Reading Time: 8 min | Good for: A, B

TL;DR: The Three Lenses of Property Value

Valuation is a process, not a single number. Sophisticated investors triangulate a property's worth using three core methods: what similar properties sold for (Sales Comparison), what it would cost to build new (Cost), and how much income it generates (Income).

For income-producing assets, cash flow is king. The Income Approach, especially a Discounted Cash Flow (DCF) analysis, is the most critical tool for evaluating commercial real estate as it directly links value to earning potential.

Assumptions drive everything. The final valuation is only as good as the inputs (rent growth, vacancy, exit cap rate). Your primary job as an investor is to pressure-test the sponsor's assumptions to ensure they are conservative and data-backed.

Figuring out what a commercial property is really worth is the absolute cornerstone of a smart investment. It’s less about landing on one perfect number and more about building a defensible price range from a few different angles. Relying on just one method is like trying to drive with one eye closed—you're missing the full picture.

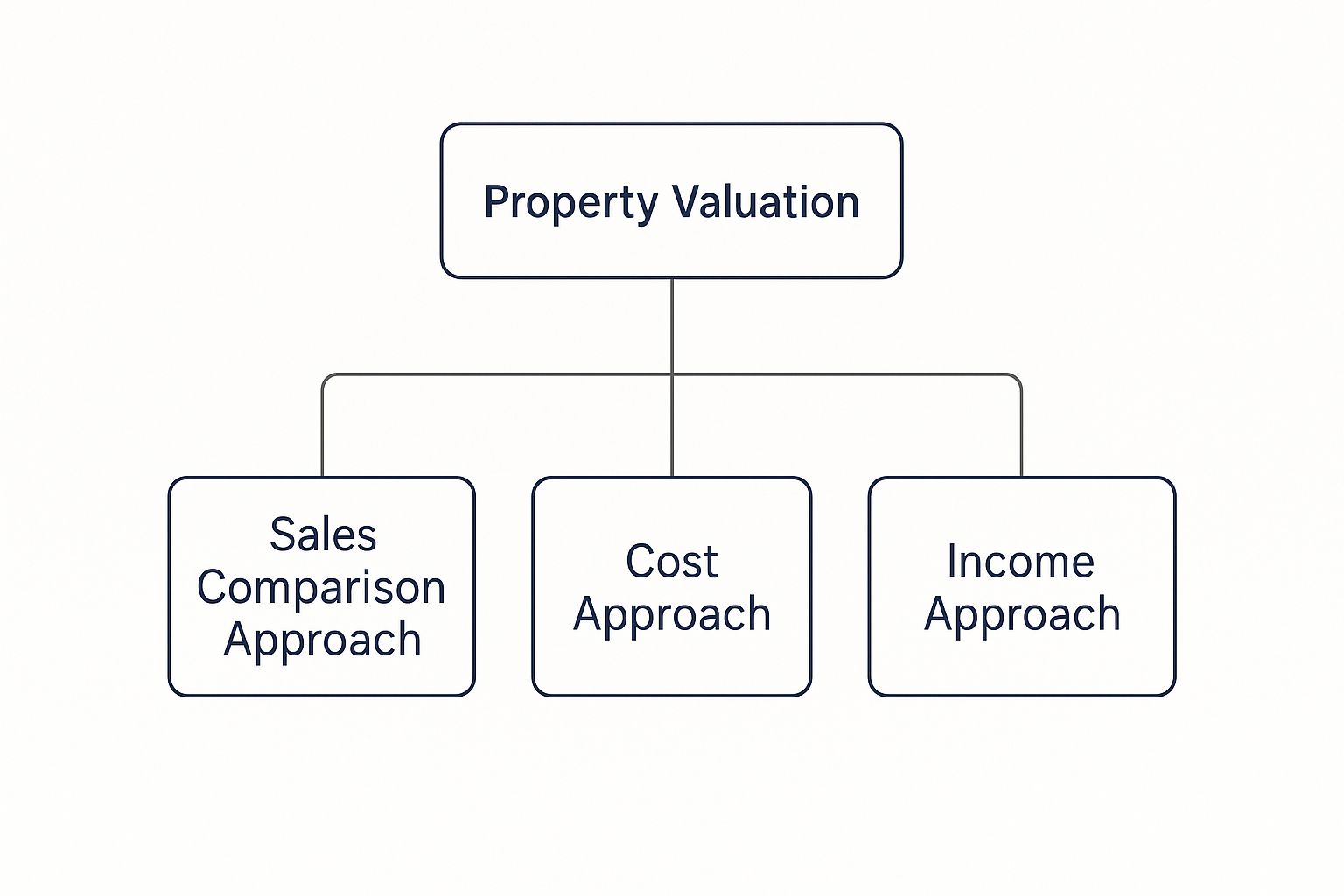

There are three main ways the pros do it: the Sales Comparison Approach, the Cost Approach, and the Income Approach. A seasoned investor knows how to weave all three together to get a three-dimensional view of a property's true value.

This isn't just academic; it's how you spot real opportunities and, just as importantly, how you avoid overpaying. Whether you're eyeing a brand-new apartment building or a tired strip mall ripe for a turnaround, getting a grip on these concepts is your first step to making a confident call.

The Three Pillars of Property Valuation

Every professional appraisal is built on three distinct, yet complementary, frameworks. Each one gives you a unique lens to look through, and which one you lean on most heavily often depends on the type of property and what the market is doing at that moment.

The Sales Comparison Approach: This one is the most intuitive. It answers a simple question: What did similar properties nearby just sell for? It's all about comparing apples to apples.

The Cost Approach: This method looks at value from a builder's perspective. It calculates what it would cost to build the exact same property from scratch today, then subtracts for any wear and tear (depreciation).

The Income Approach: For any property that generates rent, this is king. It values an asset based purely on the net income it's expected to produce over time.

This infographic shows how these three pillars work together to support a final valuation.

As you can see, a truly solid valuation doesn't just pick one. It pulls insights from all three approaches to arrive at a well-reasoned conclusion.

Novice Lens / Why This Matters: If a deal sponsor can't clearly explain why they favored one valuation method over another, it's a huge red flag. It might mean their underwriting process isn't as buttoned-up as it should be. The story behind the number is often more telling than the number itself, because it reveals the key assumptions driving their whole investment thesis.

Quick Guide to Real Estate Valuation Methods

To help you keep these straight, here’s a quick-glance table summarizing the three core methods. Think of it as your cheat sheet for understanding how any commercial property gets its price tag.

Valuation Method | Core Principle | Best Suited For | Key Metric |

|---|---|---|---|

Sales Comparison Approach | Value is determined by what similar properties have recently sold for. | Single-family homes, condos, and unique properties with many comparable sales. | Price Per Square Foot ($/SF) |

Cost Approach | Value is the cost to build a new, identical property, minus depreciation. | New construction, public buildings (schools, churches), and special-use properties. | Replacement Cost |

Income Approach | Value is based on the property's ability to generate future income. | Commercial properties: office, retail, industrial, multifamily apartments. | Capitalization Rate (Cap Rate) |

Each approach offers a unique perspective, and knowing when to apply each one is a hallmark of an experienced investor. By understanding these fundamentals, you're better equipped to analyze deals and ask the right questions.

Finding Value Through Comparable Sales (The Sales Comparison Approach)

Of all the ways to value a property, the Sales Comparison Approach is probably the most intuitive. It’s built on a simple idea we all use, whether we’re buying a car or a house: What did similar ones sell for recently? In commercial real estate, this means digging up recently sold properties—we call them “comparables” or “comps”—to set a value for the building we’re analyzing (the “subject property”).

This method is the absolute bedrock of residential real estate, and it carries serious weight in the commercial world, too. It’s especially useful for assets like apartment buildings, where you can find plenty of similar properties. At its core, the logic is that the market itself—all the buyers and sellers making deals—is the truest indicator of what something is worth.

Selecting the Right Comparables

The real magic of this approach is in picking the right comps. An appraiser isn't just grabbing any random building in the same zip code. The goal is to find properties that are as close to a carbon copy of the subject property as possible.

Here’s what they’re looking for:

Proximity: Closer is always better. A property just across the highway could be in a totally different submarket with its own set of rules.

Timing: Real estate markets don't stand still. A sale from a year and a half ago might as well be ancient history. You want comps that closed in the last three to six months.

Physical Attributes: This gets into the nitty-gritty: the building's age, its total square footage, the mix of units (like how many one-bedrooms vs. two-bedrooms), and its general condition.

Property Type: You have to compare apples to apples. A sprawling, garden-style apartment complex is a world away from a luxury high-rise condo building, even if they're neighbors.

But let's be realistic—perfect matches are like unicorns. That’s where the real skill comes in: making adjustments.

The Art of Adjustments

Once you have a handful of the best comps available, the next step is to account for the differences between them and your property. This isn't just guesswork. It's a methodical process of putting a dollar value on specific features and adjusting the comp's sale price up or down.

The key question you're trying to answer is, "What would this comparable property have sold for if it were identical to my property?"

Advanced Lens / Investor Takeaway: Adjustments are where an analyst’s assumptions can really move the needle on a valuation. If a deal sponsor is making adjustments, you should always ask how they landed on their numbers. A $5,000 adjustment per unit for a kitchen renovation needs to be backed by hard data showing that tenants in that specific submarket actually pay more rent for that upgrade, justifying the capital expense.

Adjustments are made for any meaningful difference, such as:

Location: A property on a quiet side street might get a positive adjustment compared to a similar one on a loud, busy avenue.

Condition: If your comp has a brand-new roof but your subject property’s roof is on its last legs, the comp’s sale price will be adjusted downward.

Amenities: Does the comp have a pool and a gym while your property doesn't? Its price will be adjusted down to level the playing field.

This whole process leans heavily on solid historical sales data, which usually comes from public records and industry tools like the Multiple Listing Service (MLS). The National Association of Realtors (NAR), for example, is a primary source for the residential sales data that underpins countless valuations. This data is so foundational that the Automated Valuation Models (AVMs) used by over 90% of U.S. mortgage lenders for initial estimates are built right on top of it, according to industry sources. To see the latest trends, you can check out the housing statistics from NAR's research team.

Challenges of the Sales Comparison Approach

As powerful as this method is, it isn't foolproof. It really shines in busy, active markets where there are plenty of recent sales to draw from.

It starts to lose its punch when:

The asset is unique: Good luck finding comps for a one-of-a-kind historic hotel or a highly specialized data center. It's nearly impossible.

The market is illiquid: In slow markets with few transactions, the only available data might be stale and out of touch with today's reality.

Data is unreliable: In some areas, sale prices aren't public knowledge, making it incredibly difficult to find verified comps you can trust.

Because of these potential blind spots, no savvy investor ever relies on this method alone. It's a critical piece of the puzzle, used to cross-check and validate the numbers you get from other methods—especially the Income Approach.

Valuing a Property Based on Its Cash Flow (The Income Approach)

When you're looking at any property that brings in rent—whether it's a bustling apartment complex or a quiet medical office building—the Income Approach is more than just another valuation tool. It's the most important one.

Comps can tell you what the market has paid for similar assets, and the Cost Approach tells you what it would take to build from scratch. But the Income Approach gets to the heart of the matter: what is this property worth based on the money it can earn? This is the language every serious investor speaks.

The philosophy is refreshingly simple. A commercial property’s value is directly tied to the net income it generates. More income means more value. It’s the bedrock of disciplined underwriting, especially for value-add and opportunistic plays where the entire game is about boosting cash flow over time.

There are two main ways we translate that cash flow into a hard number: Direct Capitalization and Discounted Cash Flow (DCF) analysis.

The Direct Capitalization Method

Think of this method as taking a property’s financial pulse. It gives you a quick, powerful snapshot of its value based on a single year’s income. The formula is beautifully straightforward but incredibly insightful, boiling everything down to just two key ingredients: Net Operating Income (NOI) and the capitalization rate (cap rate).

The formula looks like this: Value = Net Operating Income (NOI) / Capitalization Rate (Cap Rate)

Before you can use it, you need the NOI. This isn't just profit. It's a specific metric that shows the property’s income after all operating expenses are paid but before you factor in debt service (the mortgage) and income taxes.

Here’s a quick rundown of how to get there:

Gross Potential Rent: The absolute maximum rent you could collect if the property was 100% occupied.

Less Vacancy: An allowance for the reality that some units will be empty.

Effective Gross Income (EGI): What you actually expect to collect.

Less Operating Expenses: This covers everything from property taxes and insurance to management fees, utilities, and maintenance.

Equals Net Operating Income (NOI): The final figure representing the property's raw earning power.

Once you have your NOI, you divide it by the cap rate. The cap rate is simply the expected rate of return you’d get if you bought the property with all cash. It’s a crucial market indicator that tells you a lot about both opportunity and risk. A lower cap rate implies lower risk and higher value, while a higher cap rate suggests more risk and a lower value.

Novice Lens / Why This Matters: The cap rate is more than just a number; it's a reflection of market sentiment. When investors are confident and capital is cheap, cap rates compress (go down), pushing property values up. When uncertainty rises, cap rates expand (go up), pushing values down.

The Discounted Cash Flow (DCF) Method

If Direct Capitalization is a snapshot, then Discounted Cash Flow (DCF) analysis is the full-length movie. It's the gold standard for projecting an asset's value over a longer holding period, typically five to ten years. This method is absolutely essential for any strategy where the plan is to improve the property and grow its income over time.

DCF involves a few more steps, but the logic is powerful. It’s built on a fundamental financial principle: a dollar today is worth more than a dollar tomorrow.

The process generally breaks down like this:

Project Annual Cash Flows: Forecast the property's NOI for each year you plan to hold it, factoring in things like expected rent growth and rising expenses.

Estimate a Terminal Value: Calculate what you think the property will sell for at the end of your holding period. This is often done by applying a future "exit cap rate" to the final year's NOI.

Choose a Discount Rate: This is the required rate of return an investor demands for taking on the project's risk. It’s the rate you'll use to translate all those future dollars back into today’s money.

Calculate Present Value: Each year's projected cash flow, plus the terminal value, is "discounted" back to its value today using that discount rate.

Sum It All Up: Add up all those present values, and you get the total estimated value of the property right now, according to your DCF model.

This method is crucial for investors, especially when [understanding properties with a secured yield for long periods](https://www.noagent.properties/5pa-yield-secured-for-25-years-67f78dd337631b0012b7fcca/), as it helps quantify the true value of those long-term, stable income streams.

Because it forces you to think critically about the future—from rent growth to market conditions years down the road—DCF is an indispensable tool for sophisticated analysis. To see this in action, check out our guide on [how to calculate a discounted cash flow for real estate success](https://www.stiltsvillecapital.com/post/how-to-calculate-a-discounted-cash-flow-for-real-estate-success). It truly separates a speculative bet from a well-underwritten investment.

Determining a Property's Replacement Cost (The Cost Approach)

What would it cost to build this exact property from the ground up today? That’s the simple but powerful question at the heart of the Cost Approach, one of the foundational methods for valuing commercial real estate.

The logic is straightforward: a rational investor isn't going to pay more for an existing property than it would cost to build a brand-new, equivalent one from scratch. This makes the Cost Approach an essential tool for valuing assets where you can't just look up recent sales of similar properties—think new developments or unique assets like data centers, medical facilities, or public buildings.

The process boils down to two key steps. First, you calculate the current cost to construct the building and all its improvements (the replacement cost). Second, you subtract any depreciation that has built up over time.

Understanding the Three Forms of Depreciation

Depreciation isn't just about physical wear and tear. It’s any factor that makes the existing property less valuable than its brand-new counterpart. In real estate, this breaks down into three distinct categories.

Physical Deterioration: This is the one we all think of first—the tangible decline of a property. It's the worn-out roof, the cracked pavement, or the HVAC system that’s on its last legs. Basically, it's the cost to fix what’s broken or old.

Functional Obsolescence: This is about outdated design, even if everything is in perfect working order. A classic example is an old office building with too few electrical outlets for a modern tech-heavy team, or a multifamily property with a choppy, closed-off floor plan that today's renters hate. The "cost to cure" these design flaws gets subtracted from the value.

External Obsolescence: This type is completely out of the owner's control. It’s caused by negative factors outside the property lines, like a major local employer shutting down, new zoning laws that restrict the property’s use, or a new highway ramp that brings constant traffic and noise. This is almost always considered incurable.

Advanced Lens / Investor Takeaway: The Cost Approach provides a crucial reality check, acting as an upper limit on a property's value. If a sponsor pitches a value-add deal where the purchase price is close to—or even above—the replacement cost, you should dig deeper. Their strategy needs to clearly justify why buying an older building makes more sense than just building a new one.

This is becoming even more critical as new construction methods gain ground. Investors looking at development deals should explore the [9 key modular construction benefits](https://www.stiltsvillecapital.com/post/9-key-modular-construction-benefits-for-real-estate-investors-in-2025), which can dramatically change the replacement cost calculation.

When Cost Does Not Equal Value

Here’s a common trap: assuming that what you spend on a property automatically equals its market value. While the Cost Approach tells you the price of the "bricks and sticks," it doesn't dictate what the market is actually willing to pay. Market demand is always the final judge.

This is also clear in retrospective appraisals, which are used to determine a property’s value on a past date for legal or tax reasons. These valuations rely on deep historical data to understand past market conditions, not just what it cost to build back then.

For instance, the Federal Housing Finance Agency (FHFA) data shows that U.S. single-family home prices have seen dramatic long-term growth driven by economic trends, inflation, and demand—factors that go far beyond simple construction costs.

How Professionals Settle on a Final Number (Reconciliation)

Getting to a final valuation isn't as simple as plugging numbers into three formulas and taking the average. The truth is, a single valuation method rarely paints the full picture. Instead, seasoned professionals go through a critical thinking process called reconciliation.

This is where the art of real estate valuation truly meets the science. Reconciliation is all about weaving together the values from the Sales Comparison, Cost, and Income approaches into a single, logical, and—most importantly—defensible conclusion. It's an exercise in professional judgment, not just number crunching.

The trick is to assign the right amount of weight to each method based on the property itself and the reason for the valuation in the first place.

The Art of Assigning Weight

Think of each valuation method as an expert witness in a courtroom. Depending on the case, some witnesses will have far more credible and relevant testimony than others. The appraiser or investor plays the role of the judge, deciding which testimony is the most compelling.

Several factors influence how this "weight" is assigned:

Property Type: The kind of asset you're looking at is the biggest driver. For a fully leased office building with a solid, long-term tenant, the Income Approach is king. It will likely carry 70-80% of the weight, if not more, because its value is almost entirely tied to its cash flow.

Data Quality and Availability: If you’re valuing a standard apartment building in a busy city with tons of recent, nearly identical sales, the Sales Comparison Approach is incredibly reliable and will be weighted heavily. On the other hand, if you're trying to value a one-of-a-kind data center with no recent sales to compare it to, that approach becomes almost useless.

Purpose of the Valuation: The "why" behind the valuation changes everything. For insurance purposes, the Cost Approach is what matters most because it determines what it would cost to rebuild. For a private equity firm looking to buy, the Income Approach (especially a deep-dive DCF analysis) will dominate the entire conversation.

Advanced Lens / Investor Takeaway: When you’re looking at an investment summary, the final valuation number isn't as important as understanding the logic behind it. A sharp sponsor should be able to clearly explain why they gave more weight to one method over another. This tells you everything about their core investment strategy.

Connecting the Dots to Market Reality

Valuation doesn't happen in a bubble. Big-picture economic trends, especially interest rate cycles, can throw a wrench into the inputs for every single approach, forcing professionals to constantly tweak their models.

A perfect example of this was the global shift in 2023, when private real estate valuations dropped by 5–15% in major markets. This was a direct result of central banks, like the U.S. Federal Reserve, jacking up interest rates from near zero to over 5% in about 18 months. That move immediately drove up the cost of debt and pushed cap rates higher, putting serious downward pressure on values calculated with the Income Approach.

As one analysis pointed out, private real estate valuations often lag what's happening in the public markets by a few quarters. This meant the full impact of those rate hikes was a slow-motion adjustment that played out over many months. You can explore a detailed overview of this trend in the Pension Real Estate Association's quarterly report.

At the end of the day, the final conclusion of value is a carefully reasoned opinion. It’s backed by data, years of experience, and a clear-eyed view of what’s happening in the market. It's the point where all the methods of real estate valuation finally come together into a single, actionable number.

Investor Checklist: Questions to Ask About Valuation

A sophisticated valuation is more than just a number on a page. It’s the story of a property's potential, its risks, and the sponsor's core strategy. As a passive investor, your job is to scrutinize that story. Asking the right questions is the single best way to pressure-test the underwriting and make sure a sponsor's assumptions are grounded in reality, not wishful thinking. A transparent sponsor will welcome these questions.

Key Questions on Methodology and Assumptions

Which valuation methods did you lean on most heavily and why? For an income property, the sponsor must have a clear rationale centered on the Income Approach.

What are your key assumptions for rent growth, vacancy, and expense inflation over the hold period? Ask for the source of this data (e.g., market reports from CBRE, JLL, CoStar).

How did you determine the exit cap rate? A conservative sponsor will assume a higher (less aggressive) cap rate at sale than the cap rate at purchase to build in a margin of safety. Our guide to [cap rate and NOI](https://www.stiltsvillecapital.com/post/cap-rate-and-noi-your-guide-to-smarter-real-estate-investing) digs deeper into this critical metric.

What comparable sales did you use, and what major adjustments were made? Understand how they normalized for differences in location, condition, and amenities.

What is the "as-is" value versus the "as-stabilized" value? This is crucial for value-add deals. It shows the value today versus the projected value after renovations and lease-up are complete.

Probing for Risk and Downside Scenarios

Can I see your sensitivity analysis? Ask how the valuation and returns are affected if interest rates rise, leasing takes longer, or construction costs go over budget.

What is the weakest or most aggressive assumption in your model? This question forces transparency and reveals where the projections are most vulnerable.

How does the purchase price compare to the replacement cost? If you are paying near or above the cost to build new, the deal's logic needs to be rock-solid.

Common Questions About Real Estate Valuation

Even after you get the hang of the core valuation methods, a bunch of practical questions always pop up when you're looking at a real deal. It’s one thing to know the theory, but another to apply it in the real world. Let's break down some of the most common questions we hear from family offices and accredited investors.

How often should a commercial property be valued?

For transactional purposes—like a purchase or refinancing—a lender will almost always require a formal, third-party appraisal.

For institutional asset managers, however, valuation is an ongoing discipline. We re-evaluate our portfolio internally at least quarterly. This isn't a full-blown appraisal each time, but a disciplined "mark-to-market" analysis where we stress-test our original assumptions against the latest sales comps, leasing data, and macroeconomic trends. This ensures our reporting to partners is transparent and our strategy remains sound.

What is the difference between Market Value and Investment Value?

This is a crucial distinction that separates sophisticated investors from the rest of the pack.

Market Value is the objective, probable price a property would command on the open market between a willing buyer and a willing seller. It reflects the consensus view of value based on comps and standard income analysis.

Investment Value is subjective. It's what a property is worth to a specific investor based on their unique circumstances. For example, an investor might have a lower cost of capital, unique tax advantages, or operational synergies with an adjacent property they own. For them, the investment value could be significantly higher than the market value.

How is technology changing property valuation?

Technology, especially AI, is making the valuation process faster and more data-heavy. Automated Valuation Models (AVMs) can process vast datasets of property records and market trends to produce an estimate in seconds. For a general idea of how this works, some resources on determining your home's value use similar data-driven methods.

However, AVMs are a tool, not a replacement for human expertise. An algorithm cannot walk a property to spot deferred maintenance, understand the nuanced dynamics of a specific submarket, or envision a creative value-add strategy. The future isn't AI replacing experts; it's experts using AI to supercharge their analysis, combining powerful data processing with the strategic, on-the-ground insight that only experience can provide.

At Stiltsville Capital, we believe that well-structured real estate can be a prudent, resilient component of a long-term wealth strategy. We blend rigorous, multi-layered valuation with deep market knowledge to identify compelling investment opportunities for our partners. If our disciplined approach aligns with your goals, we invite you to [schedule a confidential call](https://www.stiltsvillecapital.com).

Information presented is for educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy securities. Any offering is made only through definitive offering documents (e.g., private placement memorandum, subscription agreement) and is available solely to investors who meet applicable suitability standards, including “Accredited Investor” status under Rule 501 of Regulation D. Investments in private real estate involve risk, including loss of capital, illiquidity, and no guarantee of distributions. Past performance is not indicative of future results. Verification of accredited status is required for participation in Rule 506(c) offerings.