A Disciplined Guide to Analyzing Multifamily Investment Opportunities

- Ryan McDowell

- Nov 29, 2025

- 17 min read

Reading Time: 9 min | Good for Audiences: A, B, C

TL;DR: Key Takeaways for Investors

A winning deal starts with a winning market. Before you ever look at a property's financials, you must confirm the local economy has durable, long-term growth drivers in jobs, population, and income.

Underwriting is forensic work. Scrutinize the Trailing 12-Month (T-12) financials and rent roll to build a realistic Net Operating Income (NOI). Trust, but verify, every number the seller provides.

Your pro forma must survive a stress test. A solid financial model isn't a single prediction; it's a dynamic tool for sensitivity analysis. You must understand how returns hold up in a downside scenario.

The goal is superior risk-adjusted returns. This guide provides a repeatable, institutional-grade framework to help you separate genuine opportunities from deals with hidden landmines, ensuring your capital is deployed wisely.

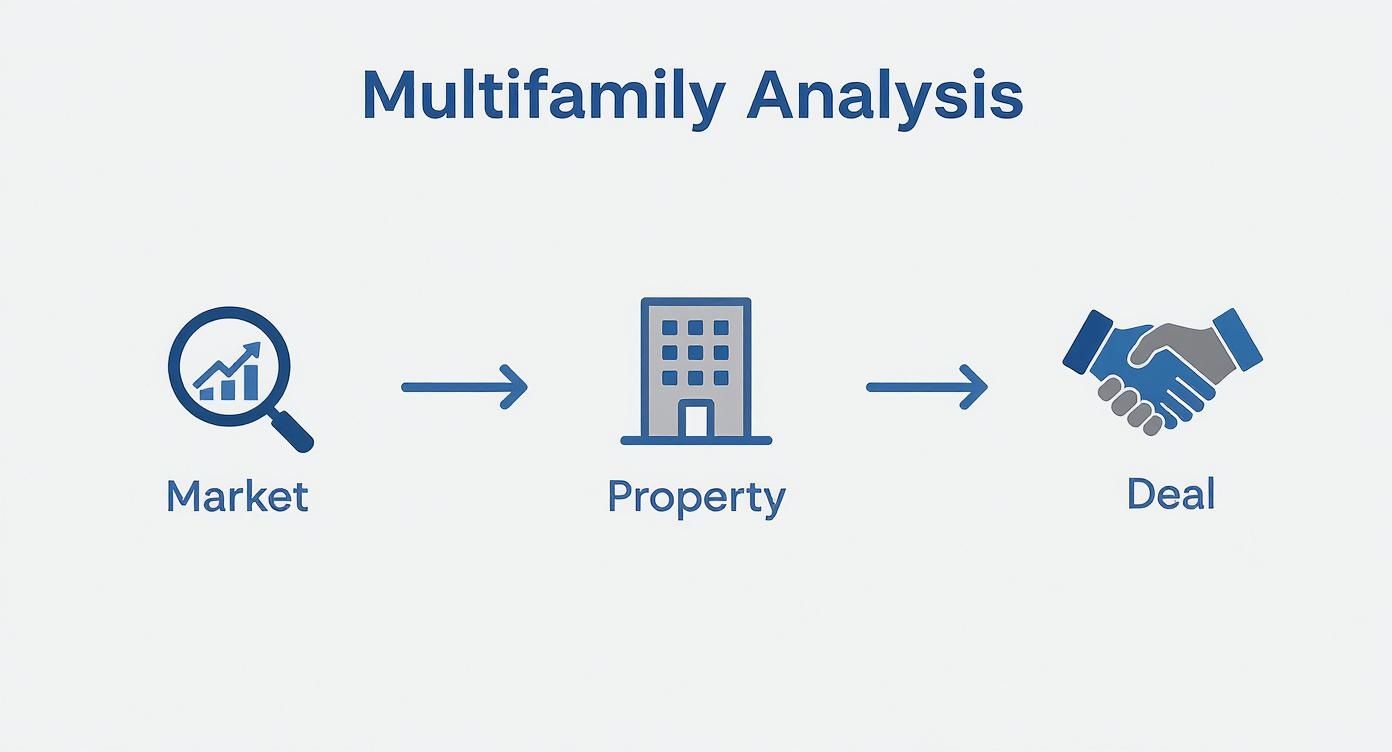

To succeed in multifamily investing, a disciplined process is non-negotiable. At Stiltsville Capital, we break it down into a simple, three-part framework: evaluate the market, underwrite the property, and structure the deal. This approach forces you to look beyond flashy numbers and ground your decisions in solid economics and realistic projections.

This guide lays out that exact framework—a repeatable process for analyzing any multifamily opportunity that comes across your desk. We'll start big by showing you how to build a strong investment thesis based on market dynamics, then zoom in on the nitty-gritty of property-level underwriting.

The goal here is simple: to give you the confidence to vet deals, spot genuine value-add potential, and protect your capital.

Along the way, you'll learn:

The critical questions you must ask sponsors and brokers.

Which key performance indicators (KPIs) actually move the needle on multifamily assets.

How to build a financial model that can stand up to scrutiny and stress testing.

This flowchart gives you a bird's-eye view of the entire process. It shows the logical flow from high-level market assessment, down to the property specifics, and finally, to the deal itself.

Following this sequence ensures you never get lost in a spreadsheet without first confirming the big-picture strategy makes sense. Each step builds on the last, creating a solid foundation for your investment decision.

Key Multifamily Analysis Pillars at a Glance

A solid analysis always balances a top-down view of the market with a bottom-up examination of the asset itself. The market tells you if you have a favorable wind at your back, while the property specifics tell you if your boat is seaworthy.

Here’s a quick summary of the core pillars we’ll be diving into, giving you a roadmap for what’s to come.

Market & Submarket Research: To confirm strong, sustainable demand drivers exist. * Key Metrics: Population growth, job growth, median income, rent growth trends.

Property-Level Underwriting: To accurately project Net Operating Income (NOI) and cash flow. * Key Metrics: Trailing-12 (T12) financials, rent roll, operating expenses per unit.

Pro Forma & Modeling: To forecast future performance based on your business plan. * Key Metrics: Internal Rate of Return (IRR), Cash-on-Cash Return, Equity Multiple.

Valuation & Comps: To determine a realistic purchase price and exit value. * Key Metrics: Capitalization (Cap) Rate, price per unit, price per square foot.

Financing & Deal Structure: To optimize leverage and returns for all partners. * Key Metrics: Loan-to-Value (LTV), Debt Service Coverage Ratio (DSCR).

Due Diligence & Risk Mitigation: To uncover hidden issues and protect your investment. * Key Metrics: Physical inspections, lease audits, environmental reports, title review.

As you get started, you might find our complete guide to investing in multifamily properties a helpful resource for some of the foundational concepts.

Investor Take: A great property in a dying market is a high-risk bet. A mediocre property can perform well in a booming market. Your analysis must rigorously assess both to find true, sustainable value. This structured approach is the bedrock of any successful long-term real estate portfolio.

Evaluating Market and Submarket Dynamics

A great deal in a bad market isn't a great deal at all—it’s a gamble. Before you even think about cracking open a rent roll or a T-12, your real work begins with the market itself. This is what we call a disciplined, top-down approach. It's about making sure your capital is flowing into areas with real, durable economic tailwinds, not just chasing a momentarily attractive yield. Think of it like checking the weather before you set sail; a rising tide of job and population growth can lift every asset in a market.

Your first move is to build a solid investment thesis grounded in what actually drives demand. This means you have to go way beyond national headlines and get granular, digging into the specific Metropolitan Statistical Area (MSA) and, even more importantly, the submarket where the property sits.

Identifying Thriving Economic Ecosystems

The local economy is the engine that powers rental demand. You're hunting for markets with diverse and, critically, growing employment sectors. A city that hinges on a single industry is incredibly vulnerable. A market with strong anchors in healthcare, tech, education, and logistics? That’s where you find resilience.

Start by zeroing in on these core economic vital signs:

Job Growth: Is it consistent? Look for positive job growth over the last three to five years. A rate that’s beating the national average is a huge green flag.

Population Growth: Are people moving to the area? Census data and reports from firms like CBRE or JLL will show you clear trends on net migration.

Median Household Income Growth: This is a big one. Rising incomes give tenants the ability to absorb future rent increases, which is the entire ballgame for any value-add strategy.

Novice Lens: Why This MattersIt’s really this simple: more jobs pull in more people. More people need a place to live. And if those people are earning more money each year, they can afford higher rents—which directly boosts the value of your apartment building.

Decoding Supply and Demand Signals

This might be the most critical piece of market analysis. You have to understand the delicate balance between new apartment supply and the actual demand from renters. An overbuilt submarket can trigger a race to the bottom, forcing landlords into a concession war that kills rent growth for years.

On the flip side, an area with a tight lid on new supply and high demand is a landlord’s paradise.

This supply-demand dynamic is playing out right now across the country. According to recent research from RealPage, the U.S. apartment market absorbed a massive 637,100 market-rate units over the past year (as of Q1 2024)—that's nearly double the decade average. But new deliveries are finally slowing down.

This supply pressure caused national occupancy to tick down just 30 basis points to 95.4%. The story varies by region, though. The supply-heavy South and West saw some rent cuts, while the Midwest and Northeast actually posted modest rent gains. It’s a perfect example of how much submarket conditions matter.

Questions to Ask a Sponsor About the Market

When you’re vetting a deal, you need a structured approach to catch the red flags. It's about weaving data into a coherent story about where the market is headed. Ask your potential sponsor or partner these questions:

Who are the top five employers and are they growing? Are they stable, blue-chip companies, or are they in volatile industries one bad quarter away from layoffs?

What is the complete development pipeline? Ask for a list of all new multifamily projects—approved or under construction—in a three-mile radius. This is your crystal ball for future competition.

What specific public infrastructure projects are funded? Vague promises are worthless. Ask about funded investments in transportation, parks, and schools. These are magnets for long-term growth.

What are the exact local regulations on rent control and permitting? Is the city pro-development, or are you walking into a regulatory minefield? This can make or break your entire business plan.

By starting with a deep dive into the market, you build a rock-solid foundation for your entire investment analysis. Only after you’ve confirmed the market supports your thesis should you even consider moving on to property-level underwriting.

Mastering Property-Level Financial Underwriting

Once you’ve confirmed a market has solid fundamentals, it’s time to zoom in on a specific property. This is where your investment thesis gets its first real stress test against the cold, hard numbers.

Financial underwriting is the disciplined process of dissecting a property’s past performance to build a credible forecast of its future. It’s part detective work, part financial modeling.

It all starts with two critical documents: the rent roll and the trailing 12-month (T-12) operating statement. These aren't just spreadsheets; they tell the financial story of the property, revealing everything from tenant stability to operational leaks.

Deconstructing the Rent Roll and Operating Statements

The rent roll is a real-time snapshot of the property’s revenue engine. It lists every unit, who lives there, their lease dates, square footage, and what they pay. Your T-12, on the other hand, is the property's P&L for the past year. Your job is to scrutinize each line item, verify its accuracy, and hunt for red flags.

Analogy: Buying a Classic CarYou wouldn't buy a vintage Porsche without demanding its full service history. The T-12 shows you exactly how the property has been running and where the money has been going. The rent roll tells you who's paying the bills—and if they're paying what they should be.

You can't just take the seller's numbers at face value. A classic move is to understate expenses to make the NOI look healthier than it really is.

Here’s what to look for:

Inflated Income: Are one-time windfalls like a big lease termination fee being presented as recurring revenue?

Understated Expenses: Does the T-12 show suspiciously low numbers for repairs and maintenance? Are property management fees well below the market rate of 3-5%? That’s a common trick.

Deferred Maintenance: If the repairs budget is consistently tiny, it's a huge red flag. It likely means the current owner is kicking the can down the road, leaving you with a big capex bill the day you take over.

The U.S. multifamily sector continues to show stable fundamentals, making accurate underwriting critical. Recently, effective rent growth hit 1.1% year-over-year, pushing rents over 20% above pre-pandemic levels. Investment volume reached $43.8 billion last quarter—a 13% jump from the previous year.

Cap rates have also held steady near 5.7% for seven straight quarters, signaling market stability. (Data as of Q1 2024, from Arbor.com). You have to dig into the local absorption rates, rent trends, and debt conditions, because these are what will make or break your projections.

Calculating Key Performance Metrics

Once you've scrubbed the historical data, it’s time to run the numbers. The first and most important is Net Operating Income (NOI).

NOI = Effective Gross Income (EGI) - Operating Expenses

NOI is the property's pure, unleveraged annual profit before you account for your mortgage or taxes. It is the single most important figure in commercial real estate. Period. With a credible NOI, you can establish a baseline valuation using the market capitalization (cap) rate.

Property Value = NOI / Cap Rate

A cap rate is simply the expected rate of return if you bought the property with all cash. A lower cap rate implies lower risk and a higher valuation, while a higher cap rate suggests higher risk and a lower price tag.

Beyond NOI and cap rate, a few other metrics are crucial:

Cash-on-Cash Return: Measures your annual pre-tax cash flow against the total cash you invested. It answers a simple question: "For every dollar I put in, what am I getting back each year?"

Debt Service Coverage Ratio (DSCR): Lenders live and die by this number. It’s NOI divided by your total annual mortgage payments. A DSCR of 1.25x or higher is the standard minimum, as it shows the property generates 25% more cash than needed to cover the debt.

Internal Rate of Return (IRR): A more sophisticated metric that calculates your total annualized return over the entire hold period, factoring in the time value of money. It includes both annual cash flow and your projected profit from the eventual sale.

Financial underwriting is data-intensive. To focus on the strategic assumptions that truly drive returns, consider how technology can help. Exploring resources on using AI for financial analysis can offer valuable techniques for automating the grunt work.

Building a Dynamic Pro Forma and Sensitivity Analysis

Historical performance gives you a baseline, but an investment’s real success is written in its future. Once you've scrubbed the T-12, it's time to build a credible, multi-year pro forma—your financial forecast for the property over your entire hold period.

This isn’t just about plugging numbers into a spreadsheet. The goal is to create a dynamic financial model that lets you test your core assumptions and understand the full spectrum of potential outcomes.

Crafting Defensible Assumptions

Every number in your pro forma needs to be anchored in solid market research and a realistic operational plan. This is where your top-down market analysis meets your bottom-up property underwriting. Anybody can model aggressive rent growth; disciplined investors build a case for it.

Your key assumptions will boil down to three core drivers:

Revenue Growth: To project future rent bumps, look at submarket rent comps, historical trends, and local economic forecasts for wage growth. A conservative starting point is 2-3% annual rent growth, adjusted based on your value-add strategy.

Vacancy Rates: Never assume 100% occupancy. A standard economic vacancy assumption is 5-8%, which wisely accounts for both physical vacancies (empty units) and things like concessions or bad debt.

Expense Inflation: Expenses rarely stay flat. Property taxes, insurance, and utilities are notorious for creeping up. A prudent approach is to model expense growth at 2-3% annually. Pay extra attention to insurance, which has seen major hikes in many markets.

Investor Take: Your pro forma is only as strong as its weakest assumption. Be conservative. It is always better to be pleasantly surprised by outperformance than to explain why a deal failed to meet overly optimistic projections.

Stress-Testing with Sensitivity Analysis

Once your base-case pro forma is built, the real analysis begins. Sensitivity analysis is the art of systematically changing your key assumptions to see how those tweaks impact your returns. This is what separates a professional analysis from a simple sales pitch.

The whole point is to answer those critical "what if" questions that expose a deal's weak spots. To build a truly robust pro forma, leveraging specialized finance FPA data analysis tools for forecasting and scenario planning can enhance the accuracy of your financial models.

Your stress tests should map out the full risk/return profile of the investment by modeling a few different scenarios.

Essential Scenarios to Model

Base Case: Your most likely outcome, built on conservative, well-researched assumptions. It’s the foundation of your investment thesis.

Downside Case: What happens if the market softens? Model a scenario with flat or even negative rent growth, higher vacancy (think 10%), and an increase in your exit cap rate by 50-75 basis points. If the deal still provides an acceptable return—or at least preserves your capital—it shows real resilience.

Upside Case: Your best-case scenario. Maybe your value-add renovations hit a home run and achieve higher rent premiums than expected. Or perhaps the market booms, letting you exit at a compressed cap rate. This helps you understand the deal’s maximum potential.

By modeling these different outcomes, you move from a single-point estimate of returns (like a 17% IRR) to a much more realistic range of possibilities. An investment that looks great in the base case but falls apart with a minor change in assumptions is a fragile one. A deal that holds up across multiple scenarios? That’s one worth pursuing.

Valuing the Property and Structuring the Deal

Once you’ve stress-tested your pro forma, it's time to figure out what the property is truly worth and how to put together a deal that makes sense. A fantastic forecast doesn't mean much if you overpay or finance the acquisition poorly. This is where valuation and deal structuring come together to build the foundation of your offer.

Core Valuation Methods for Multifamily Assets

You should never hang your hat on a single valuation method. A disciplined investor always triangulates the value using several different techniques. This ensures your final number is grounded in reality.

There are three primary ways we look at value in multifamily:

The Income Approach: The bread and butter for any income-producing property. The property's value is directly tied to the cash it generates. You take your projected first-year Net Operating Income (NOI) and divide it by the market cap rate. For instance, a property with a $500,000 NOI in a 5% cap rate market is valued at $10 million.

The Sales Comparison Approach: Often called "running comps." We look at recent sales of similar properties in the immediate area. The trick is to make true apples-to-apples comparisons, adjusting for differences in age, condition, and amenities.

The Replacement Cost Approach: This acts as a useful reality check. It calculates what it would cost to build the exact same property from scratch today. An investor is highly unlikely to pay more for an existing building than it would cost to build a brand new one next door.

Advanced Lens: The DCF ModelWhile the income approach is great for stabilized assets, value-add deals demand a more sophisticated Discounted Cash Flow (DCF) analysis. This model projects cash flows over the entire hold period and discounts them back to a present value, providing a more nuanced valuation. Learn more about how to calculate a discounted cash flow for real estate.

Structuring the Capital Stack

Beyond the purchase price, how you finance the deal is every bit as critical. The mix of debt (the loan) and equity (your cash) is called the capital stack. Getting this balance right is crucial for managing risk and boosting returns.

The key financing metric here is the Loan-to-Value (LTV) ratio. An LTV of 75% means the bank is putting up 75% of the purchase price, and you’re bringing the other 25% in cash.

Pushing for higher leverage can juice returns, but it also dials up risk. If the property's income dips, a hefty mortgage can wipe out your cash flow. A more conservative LTV provides a bigger safety cushion.

Financing is always influenced by the broader market. Current forecasts (as of Q2 2024) put rent growth at a modest 2.2%, below the long-term average of 2.8%, while vacancy rates are expected to climb to 6.2%. Today's elevated interest rates are putting downward pressure on property values, making a careful financing strategy more important than ever.

When talking to lenders, don't just focus on the interest rate. Negotiating loan terms like the term length, amortization schedule, and prepayment penalties is just as important. A well-structured deal gives you the flexibility to execute your business plan.

Executing Diligence and Making the Final Decision

So, your analysis points to a winner. The numbers are solid and the market story checks out. Now for the moment of truth where all those assumptions get tested: due diligence. This isn’t just a formality. Think of it as a deep, forensic investigation to confirm the asset you think you're buying is the asset you're actually getting. No surprises.

Successful diligence means methodically vetting three core pillars: the financials, the physical building, and the legal paperwork. Your goal is to sniff out any hidden problems that weren’t obvious during initial underwriting.

The Three Pillars of Investigation

The diligence period, usually 30 to 60 days, is your one shot to validate every assumption. A well-prepared sponsor will have a digital data room loaded with all the key documents. For a much more detailed breakdown, our team put together A Guide to Commercial Real Estate Due Diligence, an investor's playbook for this process.

Here’s a look at what we're tackling in each pillar:

Financial Diligence: This means a full lease audit—comparing every single lease agreement against the rent roll to confirm terms, security deposits, and expiration dates. You’ll also dig into service contracts, utility bills, and tax statements to verify operating expenses.

Physical Diligence: Time to get your boots on the ground. You or your team will walk every unit and inspect every corner. More importantly, you'll bring in third-party experts to assess the big-ticket items: the roof, HVAC systems, plumbing, and electrical. A Phase I environmental assessment is a must-do to check for hidden contamination issues.

Legal Diligence: Your attorney leads the charge. They'll run a full title search to ensure the seller has a clean right to sell the property. They’ll also review the property survey for any easements or encroachments and check city records for open permits or zoning violations.

Investor Take: Due diligence findings almost always lead back to the negotiating table. If you uncover serious deferred maintenance or find that financials aren't as advertised, it's completely standard to go back to the seller and ask for a price cut or a credit to cover those unexpected costs.

Making the Final Go/No-Go Decision

Once all reports are in, it’s time to update your financial model with the real-world numbers you’ve just uncovered.

Did the lease audit show that actual income is lower than what was on the rent roll? Your revenue projections need to be adjusted. Did the inspection reveal the roof only has two years of life left? That capital expense needs to be plugged into your model.

This final, diligence-adjusted pro forma is the most accurate picture you’ll have of your true expected returns. Now, the final decision comes down to one question: Does this deal, with all its newly discovered realities, still hit your return targets and fit your risk tolerance? A disciplined process ensures your final decision is based on hard facts, not hopeful projections.

Risk & Mitigation Checklist for Multifamily Investments

Risk: Overstated Income * Description: The seller presents financials showing higher income than what is contractually in place. * Mitigation: Conduct a comprehensive lease audit, comparing every single lease to the official rent roll.

Risk: Hidden Deferred Maintenance * Description: Major systems like the roof or HVAC are nearing the end of their life, setting you up for a massive, near-term replacement cost. * Mitigation: Commission third-party physical inspections (a Property Condition Assessment) from qualified engineers.

Risk: Environmental Liability * Description: The property has soil or groundwater contamination from a past use, creating a huge potential cleanup liability. * Mitigation: Order a Phase I Environmental Site Assessment to identify any potential environmental hazards.

Risk: Title & Zoning Issues * Description: There are hidden liens, restrictions, or zoning conflicts that could limit your use of the property. * Mitigation: Engage legal counsel to perform a thorough title search, survey review, and zoning analysis.

By systematically addressing each of these areas, you're not just buying a property; you're making a calculated investment with a clear understanding of what you're getting into.

Quick Hits: Your Multifamily Analysis Questions Answered

To wrap things up, let's tackle some of the most common questions that come up when you're learning the ropes of multifamily analysis. These are the quick, clear insights you need to evaluate your next deal with total confidence.

What is a "good" ROI in multifamily investing?

This is the million-dollar question, but smart investors don’t chase a magic number; they hunt for the best risk-adjusted return.

For a stable, Class A property in a prime location, an annual return of 8-12% might be attractive. But for a riskier value-add project or ground-up development, you'd better be targeting 16-20% (or even higher) to make the uncertainty worthwhile. The right ROI is all about your strategy and the market. The real question is: does this potential return actually justify the risks I'm taking?

How do you spot red flags during due diligence?

The biggest red flags are often hiding in plain sight. A rent roll loaded with month-to-month leases is a sign of instability. Be suspicious of a T-12 operating statement with suspiciously low numbers for repairs or property management—this is a classic trick to inflate the NOI by kicking maintenance down the road.

One of the most telling red flags? A seller who is disorganized or slow to provide key documents. If they can't produce clear records, it's often because they're hiding something. In this business, transparency is everything.

And if a physical inspection turns up major issues like foundation cracks or ancient electrical systems, it's time to pause. Those are the kinds of capital-intensive nightmares that can torpedo your pro forma.

What's more important: IRR or Cash-on-Cash Return?

This isn't an either/or situation—both metrics are critical, but they tell different stories.

Think of Cash-on-Cash Return as your "right now" metric. It’s a clean look at the annual cash flow you’re getting back compared to the equity you put in. It answers the question: "How much passive income is this property putting in my pocket this year?"

Internal Rate of Return (IRR), on the other hand, is the big-picture metric. It calculates your total annualized return over the entire life of the deal, factoring in both the yearly cash flow and the big payday when you sell. While IRR is essential for judging overall profitability from start to finish, your cash-on-cash return is the vital sign of the investment's immediate financial health.

Take the Next Step

Analyzing multifamily opportunities requires discipline, but the right framework makes it achievable. This process—market first, then property, then deal—is how sophisticated investors protect and grow capital over the long term. Well-structured real estate can be a prudent, resilient component of a long-term wealth strategy.

If you are an accredited investor and would like to learn more about our disciplined approach or review our current offerings, we invite you to connect with us.

Schedule a confidential call with Stiltsville Capital

Information presented is for educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy securities. Any offering is made only through definitive offering documents (e.g., private placement memorandum, subscription agreement) and is available solely to investors who meet applicable suitability standards, including “Accredited Investor” status under Rule 501 of Regulation D. Investments in private real estate involve risk, including loss of capital, illiquidity, and no guarantee of distributions. Past performance is not indicative of future results. Verification of accredited status is required for participation in Rule 506(c) offerings.

Comments