What Is Preferred Equity? A Guide for Real Estate Investors

- Ryan McDowell

- Jul 27, 2025

- 10 min read

Reading Time: 7 min | Good for: Novice Investors (A), Informed Principals (B)

Let's get straight to it. Preferred equity is a unique type of investment that blends the steady, predictable income you'd expect from a loan with the growth potential of owning a piece of a real estate asset. It’s a powerful tool for sophisticated investors seeking attractive risk-adjusted returns.

It’s often called a “hybrid” security for a good reason. Think of it as sitting in the sweet spot of a real estate deal’s capital structure—it’s tucked right between the relative safety of a traditional bank loan and the higher-risk, higher-reward position of a common equity partner.

TL;DR: Key Takeaways on Preferred Equity

What it is: A hybrid investment that combines debt-like features (a fixed return) with equity-like features (potential profit sharing).

How it works: Preferred equity investors receive a fixed, priority payment (a "preferred return") before the project's sponsors or common equity investors receive any profits.

Who it's for: Investors seeking higher returns than traditional debt but with more downside protection and predictability than a standard common equity position.

The Market "Why Now"

In today's market, flexible capital is king. As of Q1 2024, many real estate sponsors are navigating a landscape of higher interest rates and tighter bank lending standards. According to analysis from firms like CBRE, this has created a "capital gap" in many deals, particularly for refinancing or new developments. Preferred equity has become a go-to solution to bridge this gap, creating compelling opportunities for investors who can provide this crucial layer of capital.

Visualizing The Real Estate Capital Stack

To really get a handle on what is preferred equity, you first have to understand where it fits into the bigger picture. That picture is the capital stack—the financial blueprint for every single real estate deal. It’s a simple but powerful concept that outlines who gets paid, in what order, and how much risk each investor is taking on.

Think of it like building a pyramid. Each block is a different type of funding, stacked from the safest at the bottom to the riskiest at the top.

The Foundation: Senior & Mezzanine Debt

At the very bottom, forming the wide, stable base, is Senior Debt. This is your classic bank loan or primary mortgage, secured by the property itself. Because they have the first claim on repayment if things go south (and the right to foreclose), senior debt holders are in the safest position.

Moving one layer up, you might find Mezzanine Debt. This is a secondary, smaller loan that fills the gap between the senior loan and the equity. It's riskier than senior debt since it only gets paid after the bank, but it still stands in line ahead of any equity investors.

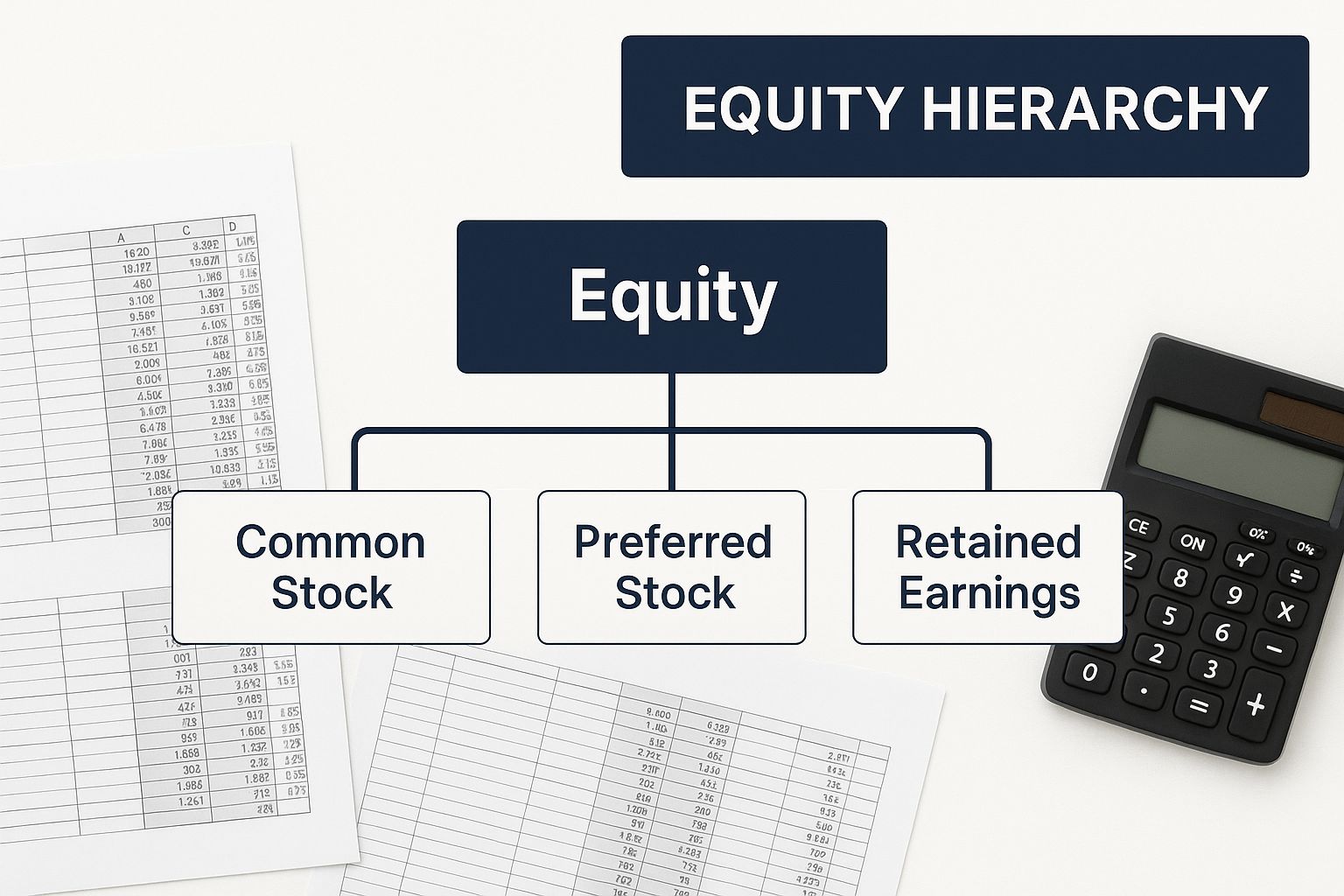

The Hybrid Middle Ground: Preferred Equity

Right in the middle, we find Preferred Equity, the star of our show. It sits in a unique, strategic spot—it’s junior to all the debt, but it’s senior to the common equity. This means preferred equity investors get their money back, plus their promised return, before the project sponsors (the common equity) see a dime of profit.

Novice Lens: Why It Matters Imagine a line for a sold-out concert. The senior debt holders are at the very front, guaranteed to get in. The common equity holders are way at the back, hoping the venue isn't full. Preferred equity investors? They're comfortably in the middle—not first, but way ahead of the huge crowd at the back, with a great shot at getting in and enjoying the show.

The Peak: Common Equity

Finally, at the very top of the pyramid, is Common Equity. This is the high-risk, high-reward slice of the pie, usually funded by the deal sponsor and their co-investors. They are the absolute last to get paid. But if the project is a home run, their profit potential is unlimited. Understanding this pecking order is absolutely critical when you're looking at any real estate investment.

Understanding Key Terms and Investor Rights

Alright, let's get into the nitty-gritty of how a preferred equity deal actually works. This is where you go from understanding the concept to speaking the language of professional investors. For any serious due diligence, knowing these terms isn't just helpful; it's essential.

Every preferred equity agreement is built around a handful of core components that define your rights, returns, and risk.

Core Components of a Preferred Equity Deal

Preferred Return: The headline number—the fixed annual rate of return your investment is set to earn, like 9% or 11%. This return gets paid before any profits are distributed to the common equity holders.

Current Pay vs. Accrual (PIK): This defines when you get paid. A Current Pay structure means you receive regular cash distributions (e.g., quarterly). An Accrual or "Payment-in-Kind" (PIK) structure means the return you earn gets added to your initial investment and is paid out in one lump sum when the property is sold or refinanced.

Equity Kicker: This is an upside booster. On top of your fixed return, a "kicker" gives you a slice of the back-end profits. For instance, a deal might offer a 10% preferred return plus 5% of the profits after all capital is returned.

Maturity Date: The target date for when the sponsor plans to pay back your principal and any accrued return. It provides a clear timeline for the investment's expected lifecycle.

The market for these investments is always shifting. For example, some market analysis from sources like Cohen & Steers has shown that preferred securities can offer attractive yields compared to other fixed-income assets, especially when interest rates are in flux. As of late 2023, for example, yields on publicly traded preferreds were significantly higher than they were a year prior, reflecting the changing rate environment. For the latest analysis, it's always worth reviewing expert insights on preferred securities.

Deal Lens: How Preferred Equity Plays Out

Theory is one thing, but seeing the numbers in action is where it all clicks. Let’s walk through a simplified case study to see how preferred equity works in a real-world scenario.

Imagine Stiltsville Capital identifies an underperforming apartment complex. The total cost to acquire and renovate it is $20 million.

The Initial Capital Stack

Here’s how the $20 million gets funded:

Senior Debt: A bank provides a $12 million (60% LTV) first-position mortgage.

Preferred Equity: A family office provides $4 million of preferred equity structured with a 10% annual accruing return.

Common Equity: Stiltsville Capital, as the sponsor, along with our co-investing partners, contributes the remaining $4 million. We are last in line to be repaid but retain the majority of the upside.

For two years, we execute our business plan: renovating units, improving management, and increasing net operating income. During this time, the 10% preferred return on the $4 million accrues, totaling $800,000 ($400,000 per year).

The Exit and the "Payment Waterfall"

Two years later, the stabilized property is sold for $25 million. Now, the proceeds are distributed via the "payment waterfall," a strict sequence that dictates who gets paid and when.

Informed Investor Takeaway: The waterfall is non-negotiable and is the primary mechanism for risk mitigation in the capital stack. Its rigid structure is what gives preferred equity its security relative to common equity.

Here’s how that $25 million is distributed:

Pay Off Senior Debt: The bank is paid first. $12 million goes to repay the mortgage.

Pay Off Preferred Equity: Next, the preferred equity investors receive their $4 million principal plus the $800,000 in accrued return, for a total of $4.8 million.

Return Common Equity: The sponsor and co-investors get their initial $4 million investment back.

Distribute Profits: The remaining $4.2 million ($25M - $12M - $4.8M - $4M) is profit. This entire amount flows to the common equity holders as the reward for taking the most risk.

This example shows preferred equity's role perfectly. It bridged a critical funding gap, allowed the value-add plan to proceed, and earned its investors a strong, contractually-defined return, paid out right behind the senior lender.

Investor Checklist: Questions to Ask a Sponsor

When a sponsor presents a preferred equity opportunity, your knowledge becomes a practical checklist. The answers to these questions directly impact your cash flow, total return, and principal safety. A vague answer is a red flag.

What is the precise Preferred Return, and is it Current Pay, Accrual, or a hybrid?

Is the return cumulative? (Crucial: This means any missed payments stack up and must be paid in full before common equity gets anything.)

Is there an Equity Kicker? If so, how is it calculated and at what point in the waterfall does it get paid?

What is the loan-to-value (LTV) of the senior debt? (A lower LTV means more protective equity cushion below you.)

What is the stated maturity or anticipated redemption date?

What are my rights in the event of a default on payments or a failure to redeem on time? (e.g., penalty interest, ability to force a sale).

What is the sponsor's track record with this specific asset class and strategy?

Can you walk me through the downside scenarios in your underwriting?

For a deeper dive into financial modeling, see our guide to commercial real estate underwriting.

Weighing the Advantages and Risks

Every smart investment decision comes down to a clear-eyed assessment of risk versus reward. Preferred equity is no different.

The Upside: Why Investors Choose "Pref"

The appeal lies in its built-in safety features and predictability compared to a standard equity deal.

Priority of Payment: You get paid your return—and get your initial capital back—before common equity investors see a dime. This creates a significant cushion if a project underperforms.

Predictable Returns: The fixed "preferred return" creates a more consistent and reliable income stream (or accrual) than the residual profits that flow to common equity.

Potential for Upside: An "equity kicker" can offer the best of both worlds: the stability of a fixed return with a shot at equity-like profits.

The Risks & Mitigation

Risk: Subordination to Debt * You are behind the senior lender. If the property is sold at a loss, the bank gets paid first, and there is a risk your principal may not be fully recovered. * Mitigation: Partner with sponsors who use conservative leverage. A lower loan-to-value (LTV) ratio means a larger equity cushion exists to absorb value declines before your position is impacted.

Risk: Limited Control * You typically don’t get voting rights or a say in the day-to-day operations of the project. * Mitigation: Your diligence on the sponsor is paramount. A sponsor with deep experience, a transparent communication style, and a history of successful execution is your best risk mitigant.

Risk: Capped Upside * Your potential profit is generally limited to the preferred return plus any kicker. You miss out on the uncapped upside common equity enjoys in a "home run" deal. * Mitigation: This is a feature, not a bug. It’s the explicit trade-off for a lower-risk position and payment priority. If your goal is a stable 10-14% IRR with more security, this structure aligns perfectly.

Why Do Sponsors Use Preferred Equity?

Thinking like a sponsor is key to spotting a good deal. Why would a sponsor offer a preferred equity position instead of just raising more common equity or taking on more debt?

At its core, sponsors use preferred equity to solve a funding puzzle while maintaining control and maximizing their own upside. When a sponsor offers a preferred equity slice, it's often a sign of confidence. They are betting the project will generate enough profit to easily cover the fixed preferred return and still deliver a significant return for their common equity.

Advanced Lens: The Sponsor's Rationale When a sponsor opts for preferred equity, they are making a calculated decision. They are effectively saying, "We believe so strongly in the upside of this deal that we would rather pay a fixed, higher-cost coupon on this capital than dilute our share of the ultimate profits by bringing in more common equity partners."

Key reasons include:

Less Dilution: Bringing in more common equity partners means slicing the profit pie into smaller pieces. Preferred equity lets sponsors keep a larger share of the potential profits.

More Flexibility than Debt: Mezzanine debt often comes with restrictive covenants and foreclosure rights. Preferred equity, as an equity instrument, typically offers the sponsor more operational flexibility.

Understanding the sponsor's motivation provides you with deeper insight. For more on the sponsor's side of the table, explore our guide on how to raise capital for real estate.

FAQ: Your Preferred Equity Questions Answered

To wrap up, let's tackle some of the most common questions we hear from investors.

Is preferred equity a debt or equity investment?

It’s a true hybrid. It acts like debt by offering a fixed return and holding payment priority over common equity. However, it is legally and structurally an equity investment, sitting on the equity side of the balance sheet, and its repayment is dependent on the project's performance, not secured by a direct lien on the property.

What happens if a project misses a preferred return payment?

This is defined in the operating agreement. If the return is "cumulative," any missed payments accrue and must be paid in full (often with penalty interest) before common equity holders can receive any distributions. In a severe default, the agreement may grant preferred equity holders certain rights, such as the ability to force a sale or take over management.

How is preferred equity taxed?

The tax treatment is highly specific to the deal structure and your personal circumstances. Returns could be treated as portfolio income or capital gains. It is essential to consult a qualified tax advisor to understand the implications before investing.

Can I lose my entire investment in preferred equity?

Yes. While safer than common equity, it is not risk-free. If a project fails and the sale proceeds are only sufficient to cover the senior debt, both preferred and common equity investors can lose their entire principal. This is precisely why the quality, track record, and alignment of the sponsor are the most critical factors in your investment decision.

Well-structured real estate assets, including positions like preferred equity, can be a prudent and resilient component of a long-term wealth strategy. At Stiltsville Capital, we structure offerings with a focus on disciplined underwriting, alignment of interests, and clear risk mitigation.

To discuss how our institutional-grade approach could fit into your portfolio, schedule a confidential call with our team.

Information presented is for educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy securities. Any offering is made only through definitive offering documents (e.g., private placement memorandum, subscription agreement) and is available solely to investors who meet applicable suitability standards, including “Accredited Investor” status under Rule 501 of Regulation D. Investments in private real estate involve risk, including loss of capital, illiquidity, and no guarantee of distributions. Past performance is not indicative of future results.

Comments