Reading Time: 7 min | Good for: Novice (A), Informed (B)

TL;DR: Key Takeaways on Finding Cap Rate

The Formula: To find a property's cap rate, divide its Net Operating Income (NOI) by its Current Market Value ().

Why It Matters: This simple calculation provides a crucial, unlevered snapshot of a property's potential annual return, allowing for quick, apples-to-apples comparisons between investment opportunities.

The "Good" Rate Myth: A "good" cap rate is relative. Lower rates (e.g., 4-5%) typically signal lower risk and higher quality assets, while higher rates (e.g., 8%+) suggest higher risk but potentially greater returns.

Next Step: Mastering the cap rate is the first step. The next is understanding how it fits into a broader due diligence process to identify resilient, institutional-quality real estate investments.

The Core Formula for Valuing Property

For any serious real estate investor—from a family office principal to someone making their first passive allocation—the capitalization rate, or cap rate, is a fundamental tool. It cuts through the noise to offer a clear look at a property's profitability relative to its price. While it's just one piece of the puzzle, it’s often the first question asked when a deal hits the table.

To use it effectively, you must get the two main ingredients right. The formula, Cap Rate = NOI / Market Value, is only as good as the numbers you plug into it.

Net Operating Income (NOI): This is all the cash the property generates from rents and other fees after you subtract all necessary operating expenses like taxes, insurance, and routine maintenance. Crucially, NOI excludes debt payments (mortgage) and major capital projects.

Current Market Value: This is straightforward—it’s either the property’s asking price or what it’s estimated to be worth today based on what similar properties ("comps") have recently sold for.

To get the NOI right, you need a clear-eyed view of the property's income and expenses. Here’s a quick breakdown of what goes into that calculation.

Net Operating Income (NOI) at a Glance

Component | Description | Example Item |

|---|---|---|

Gross Potential Income | The total rent you could collect if the property were 100% occupied. | Scheduled monthly rent x 12 |

Vacancy & Credit Loss | An allowance for periods when units are empty or tenants don't pay. | A percentage of Gross Income (e.g., 5%) |

Effective Gross Income | The realistic income after accounting for vacancies. | Gross Income - Vacancy Allowance |

Operating Expenses | The day-to-day costs of running the property (excluding debt). | Property taxes, insurance, utilities, repairs |

Net Operating Income | The property's total profit before mortgage payments. | Effective Gross Income - Operating Expenses |

Once you have a credible NOI, you're ready to see how it relates to the property's value.

The Inverse Relationship

The calculation itself is direct, but its implications are what really matter. Cap rates and property values move in opposite directions—it's an inverse relationship.

For example, a property with a $500,000 NOI that’s valued at $10 million has a 5% cap rate. But if market sentiment shifts and similar properties start trading at an 8% cap rate, that same $500,000 NOI now suggests a market value of only $6.25 million. This dynamic is at the very heart of real estate valuation.

Novice Lens: Why It MattersA lower cap rate usually points to a higher-quality, lower-risk asset in a prime location. Investors are willing to pay a premium for stability. Conversely, a higher cap rate often signals more perceived risk or a less desirable market—but it could also mean a bigger potential payoff for those willing to take on the challenge.

For a foundational understanding of this crucial metric, check out this detailed guide on What Is Cap Rate in Real Estate. Getting this concept down is the first step toward disciplined underwriting and spotting true value in the market.

Nailing Your Net Operating Income

The cap rate formula is simple, but its results are only as reliable as the numbers you use. This is where Net Operating Income (NOI) comes in, and frankly, it's everything. NOI tells the true financial story of a property, and it's where an undisciplined seller can easily make a deal look much better on paper than it is in reality.

Getting this number right is the most critical part of the entire process. An accurate NOI starts with the property’s total potential revenue.

From Gross Income to Effective Income

First, you determine the Gross Potential Income (GPI). Think of this as the perfect-world scenario—it’s the total annual rent you'd pocket if every unit was occupied and every single tenant paid on time, all year long.

But we don't invest in a perfect world. The next step is to bring that GPI down to earth by subtracting an allowance for vacancy and credit loss. This accounts for the inevitable empty units or tenants who don't pay. What you're left with is the Effective Gross Income (EGI), a much more honest picture of the cash that actually hits the bank.

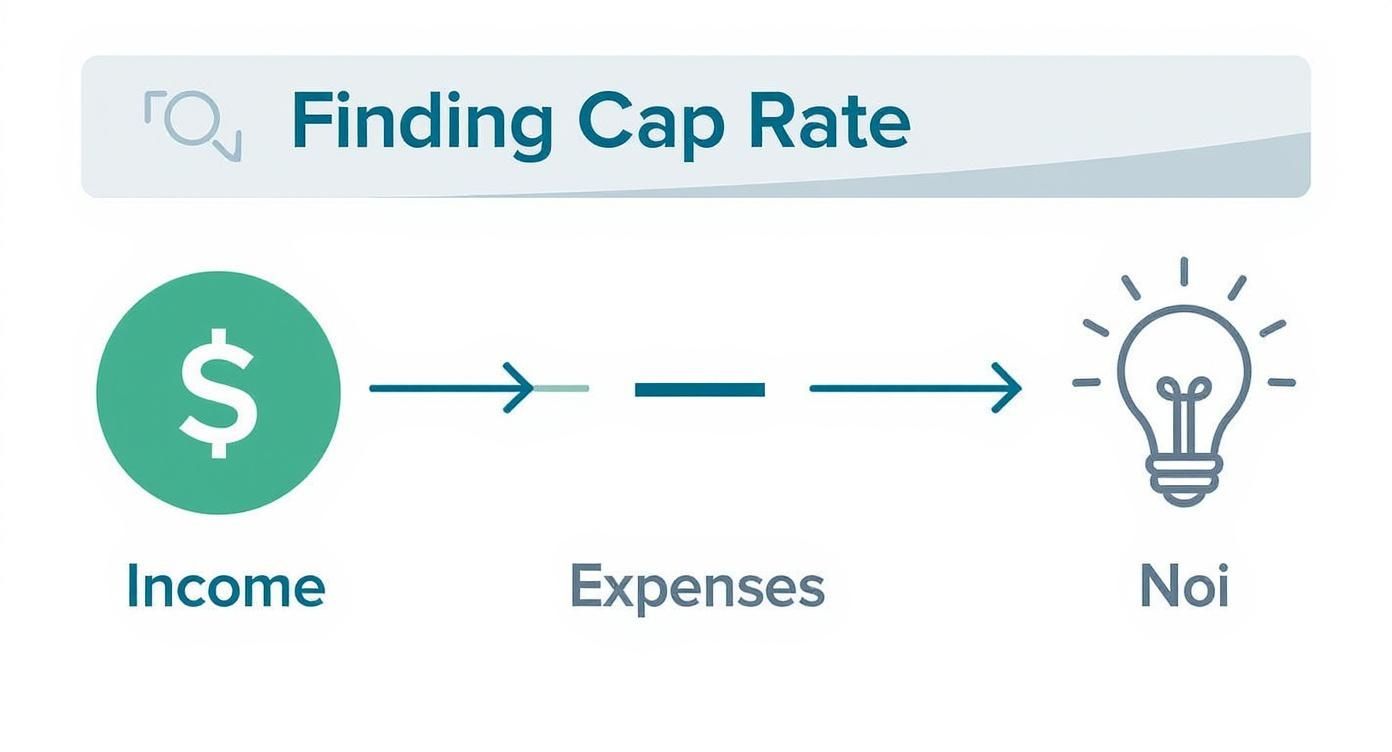

This flow from pie-in-the-sky potential to real-world income is a foundational concept you have to master.

The infographic above breaks it down visually, showing how you methodically peel away the property's costs from its income to get to that all-important number: the NOI.

Subtracting the Right Operating Expenses

Once you have your EGI, it's time to subtract the legitimate operating expenses. These are the recurring, necessary costs of keeping the property running. Your typical list will include:

Property Taxes

Insurance Premiums

Property Management Fees

Utilities (if paid by owner)

Routine Repairs & Maintenance

Admin and Marketing Costs

Knowing what not to include is just as important. New investors often make the mistake of subtracting costs that aren't true operating expenses. Make sure you exclude debt service (your mortgage payments), major capital expenditures (like a new roof), and depreciation. If you want to dive deeper into this crucial step, check out our guide on how to find net operating income.

Advanced Lens: Pro Forma vs. Trailing Twelve (T12)A seller will often present a "pro forma" NOI. This is a forward-looking forecast that usually bakes in optimistic assumptions, like immediate rent hikes or magically lower expenses. A sophisticated investor or family office will always demand the "trailing twelve" (T12) financial statement. The T12 shows the actual, verifiable income and expenses over the last 12 months. Always underwrite your deal based on the T12, not the seller's pro forma fantasy.

To really get a handle on metrics like cap rate, you first have to master the inputs. For another great resource on this, take a look at this guide on how to calculate income from operations.

Alright, you’ve got your Net Operating Income nailed down. You’re halfway there.

The final piece of the puzzle is the property's market value—the denominator in our cap rate formula. In simple terms, this is what a willing buyer would realistically pay a willing seller on the open market.

If you're in the process of buying a property, this part is easy. The market value is your purchase price. But what about a potential deal you're sizing up, or an asset you already own? That’s when you have to determine its value based on what the market is paying for similar properties right now.

Using Comps to Find a Market Cap Rate

This is where comparable sales—or "comps," as they are known in the business—are absolutely essential. You cannot value a property in a vacuum. You must dig in and research recent sales of similar assets: same property type, class, and size, all within the same local submarket.

This research uncovers the prevailing market cap rate, which is the rate investors are currently willing to accept for that specific level of risk and return in that area. It's more than just finding one number; it’s about analyzing several deals to get a solid benchmark. For a deeper dive, check out our complete guide to real estate property valuation methods for investors.

Deal Lens Example: Multifamily AcquisitionLet's say you're analyzing a 100-unit multifamily property with a verified T12 NOI of $600,000. To pin down its value, your team finds three recent, comparable sales in the submarket:* Comp A: Sold for $11.5M at a 5.2% cap rate.* Comp B: Sold for $12.2M at a 5.0% cap rate.* Comp C: Sold for $10.8M at a 5.4% cap rate.This data tells you the market is trading around a 5.2% cap rate for this asset quality. By applying this to your target property’s NOI ($600,000 / 0.052), you can estimate its market value at $11.54 million. If the seller is asking for significantly more, you now have the data to back up a lower offer—or to know when it’s time to walk away.

Recent market shifts drive home why this analysis is so critical. According to Statista, U.S. multifamily cap rates climbed from a low of about 3.82% in 2021 to around 5.96% in 2023, largely because borrowing costs shot up. You can find more insights on these multifamily property cap rate trends on Statista.com. This kind of movement directly impacts property valuations, making up-to-date comp analysis a non-negotiable part of any serious deal underwriting.

How to Interpret a "Good" Cap Rate

Figuring out the cap rate is just math. Understanding what it means is the real skill. There's no magic number for a "good" cap rate—it all comes down to your investment objectives, risk tolerance, and the specifics of the market you're targeting.

The most important concept to grasp is the relationship between cap rates and risk. A low cap rate means a high price relative to the income it generates. Investors are only willing to pay such a premium for assets they see as rock-solid: safe, stable properties in prime locations with strong credit tenants. Think of a brand-new apartment building in a major gateway city.

On the flip side, a high cap rate is a signal that investors demand a bigger payday for taking on more risk. That risk could come from a property in a tertiary market, an older building needing significant capital improvements, or a local economy with shaky fundamentals.

Benchmarking Across Asset Classes

You can't compare apples to oranges, and the same goes for property types. Different assets trade at different cap rates because their risk profiles are fundamentally different. A shiny, new multifamily complex filled with tenants on long-term leases is a world away from a hotel that depends on nightly bookings and seasonal tourism.

Your strategy plays a huge role, too. A stabilized, "Core" property will always have a lower cap rate than an opportunistic "Value-Add" deal that needs a complete overhaul and a risky lease-up period.

Investor Takeaway: Don't just chase the highest cap rate. Instead, ask what that number is really telling you about the property's underlying risk. A 4.5% cap might be a fantastic return for a trophy asset in a supply-constrained market, while an 8% cap on a poorly located building could be a major red flag.

The table below lays out some general cap rate ranges you might see across different property types. It's a useful starting point for when you're analyzing deals.

Illustrative Cap Rate Ranges by Property Type

This table gives a ballpark idea of how cap rates can differ based on the type of commercial property. Keep in mind these are for illustrative purposes—actual rates will always depend on the specific market, asset quality, and the prevailing economic climate.

Property Type | Typical Risk Profile | Illustrative Cap Rate Range |

|---|---|---|

Multifamily | Low to Moderate | 4.5% – 6.0% |

Industrial / Logistics | Low to Moderate | 5.0% – 6.5% |

Retail (Grocery-Anchored) | Low to Moderate | 5.5% – 7.0% |

Office (Class A) | Moderate | 6.0% – 7.5% |

Self-Storage | Moderate | 5.5% – 7.0% |

Medical Office | Low to Moderate | 5.5% - 7.0% |

Hospitality (Hotel) | High | 7.5% – 9.0%+ |

Ultimately, these ranges show how the market prices risk. A lower-risk asset like a well-located multifamily building commands a premium (and thus a lower cap rate), while a higher-risk hotel needs to offer a better potential return to attract investors. Use this as a guide, but always perform your own deep-dive analysis.

Beyond the Formula: The Forces That Move Cap Rates

Any seasoned investor will tell you that the cap rate isn't a static number calculated in a vacuum. The real art is understanding the powerful market forces constantly pushing it up or down. It’s a perpetual tug-of-war between capital markets and on-the-ground property performance.

Often, the single biggest influence is the cost and availability of debt. When interest rates climb, borrowing becomes more expensive. This almost always puts upward pressure on cap rates because investors demand higher yields to make their deals pencil out. This intricate dance between borrowing costs and property yields is a core concept, and you can dive deeper into how lower interest rates can be a catalyst for commercial real estate investment.

Local Market Dynamics

But it’s not all about national interest rate trends. What’s happening on the street corner matters just as much. Strong local job growth, for instance, can fuel massive demand for apartments or office space, leading to expectations of higher rent growth.

When investors are optimistic, cap rates can compress (go down) because they’re willing to pay more today for the promise of more cash flow tomorrow. On the flip side, if a flood of new construction hits a submarket, vacancy rates can creep up and put a ceiling on rents. That perceived risk can cause cap rates to expand (go up).

These forces have created cycles for decades. As NAIOP has reported, back in the mid-1980s, you’d typically see commercial property cap rates floating between 5.5% and 8.0%. More recently, institutional-grade real estate cap rates have tended to hover around a long-term average near 7.6%. You can discover more insights on these historical trends on NAIOP.org.

Myth vs. Reality: Cap Rate as a Total Return MetricMyth: A property's cap rate is its total return.Reality: This is one of the most common and costly mistakes new investors make. A cap rate is a one-year snapshot of your unlevered yield. It tells you nothing about future rent growth, appreciation, or the powerful impact of leverage. An investor's true total return—often measured by the Internal Rate of Return (IRR) or Equity Multiple—accounts for all these factors over the entire hold period.

Unpacking the Nuances: Your Cap Rate Questions Answered

Even sophisticated investors get hung up on the details when a deal is on the line. Let's clear up a few common questions that arise when calculating and using cap rates in the real world.

Is a Cap Rate the Same as a Cash-on-Cash Return?

No, and confusing the two can completely skew your analysis. Think of it this way: a cap rate is an unlevered metric. It shows a property's earning power in a vacuum, ignoring any financing.

A cash-on-cash return, on the other hand, is a levered metric. It tells you the return you’re making on the actual cash you invested, after you’ve made your mortgage payments. Both are crucial, but they paint very different pictures of a deal's performance.

How Should I Factor Capital Expenditures into the NOI?

This is a classic debate. By the book, true Net Operating Income (NOI) excludes major capital expenditures (CapEx) like replacing a roof or HVAC system. But simply ignoring these big-ticket items is a rookie mistake.

Disciplined investors account for this by deducting a "replacement reserve" from their NOI. This is an annualized estimate set aside for future CapEx. It’s a simple move that produces a more honest, long-term picture of the property's true cash flow potential.

Is a Higher Cap Rate Always Better?

Not at all. A high cap rate might catch your eye, but more often than not, it's a red flag signaling higher risk. A juicy cap rate can be a sign of trouble—perhaps the property is in a declining market, has significant deferred maintenance, or is filled with non-credit tenants. A lower cap rate, while less exciting upfront, usually points to a safer, more stable asset in a desirable location. The "best" cap rate is the one that aligns with your risk tolerance and overall investment strategy.

Questions to Ask a Sponsor About Cap Rates

Before investing in a deal, here are five crucial questions to ask the sponsor about their cap rate assumptions:

Is the entry cap rate based on T12 actuals or a pro forma budget?

What comparable sales were used to determine the market cap rate, and how similar are they?

What is the assumed exit cap rate, and how does it compare to the entry cap rate?

What are the key drivers (rent growth, expense reduction) that are projected to lower the effective cap rate over the hold period?

What macroeconomic factors (interest rate changes, local job growth) could cause the exit cap rate to be higher than projected?

Ready to move beyond theory and see how these principles apply to institutional-grade deals? The team at Stiltsville Capital can help you analyze real-world opportunities in today's most promising markets. We believe that well-structured real assets can be a prudent, resilient component of any long-term wealth strategy.

Information presented is for educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy securities. Any offering is made only through definitive offering documents (e.g., private placement memorandum, subscription agreement) and is available solely to investors who meet applicable suitability standards, including “Accredited Investor” status under Rule 501 of Regulation D. Investments in private real estate involve risk, including loss of capital, illiquidity, and no guarantee of distributions. Past performance is not indicative of future results. Verification of accredited status is required for participation in Rule 506(c) offerings.