual mortgage payments on the loan | ($72,000) |

Net Cash Flow (Before Taxes) | NOI - Debt Service | $30,600 |

In this scenario, after all the bills and the mortgage are paid, the property generates $30,600 in positive cash flow for the year. This is the income that provides returns to investors and fuels long-term wealth creation.

Novice Lens: Net Cash Flow is your take-home pay from the property. It's the simplest measure of whether your investment is making money or costing you money each month.

Advanced Metrics Sophisticated Investors Use

While Net Cash Flow is the end goal, institutional investors and lenders look deeper to truly understand a deal's strength and risk profile.

Advanced Lens: For sophisticated investors, metrics like DSCR and Cash-on-Cash Return are not just numbers; they are the language of institutional finance. They determine if a bank will even consider your loan application and how your deal stacks up against competing investment opportunities.

Debt Service Coverage Ratio (DSCR): This is calculated as NOI / Debt Service. Lenders use it to measure a property's ability to comfortably cover its mortgage payments. In our example, the DSCR is $102,600 / $72,000 = 1.43x. Most lenders require a DSCR of 1.25x or higher, so at 1.43x, this property would be considered a strong candidate for financing.

Cash-on-Cash (CoC) Return: This metric measures the annual cash flow relative to the total cash you invested out-of-pocket. If the down payment and closing costs for our example property totaled $400,000, the CoC return would be $30,600 / $400,000 = 7.65%. It gives you a crystal-clear picture of the return on your invested capital for that year.

Finding and Analyzing High Cash Flow Properties

Spotting properties with real income potential isn't about luck. It's a disciplined process that starts with the big picture—the market—and drills down to the nitty-gritty details of the asset itself.

Success in cash flow real estate starts by zeroing in on markets with strong fundamentals. This top-down view helps you put your capital to work where demographic and economic tailwinds can support rental demand for the long haul. Once you’ve found a promising submarket, the focus shifts to the property.

Conducting Thorough Market Analysis

Before you glance at a single property listing, you need to understand the market's health. We hunt for key signals of a thriving, resilient local economy.

Here are the big-picture indicators we look for:

A Diverse Job Market: We target areas with a healthy mix of employers in stable sectors like healthcare, technology, education, and logistics, avoiding dependence on a single industry.

Population Growth: A steady stream of new residents is one of the most powerful signs of a market’s appeal and future housing demand.

Favorable Price-to-Rent Ratios: In markets where buying is expensive relative to renting, you'll find a much larger and more stable pool of long-term renters.

Focusing on Property-Specific Traits

Once you’ve locked in on a target market, it’s time to evaluate individual assets. This is where underwriting discipline shines.

You have to look for these essential characteristics:

Location: Is it close to job centers, good transportation, and amenities people want, like schools and shops? Location drives demand.

Condition: Is the property in good shape, or is it a money pit waiting to happen? Deferred maintenance can demolish your cash flow.

Unit Mix: A smart mix of one, two, and three-bedroom units opens the door to a wider range of tenants, from young professionals to small families, keeping vacancy risk low.

Investor Takeaway: A B-class property in an A-grade location will almost always outperform an A-class property in a C-grade location over the long term. Why? Because location drives demand, and demand supports rents and occupancy—the two levers that control your cash flow.

Questions to Ask a Sponsor: Your Due Diligence Checklist

Analyzing a potential deal is all about asking the right questions. This is how you protect your capital and uncover an asset's true potential.

Here are the essential questions you should be asking any sponsor:

How do the projected operating expenses compare to market averages for similar properties?

What is the gap between current in-place rents and achievable market rents?

What has the property’s occupancy rate been over the last 3-5 years, and what were the drivers?

What is the specific, actionable plan to add value and increase the Net Operating Income?

What are the terms of any existing or proposed debt on the property?

How much is budgeted for immediate repairs and future capital improvements, and is it sufficient?

A sponsor who can give you clear, data-backed answers to these questions is showing their expertise and transparency. For a deeper look into our own process, review our firm's detailed acquisitions criteria.

Proven Strategies to Maximize Your Cash Flow

A great property is just the starting point. Actively creating superior returns requires a proactive, two-pronged approach: boost revenue and trim expenses. Disciplined investors do both, relentlessly hunting for operational wins that make a huge impact on the bottom line of their cash flow real estate portfolio.

Driving Revenue Growth

This goes way beyond just hiking rents. It's about a creative, strategic mindset—a hunt for the hidden value already inside the property.

Strategic Unit Upgrades: This is the classic "value-add" play. By investing in smart renovations—think modernizing kitchens, adding in-unit laundry, or installing smart-home tech—you can justify significant rent bumps that deliver a fantastic return on capital.

Adding Ancillary Income Streams: Look around the property. Are there underused spaces or services you can monetize? This could be anything from adding reserved parking spots and tenant storage units to leasing roof space for a cell tower. These small, recurring revenues add up.

Reducing Operating Expenses

On the other side of the ledger, cutting costs can be just as potent as raising revenue. Every dollar saved on expenses is a pure dollar of profit that drops straight to the bottom line.

Proactively Appeal Property Taxes: Your property tax assessment isn't written in stone. A successful appeal can be one of the single biggest expense cuts you'll ever make.

Negotiate Vendor Contracts: Don't just let contracts for landscaping, trash removal, or insurance auto-renew. Regularly putting these services out to bid ensures you're getting competitive prices without sacrificing quality.

Implement Energy-Efficient Systems: Upgrading to LED lighting, installing low-flow water fixtures, or investing in a modern HVAC system doesn't just slash utility costs. It also polishes the property's ESG profile, making it more attractive to tenants and future buyers.

Deal Lens Example: The Workforce Housing Turnaround

To see how this works, let's walk through a simplified case study of a 100-unit workforce housing asset we might target with a value-add strategy.

The Situation: A property with dated units and inefficient management. Rents were below market, and utility bills were too high. The mission was to boost the Net Operating Income (NOI) with targeted operational fixes.

The Action Plan:

Renovation: We executed a rolling renovation on 30% of the units, focusing on kitchens and bathrooms. This justified a $150/month rent premium on each upgraded unit.

Ancillary Income: We created a paid parking program for 50 premium spots, charging $50/month.

Expense Reduction: We swapped to a more efficient utility billing system and installed water-saving fixtures, cutting water and sewer costs by 12%.

The Impact: The renovations and new parking fees boosted annual revenue by $84,000, while our efficiency push cut expenses by $30,000. The result was a $114,000 increase in NOI—a 15% lift in just two years, creating substantial value. For a deeper dive, explore our investment insights.

Risk & Mitigation: Protecting Your Cash Flow

Every seasoned investor knows that preparing for the downside is just as important as planning for the upside. A smart strategy doesn't just hope for the best; it builds a fortress around your cash flow to protect it.

Key Cash Flow Risks and Mitigation Strategies

Risk: Unexpected Vacancies * An empty unit is a direct hit to your gross income, shrinking your Net Operating Income (NOI). * Mitigation: Maintain a dedicated capital reserve fund to cover income gaps. Implement proactive tenant retention programs to keep good tenants happy and reduce turnover.

Risk: Major Capital Repairs * A sudden major expense (e.g., a new roof, HVAC system) can wipe out months of cash flow. * Mitigation: A thorough Property Condition Assessment (PCA) pre-acquisition identifies future needs. A portion of monthly income is systematically set aside into a capital reserve account to fund these repairs without impacting investor distributions.

Risk: Tenant Defaults * Non-payment means an immediate loss of income, compounded by the legal costs of eviction. * Mitigation: A rock-solid tenant screening process is the first line of defense (credit checks, income verification). In larger properties, a diverse tenant base spreads this risk out.

Risk: Rising Interest Rates * Higher rates increase the cost of debt, squeezing the cash flow available for distribution. * Mitigation: Secure long-term, fixed-rate debt whenever possible to lock in costs. For variable-rate loans, purchase interest rate caps to limit exposure.

Final Thoughts: The Resilient Power of Cash Flow

Investing in cash flow real estate is more than a financial transaction; it's a commitment to a disciplined, long-term strategy for wealth preservation and growth. While market trends will come and go, the fundamental value of a well-located, professionally managed asset that generates consistent income remains a constant. For many family offices and high-net-worth investors, allocations to private real estate, as noted in recent reports by firms like UBS, continue to be a cornerstone of a diversified portfolio aimed at hedging inflation and generating reliable returns. You can read more about global real estate investment trends here.

Well-structured real assets can be a prudent, resilient component of your long-term wealth strategy. By focusing on strong fundamentals, disciplined underwriting, and active management, investors can navigate economic cycles with confidence.

Next Steps for Accredited Investors

At Stiltsville Capital, our entire focus is on finding and managing institutional-quality assets that deliver steady, risk-adjusted returns. If you're an accredited investor looking to see how a disciplined real estate approach could strengthen your portfolio, we invite you to connect with us.

Disclaimer: Information presented is for educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy securities. Any offering is made only through definitive offering documents (e.g., private placement memorandum, subscription agreement) and is available solely to investors who meet applicable suitability standards, including “Accredited Investor” status under Rule 501 of Regulation D. Investments in private real estate involve risk, including loss of capital, illiquidity, and no guarantee of distributions. Past performance is not indicative of future results.

Comments