Reading Time: 8 min | Good for: Novice Investors (A), Informed Principals (B)

TL;DR: Your Quick Guide to Cap Rate

What It Is: The capitalization (cap) rate is a simple, powerful metric showing a rental property's potential annual return on an all-cash basis. It’s calculated as Net Operating Income (NOI) ÷ Property Value.

Why It Matters: It allows for quick, apples-to-apples comparisons of different properties by removing the variable of financing. It’s your first gut check on price, risk, and relative value.

What's a "Good" Cap Rate? It depends. Lower cap rates (e.g., 4-5%) typically mean lower risk and a higher price. Higher cap rates (e.g., 8%+) suggest higher potential returns but often come with higher risk. Market context is everything.

Investor Action: Use the cap rate as your starting point, but never your only metric. Always dig deeper with a full due diligence checklist and analyze cash-on-cash return and IRR to see the complete picture.

What a Cap Rate Really Tells You About a Rental Property

If you're evaluating a rental property, the cap rate is one of the first, most powerful numbers you'll encounter. It’s a clean metric that shows you a property's potential rate of return before any loans or financing enter the picture. Think of it as the property's raw, unleveraged earning power.

The capitalization rate is the universal language of real estate investing. It's the metric that lets investors quickly size up different properties and compare their income potential on an even playing field.

A great way to think about it is like the yield on a bond. If a bond costs $1,000 and pays you $50 a year, its yield is 5%. The cap rate works the same way. If a rental property generates $50,000 in Net Operating Income (NOI) and is on the market for $1,000,000, its cap rate is 5%.

This simple parallel frames the cap rate perfectly: it’s the unleveraged annual return you’d make if you bought the property with all cash.

Why This One Number Is So Important

This single percentage is your best friend for an initial gut check. It helps you sift through deals quickly without getting lost in the weeds of mortgage details, which are different for every buyer. By removing financing from the equation, the cap rate gives you a pure look at how well the property itself performs.

This is why everyone, from a first-time landlord to an institutional investment firm like Stiltsville Capital, leans on it. It gives you a crucial first impression, helping you answer the big questions right away:

Is the price right? Stacking a property's cap rate against what similar properties have recently sold for (the "market comps") tells you if it's overpriced, underpriced, or right in line with the going rate.

What's the risk level? Generally, a higher cap rate signals a higher potential return, but it often comes with higher perceived risk. A lower cap rate usually points to a safer, more stable asset in a prime location with strong demand.

How does it compare to other deals? When you’re looking at multiple opportunities, the cap rate lets you make a quick, apples-to-apples comparison of their income potential relative to their price tag.

Novice Lens: Why It Matters Don't let the jargon scare you. A cap rate is just a quick health check on a rental property. It tells you how hard your money will work for you based only on the building's ability to make money, making it the perfect starting point for any serious evaluation.

Getting comfortable with this metric is the first step toward building the confidence to analyze deals like a professional. While it's not the only number you'll ever use, it’s without a doubt the most important one to start with.

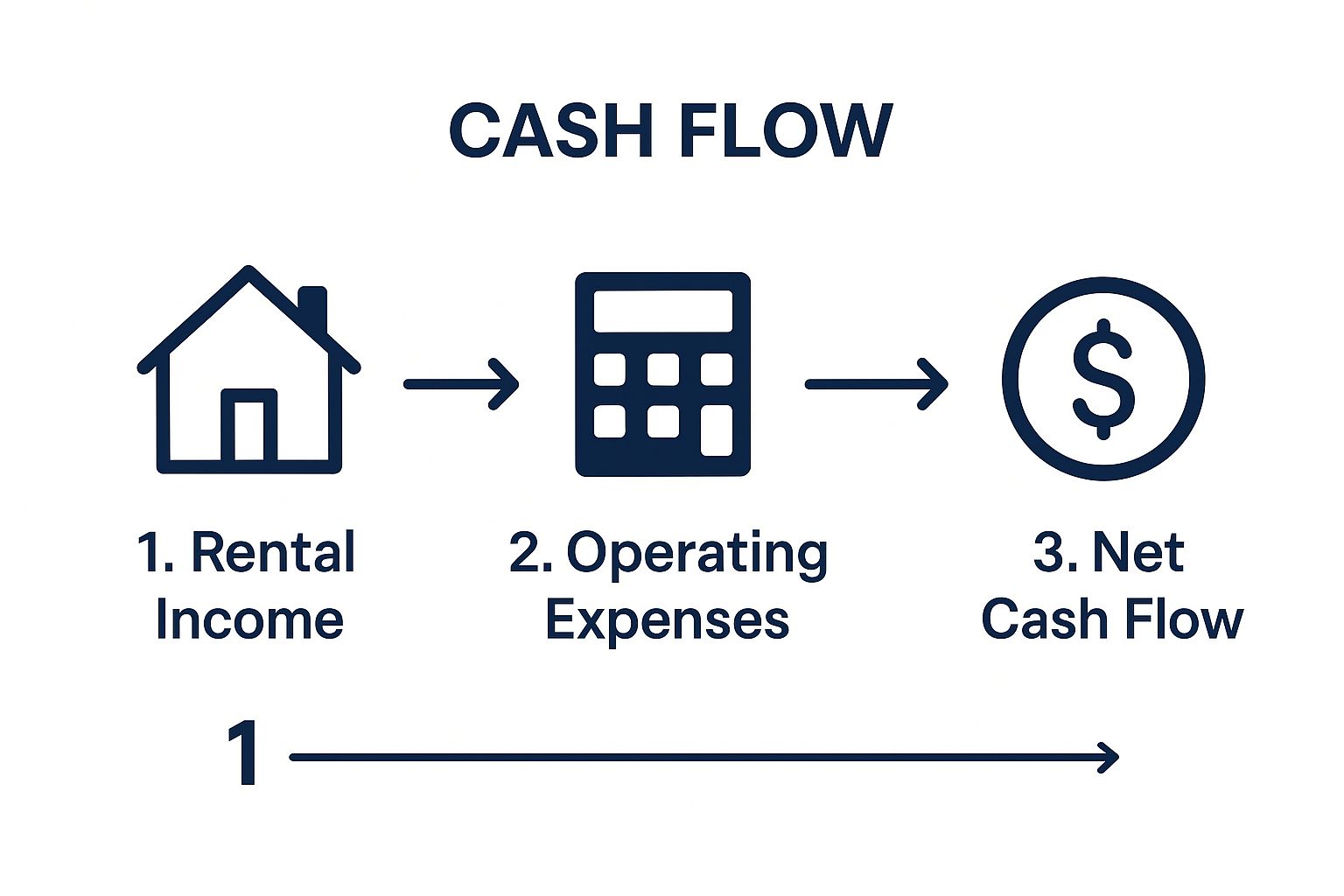

How To Confidently Calculate Cap Rate

Calculating a property's cap rate is straightforward, but the number you get is only as good as the numbers you put in. The formula itself is simple: just divide the property's Net Operating Income (NOI) by its current market value. The real work—and where most investors trip up—is mastering those two inputs, especially the NOI.

This simple visual breaks down the process into three core steps.

As you can see, the heavy lifting happens before you ever do the final division. It's all about nailing down an accurate NOI and a realistic property value.

Mastering Net Operating Income

Think of Net Operating Income (NOI) as the financial heartbeat of a rental property. It’s the total income the property brings in over a year, minus all the necessary operating expenses. Essentially, it’s the property's annual profit before you factor in loan payments (debt service) or income taxes.

Getting this right requires discipline. You have to know exactly what to include and what to leave out.

Income sources to include:

Gross Scheduled Rent (the total rent you'd collect if every unit was occupied 100% of the time).

Other Income from things like parking spots, laundry machines, storage units, or pet fees.

Operating expenses to subtract:

Property taxes

Property insurance

Property management fees

Utilities (if you, the owner, are paying for them)

Routine maintenance and repairs

Landscaping and snow removal

Pest control

General administrative costs

A vacancy allowance (usually 5-10% of gross rent to account for empty units).

A common rookie mistake is confusing NOI with cash flow. True NOI is calculated before debt service. If you include your mortgage payments, you'll artificially crush your NOI and end up with a skewed, inaccurate cap rate.

Deal Lens: Example Of A Multifamily Property

Let's walk through an illustrative example with a hypothetical 10-unit apartment building. This will show you how to build an NOI from the ground up and use it to find the cap rate.

Property Details:

Purchase Price: $2,000,000

Units: 10, each renting for $1,500/month

Step 1: Calculate Annual Income

First, let's figure out the property’s total potential income for the year.

Gross Potential Rent: 10 units x $1,500/month x 12 months = $180,000

Other Income (Laundry/Parking): $5,000 per year

Total Potential Income: $180,000 + $5,000 = $185,000

Now, we must be realistic and account for vacancies. A 5% vacancy allowance is a smart, conservative estimate.

Vacancy Allowance: $185,000 x 5% = $9,250

Effective Gross Income (EGI): $185,000 - $9,250 = $175,750

Step 2: Tally Annual Operating Expenses

Next, we subtract all the costs required to keep the property running smoothly. Here is an illustrative breakdown.

Illustrative Net Operating Income (NOI) Calculation

Effective Gross Income (EGI): $175,750

Property Taxes: ($20,000)

Insurance: ($7,500)

Property Management (8% of EGI): ($14,060)

Repairs & Maintenance: ($10,000)

Utilities (Owner-Paid): ($6,000)

Total Operating Expenses: ($57,560)

Net Operating Income (NOI): $118,190

This step-by-step approach ensures no expense is overlooked and gives us a reliable NOI figure.

Step 3: Calculate NOI And Cap Rate

With our income and expenses locked in, we can finalize the NOI.

Net Operating Income (NOI): $175,750 (EGI) - $57,560 (Expenses) = $118,190

Finally, we plug this into the cap rate formula using the property’s purchase price.

Cap Rate = NOI / Purchase Price

Cap Rate = $118,190 / $2,000,000

Cap Rate = 5.91%

This 5.91% cap rate represents the unleveraged return on the asset. It gives you a clean, simple metric to compare this deal against other investment opportunities. For a deeper dive, check out our definitive investor guide on how to calculate cap rate for real estate.

What a Good Cap Rate Actually Looks Like

Once you have a cap rate, the art is learning how to interpret what that number is telling you about a property's risk, potential, and market position.

The first concept to grasp is the seesaw relationship between cap rates and property values. When one goes up, the other typically comes down.

Low Cap Rate: A low number, say 4-5%, usually points to a higher property value. It often signals a stable, high-quality asset in a prime location with strong tenant demand. The market sees it as a "safe" bet, so investors are willing to pay a premium, accepting a lower initial return.

High Cap Rate: A high cap rate, like 8-10%, suggests a lower property value. This could be a red flag for higher risk—perhaps it's in a less desirable area, needs significant work, or is poorly managed. To take on that risk, investors demand a much higher potential return.

There’s no single "good" cap rate. It all comes down to your investment strategy and risk tolerance. A stable, low-cap-rate property might be perfect for wealth preservation, while a high-cap-rate deal could be a goldmine for a value-add investor skilled in turning properties around.

Factors That Shape Cap Rates

A cap rate isn't created in a vacuum. It’s a living number that reflects powerful forces, from the property itself to the economy at large.

Here are the key drivers:

Property Type: A multifamily complex in a growing city carries a different risk profile than a small retail space with a single tenant. Assets like data centers and medical offices often trade at lower cap rates because they have long-term leases with creditworthy tenants.

Location, Location, Location: An apartment building in a booming Sunbelt city will have a much lower cap rate than an identical building in a town with a shrinking population. Proximity to jobs, transportation, and amenities directly impacts perceived risk.

Economic Tailwinds: Macroeconomic factors, especially interest rates, play a massive role. When interest rates climb, borrowing gets more expensive. This puts upward pressure on cap rates because investors need higher returns to justify the deal.

We've seen this play out in U.S. multifamily apartments. After the Global Financial Crisis, cap rates were high due to risk aversion. As the economy recovered and rates fell, cap rates compressed, hitting all-time lows around 4.1% in 2021. By early 2024, Fed rate hikes had pushed them back up toward 5.2%, proving their sensitivity to financial conditions.

The Art of Cap Rate Compression

For savvy investors, the cap rate isn’t just an analytical tool—it’s a target. A powerful value-add strategy is built around "cap rate compression." The goal is simple: buy a property at a high cap rate, improve its operations and physical condition, and force the cap rate down. This directly increases the property's value.

Here’s how it works: An investor buys an older, C-class apartment building at an 8% cap rate. It’s underperforming because the units are dated and management is inefficient. 1. Execute the Plan: They invest capital to renovate apartments, add modern amenities, and bring in professional managers. This allows them to raise rents and cut wasteful spending, boosting the Net Operating Income (NOI). 2. Force Appreciation: Two years later, the property is a desirable B-class asset with a much healthier NOI. The market now sees it as a less risky, more stable investment. 3. Exit at a Lower Cap Rate: The investor can now sell the property at a 6% cap rate. That combination of a higher NOI and a lower exit cap rate creates a massive increase in the property's sale price—and a significant win for investors.

This strategy is the engine behind countless successful real estate deals. For a deeper look at market benchmarks, check out our complete guide on what is a good cap rate for real estate investors.

Finding Your Bearings with Market Benchmarks

A cap rate by itself is just a number; it’s meaningless without context. A 5% cap rate for a rental property could be a steal in a bustling downtown core but a red flag in an unproven market. To make smart decisions, you must ground your analysis in reality by looking at what similar properties are trading for.

This is where you need to tap into institutional-grade data. Reports from industry heavyweights like CBRE and JLL provide that crucial perspective, laying out typical cap rate ranges for different commercial real estate sectors.

Mapping Cap Rates Across Asset Classes

Not all properties are created equal, and their risk and return profiles are reflected in their cap rates. A brand-new, fully leased Class A apartment building will almost always trade at a lower cap rate than a value-add industrial warehouse that needs work.

Here are some general benchmark ranges to get you started (as of mid-2024):

Multifamily: Typically 5.0% - 5.75%. This sector is a favorite due to consistent tenant demand, making it a lower-risk play.

Industrial/Warehouse: Often 5.5% - 6.5%. Fueled by e-commerce, logistics and warehouse space has been a top performer.

Retail (Neighborhood/Service): Usually 6.75% - 7.5%. Higher cap rates reflect the added risks and ongoing shifts in the retail landscape.

Medical Office: Can be 6.0% - 7.0%. Investors value these for their stable, high-credit tenants in the resilient healthcare industry.

Remember, these are broad averages. Rates can swing wildly depending on the city, neighborhood, and building quality. The key is to compare your target property to its direct competition.

Understanding Historical Cap Rate Cycles

Cap rates move with the economy and credit markets. The sharpest investors don't just look at today's numbers; they study historical trends to understand where we are in the cycle.

Historically, cap rates fluctuate within a somewhat predictable range. A deep dive into historical data on cap rates and real estate cycles shows the long-run average for institutional real estate hovers around 7.6%. During boom times, like from 2003-2007, a flood of capital pushed cap rates down. Then, when the 2007-2009 financial crisis hit, credit dried up and cap rates shot up as property values tumbled.

Market Signal Box: Cap Rate Expansion (Q2 2024) * The Signal: Market reports from mid-2024 show "cap rate expansion" across the board. In simple terms, cap rates have been climbing from the historic lows seen a few years ago. * The Driver: This shift is almost entirely due to the Federal Reserve's higher interest rate policy. When it costs more to borrow, investors demand a higher initial return—a higher cap rate—to make a deal pencil out. * Investor Take: This is a double-edged sword. Rising cap rates can pressure the value of properties you already own. But for buyers with capital ready to deploy, it's a significant opportunity. This environment allows disciplined investors to acquire high-quality assets at more attractive initial yields than what was possible just 24 months ago.

Recognizing the Limits of Cap Rate Analysis

To build a resilient investment portfolio, you have to know the limits of your tools. The cap rate for rental property is a brilliant first-glance metric—a snapshot of a property’s raw earning power. But treating this snapshot as the full picture is a critical error.

Relying solely on cap rates is like driving a car by only looking in the rearview mirror. It tells you where the property stands today but offers zero insight into where it's headed.

The Static Nature of a Dynamic Investment

A cap rate's biggest weakness is that it's a static calculation for a dynamic asset. Real estate performance evolves. A simple cap rate calculation fails to account for critical value drivers that sophisticated investors focus on.

These blind spots include:

Future Rent Growth: Does the local market support rent increases? A property in a high-growth corridor has a much brighter future than one in a stagnant area—a detail the current cap rate won't reveal.

Changes in Vacancy: A new employer moving to town could slash vacancy rates and boost future income. Conversely, a major employer leaving could do the opposite.

The Power of Financing: Cap rates are unleveraged. They completely ignore how smart debt can magnify returns. A property with a modest 6% cap rate could deliver a stellar 15% cash-on-cash return with the right financing.

Value-Add Potential: The cap rate reflects the property as-is. It doesn’t capture the upside a skilled sponsor can unlock through renovations, better management, or repositioning the asset.

Debunking a Common Myth: Higher Is Not Always Better

New investors often fall into the trap of chasing the highest possible cap rate, assuming it automatically equals a better deal. This can be a costly mistake. An unusually high cap rate is often a warning sign—a signal of distress, a bad location, deferred maintenance, or unstable tenancy.

A lower cap rate on a well-located, professionally managed asset can often produce superior long-term, risk-adjusted returns than a high-cap-rate property with a mountain of hidden problems.

Experienced sponsors hunt for properties where the current cap rate doesn't reflect the potential NOI after a strategic business plan is executed.

Risk & Mitigation in Cap Rate Analysis

Risk: Market Blindness * Mitigation: Conduct in-depth market analysis on job growth, population trends, and new supply. A static cap rate won't warn you of a looming oversupply issue.

Risk: Ignoring Property Condition * Mitigation: Perform thorough due diligence, including physical inspections and capital expenditure projections. A high cap rate might be masking a money pit.

Risk: Overlooking Tenant Quality * Mitigation: Analyze the rent roll for tenant creditworthiness, lease terms, and expiration dates. A building full of tenants on month-to-month leases is riskier.

Risk: Miscalculating Future Potential * Mitigation: Build a dynamic financial model (pro forma) that projects cash flows over the entire hold period, factoring in rent growth, renovations, and exit strategy.

By moving beyond a single number, investors can paint a much more realistic picture of a property's true potential.

Looking Beyond Cap Rate: The Investor's Toolkit

To get the full story, disciplined investors layer their analysis with other key performance indicators.

Cash-on-Cash Return: This metric shows the annual pre-tax cash flow relative to the total cash invested. It’s a powerful measure of how hard your actual invested capital is working, incorporating the effects of leverage.

Internal Rate of Return (IRR): The IRR calculates the total annualized return over the entire investment holding period, factoring in your initial investment, ongoing cash flows, and the final sale. It gives a holistic view of profitability over time.

In 2024, cap rates expanded significantly across major commercial real estate sectors. As noted by the CFA Institute blog, the U.S. multifamily sector saw a rise of approximately 195 basis points, reflecting higher financing costs and a broad adjustment in property valuations. To learn more, read our guide on the capitalization rate formula for real estate.

Your Cap Rate Due Diligence Checklist

Analysis is one thing; action is another. A cap rate is only as good as the assumptions behind it, and a smart investor knows what to ask to get the real story. Before you commit to a rental property deal, use this checklist to guide your conversation with the deal sponsor.

Think of these questions as a way to peel back the layers of the pro forma and stress-test the investment thesis.

Scrutinizing the Numbers

First, validate the building blocks of the cap rate—the NOI and the property's value. This ensures your baseline is solid.

How did you calculate the NOI? Ask for a detailed breakdown of every income and expense item. Are one-time fees juicing the income? Are major maintenance items conveniently omitted?

What vacancy rate did you assume? See if the assumed rate matches the property's history and local market comps. An overly optimistic vacancy assumption is a classic way to inflate NOI.

Are there any major capital projects planned that aren't in the operating budget? A planned roof replacement or HVAC overhaul are critical costs to understand the property's true cash needs.

Investor Takeaway: A sponsor's answers reveal their discipline. Clear, conservative assumptions mark a seasoned operator. Vague answers or aggressive projections are a major red flag.

Understanding the Market and Exit Strategy

A deal's success depends on its future. The exit cap rate is one of the most important assumptions in any model as it determines the projected sale price.

How does this cap rate compare to recent, verified sales of similar properties in this submarket? Ask for specific "comps." If their number is an outlier, they need a compelling explanation.

What's the projected exit cap rate? A responsible sponsor will almost always underwrite a higher (more conservative) exit cap rate than their entry cap. This builds in a cushion for market changes.

What specific steps in the business plan will improve the NOI? You're looking for an actionable plan—specific renovations, new amenities, or better management—not just hope for "market improvement."

Asking these questions helps you confirm the story behind the numbers and ensures the cap rate for a rental property represents a real opportunity.

Got Questions About Cap Rates? We've Got Answers.

To wrap up, let's tackle a few common questions that arise when investors start using cap rates to analyze deals.

How Do Interest Rates Affect Cap Rates?

Think of cap rates and interest rates as dance partners—they usually move in the same direction. When the Federal Reserve hikes interest rates, loans get more expensive. To make a deal work with pricier financing, investors need a better initial return. This pressures sellers to lower their asking price, which in turn pushes cap rates higher. Conversely, when interest rates drop, borrowing gets cheaper, and cap rates often compress lower.

Can a Cap Rate Be Negative?

Technically, yes, but it’s a massive red flag. A negative cap rate means the property is spending more on operating expenses than it’s bringing in from rent. In plain English, the property is bleeding cash before the mortgage is even considered. An asset like this is not just failing to produce income; it's actively draining money. While a bold value-add plan might target a property with a razor-thin cap rate, a negative one screams "deep financial trouble."

Which Price Should I Use in the Formula?

For an accurate picture, always use the property's current market value or a recent, comparable sales price. Don't get distracted by the seller's listing price. A listing price is just an optimistic starting point. Basing your analysis on an inflated asking price will give you an artificially low cap rate, making a potentially good deal look terrible. Ground your numbers in reality.

At Stiltsville Capital, we believe that disciplined underwriting is the key to building lasting wealth in real estate. When you truly understand metrics like the cap rate, you are in a much stronger position to identify and secure high-quality investment opportunities that align with a prudent, long-term wealth strategy.

If you’d like to learn more about our approach and see our current offerings, we invite you to schedule a confidential call with our team.

Information presented is for educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy securities. Any offering is made only through definitive offering documents (e.g., private placement memorandum, subscription agreement) and is available solely to investors who meet applicable suitability standards, including “Accredited Investor” status under Rule 501 of Regulation D. Investments in private real estate involve risk, including loss of capital, illiquidity, and no guarantee of distributions. Past performance is not indicative of future results.