Preferred Return in Real Estate: An Investor's Guide

- Ryan McDowell

- Oct 14, 2025

- 11 min read

Reading Time 7 min | Good for: Novice & Informed Investors (A, B)

TL;DR: Key Takeaways

Investor-First Structure: A preferred return ("pref") acts like a VIP line for your investment returns. It ensures you, the Limited Partner (LP), receive profits up to a pre-agreed rate before the deal sponsor (General Partner or GP) takes their performance fee.

Powerful Alignment: This structure creates a powerful alignment of interests. The sponsor must clear this performance hurdle before earning their promote, motivating them to hit or exceed financial targets.

Downside Protection: If a project underperforms, 100% of distributable profits go to investors until the preferred return is met. It's a priority of payment, not a guarantee, but it provides a critical layer of capital protection.

The Critical Question: Always ask if the pref is "cumulative." This means any unpaid returns carry over to future years and must be paid before the sponsor profits. A non-cumulative pref is a significant red flag.

What a Preferred Return Means for Your Investment

When you're evaluating a private real estate deal, the term "preferred return" is one of the most important concepts to understand. It's a foundational mechanism that dictates the priority of profit distributions and is a hallmark of institutional-quality investments.

Think of it as a contractual hurdle. Before the project sponsor (the General Partner or GP) can earn their performance-based compensation (known as the "promote" or "carried interest"), passive investors (the Limited Partners or LPs) must first receive their returns, up to a specific, pre-agreed-upon annual rate.

This structure is designed to give you, the investor, confidence. It demonstrates that the sponsor is laser-focused on performance, as their ultimate compensation is directly tied to your capital first earning its preferred return.

How It Protects Your Capital

The primary function of a preferred return is to place your returns first in line, ahead of the sponsor's promote. This creates a critical layer of downside protection for your investment capital.

What happens if a project doesn't perform as expected and available profits are lower than the preferred return threshold? In that scenario, 100% of the profits that can be distributed go directly to the investors. The sponsor receives no promote until that hurdle is cleared. This setup ensures the sponsor is motivated from day one to protect and grow your capital.

Understanding the Numbers in Today's Market

Preferred returns are a standard feature in real estate private equity. While the exact rate varies by strategy and risk profile, market data provides a reliable benchmark. According to a 2023 survey from Private Equity International, approximately 80% of private equity funds set their preferred return (or hurdle rate) at 8%. Real estate funds typically operate in a similar range, often targeting 7% to 9% for value-add or opportunistic strategies.

It’s important to understand how this fits into the broader capital stack. For a deeper dive into how different types of capital are structured and protected, our guide on real estate preferred equity offers more context.

Novice Lens: Why It MattersThe preferred return is your first line of defense. It means the people managing your money don't get their big payday until you get yours. It's a simple, powerful way to ensure everyone is pulling in the same direction.

Key Aspects of a Preferred Return at a Glance

Component | What It Means for You (The Investor) |

|---|---|

Return Priority | You are first in line to receive profits up to the agreed-upon rate. |

Sponsor Alignment | The sponsor is incentivized to hit performance targets before earning their promote. |

Downside Protection | If profits are modest, you receive them all before the sponsor gets a performance fee. |

Contractual Rate | The percentage is fixed in the legal operating agreement and cannot be changed. |

This table neatly summarizes why the preferred return is such a crucial, investor-friendly feature. It’s a clear, contractual promise that puts your capital first, ensuring everyone is working toward the same goal: a successful and profitable project.

How Your Preferred Return Is Calculated

To truly understand a real estate deal, you have to look under the hood at how the preferred return is calculated. The percentage is the headline number, but the mechanics are what truly impact your bottom line. These details are always spelled out in the deal's legal documents, and they typically fall into one of two categories.

The most common and investor-friendly structure is cumulative and non-compounded. If the property's cash flow in a given year is insufficient to pay the full preferred return, the unpaid portion accrues (i.e., it's added to a running tab). This entire accrued balance must be paid out from future profits before the sponsor can receive their promote.

A less common, but more powerful, version for investors is cumulative and compounded. This method treats any unpaid preferred return as an addition to your invested capital. The shortfall from one year is added to your capital balance, and the following year's return is calculated on that new, larger amount. You are effectively earning a return on your unpaid returns.

Unpacking the Calculation Methods

Let's illustrate this with a simple example. Assume you invest $100,000 into a project with an 8% preferred return.

Cumulative, Non-Compounded: In Year 1, the deal only generates enough cash to pay a 5% return, so you receive $5,000. The remaining 3% ($3,000) is carried forward as an accrued shortfall. In Year 2, before the sponsor can take any promote, you are owed that year's 8% return plus the $3,000 shortfall from Year 1.

Cumulative and Compounded: In the same scenario, the unpaid $3,000 from Year 1 is added to your capital balance. For Year 2, your 8% preferred return is now calculated on a new basis of $103,000, not your original $100,000. Over a multi-year hold, this compounding can significantly enhance total returns.

Investor Takeaway: Always confirm that a preferred return is cumulative. A non-cumulative pref resets each year, meaning any shortfall is lost forever. This is a massive red flag in most deals because it fundamentally misaligns the sponsor's interests with yours.

Return Of Capital vs. Return On Capital

Here’s another critical distinction: "return of capital" versus "return on capital." They sound similar but are worlds apart.

Return of Capital is simply getting your initial investment back. It’s the first hurdle in any distribution waterfall—the deal returns your original $100,000 to you.

Return on Capital is your profit. Your preferred return is a return on the capital you have invested.

The sequence is vital: first, your capital is returned. Second, you are paid your preferred return. Only after both hurdles are cleared does the sponsor participate in remaining profits via the promote. These distributions can be funded from ongoing operational cash flow or from a major capital event, like a sale or refinancing.

The timing of capital contributions also matters. The preferred return clock should only start on capital you've actually contributed, not your total commitment. This is why a firm grasp of performance metrics is essential for accurate modeling. To dig deeper, check out our guide to calculating the Internal Rate of Return.

Seeing The Capital Waterfall In Action

It’s one thing to understand the mechanics of a preferred return, but seeing how it directs the flow of cash in a real deal is where it all clicks. The sequence of payments is dictated by the capital waterfall—a tiered structure that spells out exactly who gets paid, when, and in what order.

This process guarantees that capital is distributed in a specific, pre-arranged sequence, reinforcing the investor-first approach that is the foundation of a well-structured deal. Think of it as a transparent roadmap for distributing profits that protects passive investors.

Deal Lens Example: A Value-Add Multifamily Project

Let's walk through a simplified illustrative case. Imagine Stiltsville Capital and our co-investors acquire a multifamily property, execute a value-add business plan over five years, and sell it for a profit.

Total Equity Invested: $5,000,000 (from Limited Partners)

Agreed-Upon Preferred Return: 8% cumulative, non-compounded

Total Sale Proceeds (after all debt and costs): $12,000,000

With the asset sold, the capital waterfall begins, distributing the $12,000,000 in a precise sequence.

Investor Takeaway: The waterfall isn't just a financial model; it's a contractual obligation within the operating agreement. It legally enforces payment priority, ensuring the sponsor cannot take their promote until investors have received both their initial capital back and their full preferred return.

The Tiers of Distribution

The distribution happens in distinct tiers. Money only flows to the next tier after the previous one is fully satisfied.

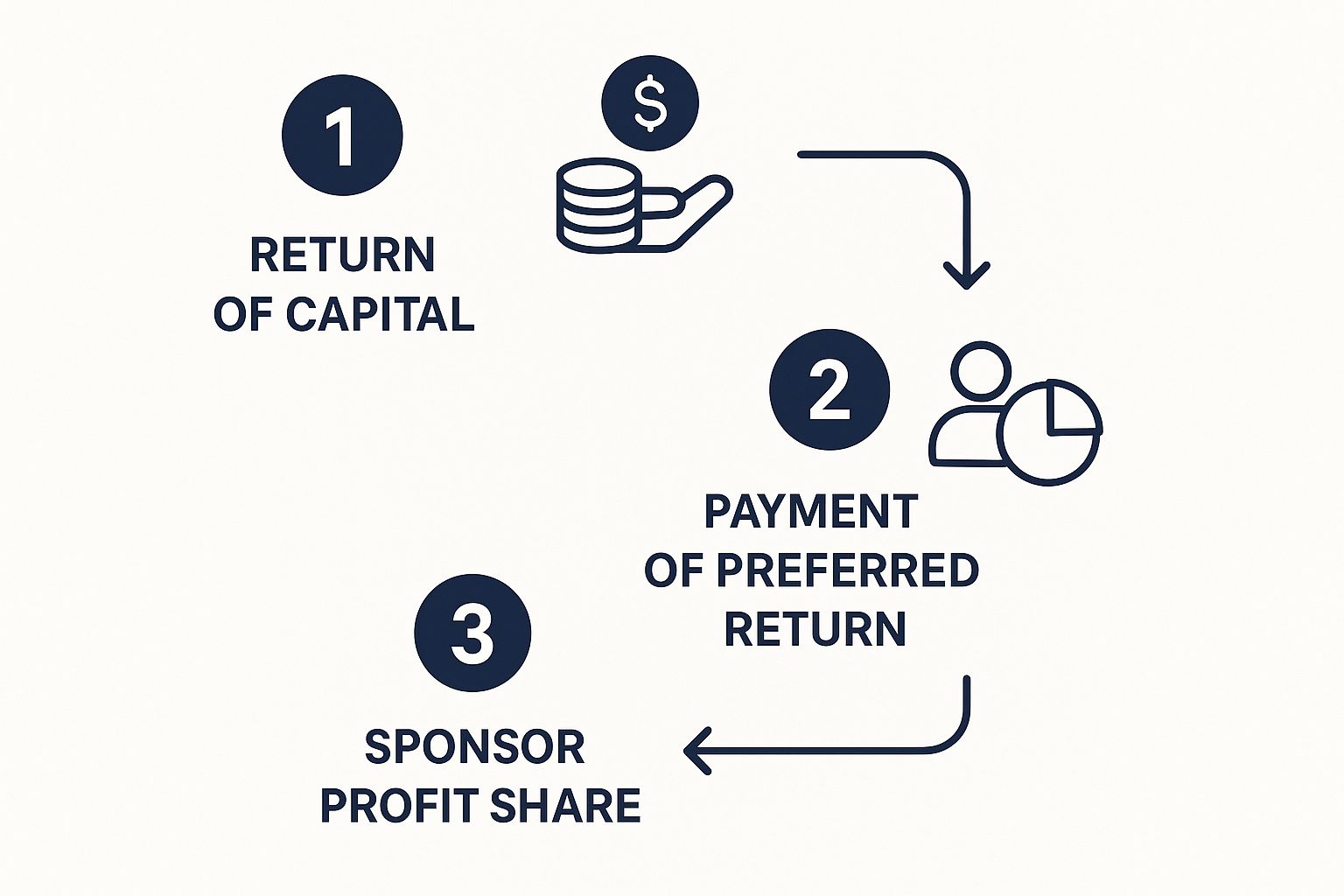

Tier 1: Return of Capital The very first dollars out are returned to the investors. In our scenario, the first $5,000,000 is distributed to the Limited Partners, fully repaying their initial investment.

Tier 2: Payment of Preferred Return Next, the accrued preferred return is paid. With an 8% cumulative pref on $5,000,000 over five years, the total preferred return owed is $2,000,000 ($400,000 per year). This amount is paid out to investors.

Tier 3: The Profit Split (Promote) Only now, with investors made whole on their capital and preferred return, does the sponsor share in the remaining profit. After the first two tiers, $5,000,000 remains ($12M - $5M - $2M). This amount is then split according to the promote structure—for example, 80% to investors ($4,000,000) and 20% to the sponsor ($1,000,000).

To make this even clearer, the table below shows how the $12,000,000 from the property sale would flow through the waterfall, step-by-step.

Illustrative Waterfall Distribution for a $12M Property Sale

Distribution Tier | Amount Allocated | Remaining Proceeds | Who Receives the Funds |

|---|---|---|---|

Initial Proceeds | $12,000,000 | ||

Tier 1: Return of Capital | $5,000,000 | $7,000,000 | Limited Partners (Investors) |

Tier 2: Preferred Return | $2,000,000 | $5,000,000 | Limited Partners (Investors) |

Tier 3: Profit Split (80/20) | $5,000,000 | $0 | $4,000,000 to LPs, $1,000,000 to Sponsor |

This tiered structure clearly shows the sponsor’s profit participation is the final step, happening only after all investor capital and preferred returns have been paid. This disciplined sequence is the ultimate mechanism for aligning sponsor and investor interests.

This simple infographic helps visualize the clear, sequential flow of the capital waterfall, from returning initial investments to sharing final profits.

For a deeper dive into these structures, feel free to check out our comprehensive guide to the waterfall in private equity.

Why a Preferred Return Is Not a Guarantee

This is perhaps the single most important nuance a passive real estate investor must understand. While a preferred return is a fantastic tool for aligning interests and protecting your downside, it’s a priority of payment, not a guarantee of payment.

The "pref" dictates where money goes first; it doesn't magically create money if a project fails to generate sufficient profit.

Think of it like having a VIP ticket to a concert. The ticket gets you to the front of the line, but it doesn't guarantee the show will go on. If the band cancels, everyone goes home empty-handed. Similarly, if a real estate deal underperforms due to market shifts or unforeseen asset-level problems, there may not be enough cash to meet the preferred return target.

Understanding Real-World Risks & Mitigants

A deal’s performance can be impacted by factors outside the sponsor's control. A preferred return gives you first claim on profits, but it can’t insulate you from major property issues like the impact of mold in commercial buildings, which can trigger expensive remediation and diminish asset value.

Risk & Mitigation Table

Risk: Market Downturn * Mitigant: Conservative underwriting with realistic rent growth, stress-testing financials against recessionary scenarios, and investing in resilient property types like workforce housing or medical office.

Risk: Interest Rate Spikes * Mitigant: Using conservative leverage, securing fixed-rate debt when possible, or purchasing interest rate caps to limit exposure on floating-rate loans.

Risk: Construction Overruns * Mitigant: Building in significant contingency reserves, using guaranteed maximum price (GMP) contracts with contractors, and having an experienced construction management team.

Risk: Exit Cap Rate Expansion * Mitigant: Underwriting the exit to a higher cap rate than the purchase cap rate, creating value that is not dependent on cap rate compression, and having flexible hold periods to avoid selling into a weak market.

In any of these adverse scenarios, investors would still receive 100% of whatever profits are available up to their full return of capital and preferred return, but the final amount might fall short of the target. The sponsor would receive no promote.

Investor Takeaway: A sponsor's confidence should be backed by disciplined underwriting, not just optimism. The best sponsors are transparent about potential risks and can clearly articulate their strategies to protect investor capital in a downturn.

This is where the quality and experience of the sponsor become paramount. A seasoned operator plans for adversity from day one. They bake resilience into their deals through conservative underwriting, rigorous stress testing, and proactive asset management designed to maximize income and control expenses through all market cycles.

Key Questions to Ask a Sponsor About the 'Pref'

Knowing the theory behind a preferred return is a great start, but the real test comes from asking the right questions. The "pref" percentage on the cover of an investment summary is just the beginning of the story. The true alignment between you and the sponsor is defined by the fine print in the operating agreement.

Coming prepared with sharp, specific questions demonstrates your sophistication and helps you quickly assess a sponsor’s transparency and experience.

Investor Checklist: Preferred Return Due Diligence

Before wiring funds, ensure you have clear, satisfactory answers to these questions. A high-quality sponsor will welcome this level of diligence.

Is the preferred return cumulative? This is non-negotiable. If the answer isn't an immediate "yes," you should seriously reconsider the investment. A non-cumulative pref means any unpaid return in a given year is lost forever—a clear misalignment of interests.

Does the preferred return compound? While less common than a simple cumulative structure, compounding can significantly enhance returns on longer-term holds. Ask if any accrued pref is added to the capital base for future calculations.

How are shortfalls handled? Confirm that any unpaid pref accrues and must be paid out—from future operating cash flow or a capital event like a sale—before the sponsor receives their performance fee (the "promote").

When does the pref clock start? Clarify whether the return is calculated on committed capital or contributed capital. It should be the latter, meaning the pref only accrues on funds you have actually invested in the project.

What is the full capital waterfall structure? Ask the sponsor to walk you through every tier. Understand if there are any "catch-up" provisions that allow the sponsor to earn a disproportionately large share of profits after the pref is paid, as this can significantly alter the final profit split.

How does the DSCR support the pref? A deal’s ability to pay its pref from operations depends on its financial health. It's smart to evaluate the overall financial health of the real estate investment by understanding its Debt Service Coverage Ratio (DSCR). This ratio shows the property’s ability to cover its mortgage payments, which directly impacts the cash available for investor distributions.

Getting clear answers to these questions empowers you to partner with sponsors who truly prioritize your capital and structure their deals for mutual success.

Final Thoughts: A Prudent Part of Your Portfolio

The preferred return is more than just financial jargon; it's a critical structural safeguard that aligns interests and protects passive investors. By prioritizing the return of and on investor capital, it ensures that sponsors are profoundly motivated to perform.

Understanding these mechanics allows you to cut through the noise and identify well-structured opportunities that fit within a long-term wealth strategy. While no investment is without risk, features like a cumulative preferred return are key mitigants that make private real estate a prudent and resilient component of a diversified portfolio.

At Stiltsville Capital, we believe in total transparency and building long-term relationships based on trust and aligned interests. We are always ready to walk you through every line of our deal structures.

If you are an accredited investor ready to explore institutional-grade real estate opportunities, we invite you to schedule a confidential call.

Learn more about our disciplined approach at https://www.stiltsvillecapital.com.

Information presented is for educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy securities. Any offering is made only through definitive offering documents (e.g., private placement memorandum, subscription agreement) and is available solely to investors who meet applicable suitability standards, including “Accredited Investor” status under Rule 501 of Regulation D. Investments in private real estate involve risk, including loss of capital, illiquidity, and no guarantee of distributions. Past performance is not indicative of future results.

Comments