A Guide to Appraisal Methods in Real Estate: Underwriting for Value

- Ryan McDowell

- Nov 28, 2025

- 15 min read

Reading Time: 8 min | Good for: Novice, Informed, and Sophisticated Investors

When you're trying to figure out what a piece of real estate is really worth, it's not about pulling a number out of thin air. For sophisticated investors and sponsors like Stiltsville Capital, the final figure is always the product of rigorous, data-driven analysis, not guesswork. The most common appraisal methods in real estate boil down to three core frameworks: the Sales Comparison Approach, the Income Approach, and the Cost Approach.

TL;DR: Key Investor Takeaways

Three Core Lenses: Real estate valuation rests on three pillars: what similar properties have sold for (Sales Comparison), how much income it can generate (Income), and what it would cost to build (Cost).

Strategy Dictates Method: The right appraisal method depends on the deal. Stabilized assets lean on Sales and Income (Direct Cap), while value-add or development deals require a forward-looking Discounted Cash Flow (DCF) and Cost Approach analysis.

Assumptions Matter Most: A valuation is only as good as its inputs. Scrutinizing a sponsor's assumptions on rent growth, exit cap rates, and construction costs is more important than the final number itself.

Getting a handle on these pillars is the first step toward the kind of disciplined underwriting that uncovers genuine value and protects investor capital.

Understanding The Three Pillars of Real Estate Valuation

Here at Stiltsville Capital, every single potential acquisition—whether it’s an adaptive reuse project or a ground-up modular multifamily development—starts with one critical question: "What is this asset truly worth?"

The answer isn't a single number. It’s a carefully reconciled conclusion, drawn from one or more of these time-tested appraisal methods. They provide a structured way to determine a property's market value, which is absolutely essential for everything from securing financing and negotiating purchase prices to projecting investor returns.

Think of them as different lenses. Each one gives an appraiser or investor a unique view of a property, and by combining those views, you get a complete and defensible opinion of value. If you want to dive deeper into the professional techniques, resources like this guide on Mastering Real Estate Property Valuation Methods are incredibly helpful.

The Core Valuation Frameworks

While each approach has its own nuances (which we’ll get into), the fundamental logic is pretty straightforward. They represent the three primary ways to think about an asset’s value:

What have similar properties sold for? This is the heart of the Sales Comparison Approach.

How much income can the property generate? This is the question that drives the Income Approach.

What would it cost to build it from scratch? This is the core idea behind the Cost Approach.

These three methods have dominated appraisal practices across the globe for decades, and for good reason. Market analysis from the Appraisal Institute shows the sales comparison approach is still the most widely used, especially for residential properties. For commercial assets, a blend of all three is common, with the Income Approach often taking precedence.

At a Glance Overview of Core Appraisal Methods

To make it simple, we've broken down these foundational pillars into a quick summary table. This gives you a snapshot of how each method works and where it shines.

Appraisal Method | Core Principle | Best For | Key Data Inputs |

|---|---|---|---|

Sales Comparison | Value is derived from recent sales of similar properties. | Single-family homes, condos, and properties with ample comparable sales data. | Recent sales prices, property characteristics, location, market conditions. |

Income Approach | Value is based on the property's ability to generate income. | Commercial real estate (multifamily, retail, office), investment properties. | Net Operating Income (NOI), capitalization rates, cash flow projections. |

Cost Approach | Value is the cost to build a new equivalent property, minus depreciation. | New construction, unique assets (e.g., schools, churches), insurance valuation. | Land value, construction costs, depreciation estimates (physical, functional). |

This table provides a high-level overview, but the real magic happens when you know which method to apply, how to source the right data, and how to make the necessary adjustments—which is exactly what we'll explore next.

A Deep Dive into the Sales Comparison Approach

Of all the appraisal methods out there, the Sales Comparison Approach is the most intuitive. Often called the "market approach," its logic is incredibly straightforward: a property is worth what similar properties have recently sold for.

This method is the backbone of almost every residential valuation and a go-to for commercial assets when you’ve got enough solid transaction data. The appraiser's job is to hunt down recently sold properties—known as comparables or “comps”—that are as close a match as possible to the asset being valued, the "subject property."

But finding the comps is just the start. The real skill is in making precise, defensible adjustments for the inevitable differences between the comps and the property you're analyzing.

Selecting the Right Comps

Getting the comps right is everything. A good appraiser doesn't just pull up any old property that sold in the area; they use a strict set of criteria to make sure the comparison is relevant and apples-to-apples.

Here’s what they look for:

Proximity: The closer the comp, the better. A property across the street reflects the same neighborhood influences, while one across town might not.

Recency of Sale: Markets move fast. A sale from six months ago is a solid data point; one from three years ago is practically ancient history.

Physical Similarity: Comps should be close in size (square footage), age, design, and overall condition. You can't compare a brand-new build to a teardown.

Legal Characteristics: Things like zoning and land use have to line up to provide a meaningful benchmark.

Novice Lens: Why This Matters for Your HomeThink about how a real estate agent prices your house. They’ll find three or four homes in your neighborhood that sold in the last 90 days. If an almost identical house next door just sold for $500,000, that’s your baseline. But if your kitchen is brand new and theirs wasn't, an appraiser will add value. If their place had a pool and yours doesn't, they'll adjust your home's value down.

The Art of Adjustments

Since no two properties are ever truly identical, appraisers must adjust the sale prices of the comps to account for the differences. If a comparable property is superior in some way—say, it has an extra bathroom—its sale price is adjusted downward. If it's inferior—maybe it sits on a smaller lot—its price is adjusted upward to level the playing field.

Common adjustments fall into a few key categories:

Location: Even one street over can make a big difference in desirability.

Financing Terms: A sale involving special seller financing might not reflect the true market value.

Condition of Sale: An arm's-length transaction is crucial. A sale between family members, for example, is likely skewed.

Physical Features: Every difference matters—square footage, amenities, construction quality, and age all require careful adjustments.

After all this, you get an "adjusted sales price" for each comp. The appraiser then reconciles these adjusted prices, giving more weight to the comps they feel are the closest match, to land on a final value for the subject property.

The Challenge of Unique Assets

The Sales Comparison Approach shines in active markets with plenty of transaction data, like workforce multifamily housing. But it gets tricky when you're dealing with unique or thinly traded assets where good comps are few and far between.

Sophisticated Lens: The Data Center DilemmaImagine trying to value a hyperscale data center in a secondary market. Good luck finding three similar facilities that sold nearby in the last year. It’s nearly impossible. One potential "comp" might be older with lower power density, another might have a less creditworthy tenant, and a third could be in a different state entirely. In cases like this, appraisers have to cast a much wider net and make significant, complex adjustments. This is where the Sales Comparison Approach starts to lose its punch, and investors at Stiltsville Capital lean more heavily on the Income or Cost approaches. For these tough cases, data sources like CoStar and Real Capital Analytics are absolutely vital for finding even distant comparables.

Mastering The Income Approach for Investment Properties

While the Sales Comparison Approach looks backward, the Income Approach looks to the future. For any serious commercial real estate investor, this is the most important valuation method in the toolkit. It cuts right to the chase, answering the one question that truly matters: "How much cash will this asset actually produce?"

This is the language of real estate finance. It treats a property less like a physical structure and more like what it is—a business designed to generate a return. Under the Income Approach umbrella, there are two techniques we live and breathe: Direct Capitalization and Discounted Cash Flow (DCF) analysis.

Direct Capitalization: The Investor Snapshot

Think of Direct Capitalization as a quick, powerful way to gauge a property's value based on a single year of its income. It’s a snapshot in time. This makes it perfect for stabilized assets with predictable income streams, like a fully occupied apartment building with a solid history of rent collection.

The formula is beautifully straightforward:

Value = Net Operating Income (NOI) / Capitalization Rate (Cap Rate)

Net Operating Income (NOI) is the property's yearly income after you've paid all the operating expenses but before accounting for mortgage payments or income taxes. Nailing down an accurate NOI is the bedrock of any credible valuation.

The Capitalization Rate (Cap Rate) is the expected annual return an investor would get if they bought the property with all cash. We find this number by looking at what similar properties in the market recently sold for and what their NOIs were. A lower cap rate usually means lower risk and a higher price tag, while a higher cap rate signals more risk and thus a lower valuation.

Discounted Cash Flow: The Strategic Forecast

But what about properties that aren't stabilized? For a value-add project, a ground-up development, or anything with a story still unfolding, a single year's income just doesn't cut it. This is where Discounted Cash Flow (DCF) analysis becomes absolutely vital.

A DCF projects all of a property's expected cash flows over a specific holding period—typically 5-10 years—and includes the final payout from its sale. Each of those future cash flows is then "discounted" back to what it's worth today, because a dollar tomorrow is worth less than a dollar in your hand now.

This forward-looking model is the engine behind how firms like Stiltsville Capital underwrite our opportunistic and value-add deals. It allows us to build a financial model that shows the real impact of our business plan, whether that’s renovating units, pushing rents to market, or tightening up operations. For a deeper look into this crucial technique, you can explore our guide on how to calculate a discounted cash flow for real estate success. To stress-test our assumptions against future uncertainty, we often run a Monte Carlo simulation to get a more robust picture of potential outcomes.

Insight Edge: A Value-Add Multifamily DCF ExampleLet's say we're buying a 100-unit building where rents are 20% below market. Our plan is to inject $10,000 per unit for renovations over the first two years. A simple cap rate on today's income would undervalue this opportunity.* Years 1-2: Our model shows lower Net Operating Income (NOI) due to renovation downtime and heavy capital spending.* Years 3-5: As renovated units come online, we project leasing them at higher market rates, causing the NOI to increase significantly.* Year 5 (The Exit): We model the sale of the now-stabilized asset. With a much higher income stream, we can sell it at a "terminal" cap rate that reflects its improved condition and performance.By discounting all these projected cash flows—and the final sale proceeds—back to their present value, our DCF model gives us a valuation that truly captures the future value we're creating. It’s a far more dynamic and insightful tool than just slapping a cap rate on day-one income.

Applying The Cost and Residual Valuation Methods

So, what do you do when you can't find any recent sales comps and there’s no predictable income stream to analyze? This is a common problem with unique properties, new construction, or proposed developments. Both the Sales Comparison and Income Approaches can fall flat.

This is exactly where the Cost Approach comes in. It provides a logical, ground-up framework for valuation.

The logic is simple: a property shouldn’t be worth more than it would cost to build a functional equivalent from scratch. This makes it an indispensable tool for real estate development and for valuing specialized assets where comps just don't exist—think a brand-new medical office building, a data center, or a public school.

The formula itself is pretty straightforward:

Value = Replacement Cost New - Accumulated Depreciation + Land Value

This equation breaks the valuation down into its core parts, forcing a methodical, piece-by-piece analysis.

Deconstructing The Cost Approach Formula

First, an appraiser has to calculate the Replacement Cost New. This is the estimated cost to construct a building with the same utility, but using today’s materials and modern standards. It covers everything: labor, materials, contractor overhead, and even developer profit.

Then comes the tricky part: figuring out Accumulated Depreciation. In an appraisal, depreciation isn't just about routine wear and tear. It’s any factor that drags down the property's value compared to a brand-new version. For a deeper look at how this concept also unlocks major tax advantages, our guide on the tax shield on depreciation is a must-read for serious investors.

Appraisers have to quantify three main types of depreciation:

Physical Deterioration: This is the one everyone thinks of—the physical decay of the property. We’re talking about a leaky roof, cracked pavement, or an HVAC system on its last legs. It can be curable (it makes economic sense to fix it) or incurable (the repair cost is more than the value it adds).

Functional Obsolescence: This happens when a property's design is just plain outdated. Think of a five-bedroom house with only one bathroom or a warehouse with ceilings too low for modern forklifts and racking systems. The property just doesn’t function well for its intended use anymore.

External Obsolescence: This form of depreciation is caused by negative factors completely outside the property lines. It could be a new zoning law that restricts the property’s use, a sudden increase in traffic congestion, or a major local employer shutting down. This type is almost always incurable.

By adding up all these forms of depreciation and subtracting them from the replacement cost, the appraiser arrives at the value of the improvements, which is then added to the land value.

The Developer's Go-To: The Residual Land Valuation Method

For sophisticated investors and developers underwriting a new deal, there’s a specialized version of the Cost Approach that is absolutely essential: the Residual Land Valuation method.

This technique flips the standard formula on its head to solve for the single most important variable in a new development—what you can actually afford to pay for the land.

Instead of starting with land value, you work backward to find it. It's really a feasibility analysis that answers the critical question: "Given this project's total value and costs, what's the maximum price we can pay for this site and still hit our return targets?"

Here’s how the process works backward:

Estimate Gross Development Value (GDV): First, we figure out the total value of the project once it’s built and stabilized. This is usually done with the Income Approach, like capitalizing the projected Net Operating Income.

Subtract All Development Costs: Next, we subtract every single cost tied to the project. This includes hard costs (materials, labor), soft costs (architectural fees, permits, insurance), financing costs, and a necessary line item for developer profit.

The Remainder is the Land Value: What’s left over—the residual amount—is the highest price you can justify paying for the land.

Investor TakeawayAt Stiltsville Capital, we live by the Residual Land Valuation method. It's a core discipline when we evaluate ground-up development opportunities, including our modular multifamily projects. If our analysis shows the required land price is higher than what the seller is asking, the deal simply doesn't pencil out. This rigorous, data-driven approach ensures we never overpay for land, protecting investor capital from day one.

How to Choose the Right Appraisal Method for Your Strategy

Understanding the individual appraisal methods real estate professionals use is one thing. Knowing which one to lean on for a specific deal is what separates novice investors from seasoned experts.

The right method isn’t just a matter of preference; it’s dictated by the asset itself and your strategic goals. A stabilized, fully-leased office building and a ground-up development opportunity are two entirely different animals, and they demand different valuation lenses. The key is matching the method to the asset’s characteristics and where it sits in the investment lifecycle.

The Art of Reconciliation

An appraiser rarely, if ever, hangs their hat on a single method. Instead, they perform a reconciliation—a process of weighing the values derived from two or three different approaches to arrive at a final, defensible opinion of value.

Think of it as building a legal case. The Sales Comparison Approach is your eyewitness testimony, the Income Approach is your financial forensics, and the Cost Approach is your expert reconstruction. An appraiser gives the most weight to the method providing the most reliable and relevant evidence for that specific property.

For a 10-year-old apartment building with plenty of recent sales in the area, the Sales and Income approaches will carry the most weight. For a custom-built data center, the Cost and Income approaches will dominate, simply because finding true "comps" is next to impossible.

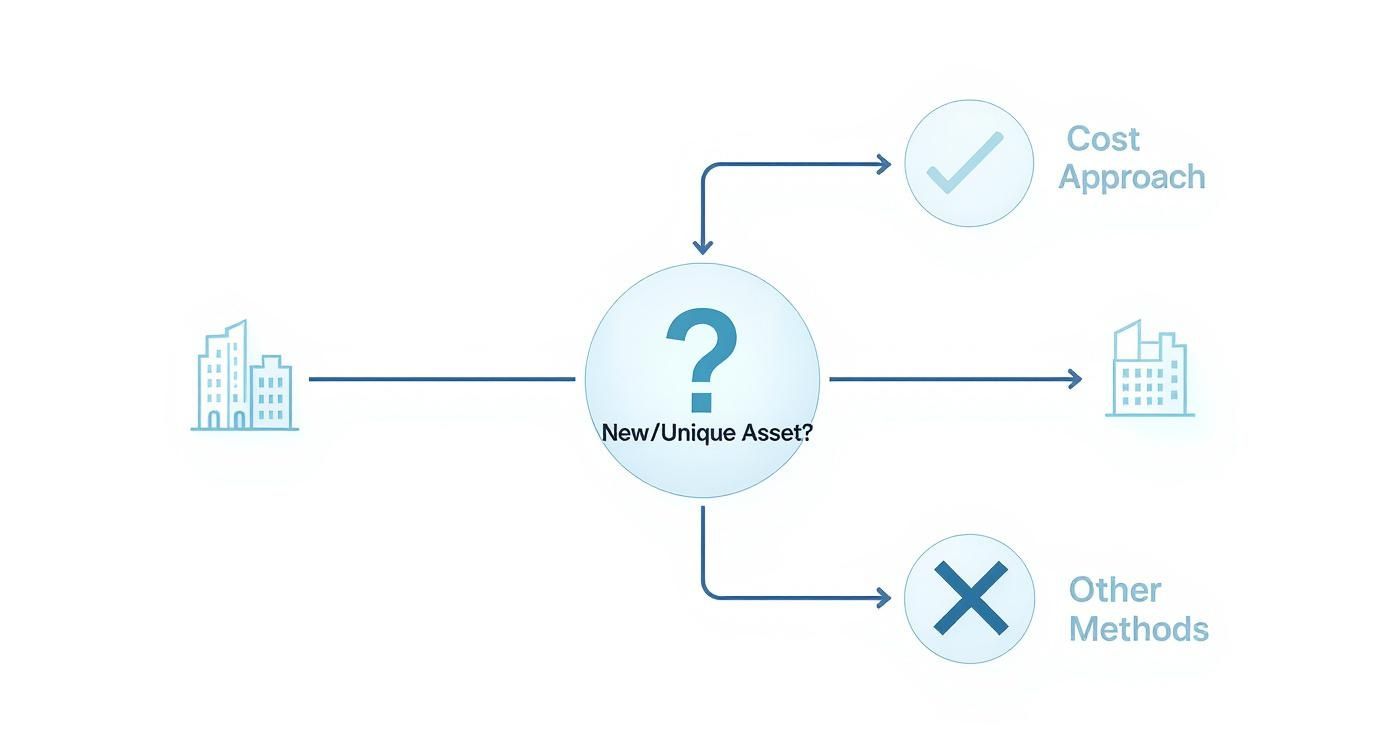

This decision tree shows exactly when the Cost Approach becomes the most logical choice, particularly for new or unique assets where other methods fall short.

The real takeaway here is that the Cost Approach steps up as the primary tool when an asset's uniqueness or newness makes historical sales or income data irrelevant.

Mapping Appraisal Methods to Property Type and Strategy

Knowing which appraisal method to prioritize is fundamental to your investment strategy. A mismatch can throw off your entire underwriting process and lead you to make the wrong call on a deal. This table breaks down which methods we emphasize for different asset types and strategies.

Property Type / Strategy | Primary Method | Secondary Method | Investor Takeaway |

|---|---|---|---|

Core (Stabilized Multifamily) | Income (Direct Cap) | Sales Comparison | Value is driven by stable, predictable NOI. Comps simply confirm the market cap rate is in line. |

Value-Add (Retail Repositioning) | Income (DCF) | Cost Approach | The DCF is king because it captures the future value created from renovations and lease-up. The Cost Approach helps validate your renovation budget. |

Opportunistic (Ground-Up Dev.) | Cost / Residual Land | Income (DCF) | The Residual Method determines if the land deal even makes sense. Then, the DCF projects the value of the final, stabilized asset once built. |

Unique Asset (Medical Office) | Income (DCF) | Cost Approach | Long-term leases with credit tenants make the DCF the most reliable method. The Cost Approach is a crucial check for any new construction or expansion plans. |

As you can see, the choice isn't random. It’s a strategic decision that aligns the valuation technique with the specific way you plan to create value.

Questions to Ask a Sponsor About Valuation

When you review a deal from a sponsor, the final valuation number is far less important than the assumptions that got them there. To truly get under the hood of their underwriting, you need to ask the right questions.

Sales Comps: Which comparable properties did you choose, and why? What specific adjustments were made for location, age, and amenities, and what was the logic behind them?

Income Approach: Where are you sourcing your market rent and expense assumptions? How does your exit cap rate compare to the entry cap rate and current market rates? For a deep dive, check out our guide to the capitalization rate real estate formula.

DCF Projections: What are your annual rent growth and inflation assumptions over the hold period? How did you model for vacancy and credit loss, and are those numbers stressed?

Cost Assumptions: Are your construction or renovation budgets based on recent, hard bids or general estimates? What contingency has been included for overruns?

Investor TakeawayA sponsor's valuation tells a story about their business plan. By dissecting their assumptions, you can gauge the realism of their projections and the discipline behind their underwriting. A confident sponsor will always have clear, data-backed answers to these questions.

Answering Your Top Real Estate Appraisal Questions

Even the most experienced investors run into questions when it comes to the finer points of property valuation. Here are some of the most common ones we hear, broken down with straight answers to help sharpen your due diligence.

How Do Automated Valuation Models Compare to Traditional Appraisals?

Think of Automated Valuation Models (AVMs) as a quick first glance. They're algorithms that spit out a property estimate in seconds, which is great for high-level portfolio screening. But they’re just that—a glance. AVMs can’t see the new roof you just put on, the water damage in the basement, or the unique neighborhood dynamics an appraiser picks up on just by walking the property. For a decision as big as an institutional investment, an AVM is only the starting point. The real commitment always comes after a full appraisal using one of the core methods we've discussed.

What Is the Difference Between As-Is and As-Stabilized Valuation?

This is a critical distinction, especially for the kind of value-add and development projects we tackle. An "as-is" valuation tells you what a property is worth right now, in its current state. On the other hand, an "as-stabilized" valuation is a projection. It estimates the property's value after our business plan is fully executed—meaning all renovations are done, the building is leased up, and it's generating the income we projected. This future value is absolutely essential for lining up financing and proving out the deal's potential returns.

Why Might Two Appraisals for the Same Property Show Different Values?

This happens more than you’d think, and it’s because valuation is part science, part art. Two perfectly qualified appraisers can look at the same asset and land on different numbers. Here’s why:

Different Comps: One appraiser might pull a slightly different set of comparable sales or apply different adjustments.

Varying Assumptions: In an income approach, a tiny tweak to the cap rate or discount rate can create a big swing in the final valuation.

Subjective Adjustments: How much is a "better location" or "superior condition" really worth? That number involves a degree of professional judgment, and it can vary.This is exactly why smart investors never just look at the final number. You have to dig into the appraiser’s report and understand the why behind their value. That’s where the real insight is.

Is a Broker Opinion of Value the Same as an Appraisal?

Not at all. A formal appraisal is a legally binding, impartial valuation from a state-licensed professional who must follow strict industry standards. A Broker’s Opinion of Value (BOV) is an informal estimate from a real estate broker of what a property might sell for. It’s a useful data point, but lenders won’t touch it for financing.

Mastering these appraisal concepts is fundamental to disciplined and profitable real estate investing. We believe that well-structured real assets, underwritten with this level of rigor, can be a prudent and resilient component of a long-term wealth strategy. At Stiltsville Capital, this analytical depth isn't just a step in our process—it's the foundation of everything we do to protect investor capital and create value.

To learn more about our institutional-grade investment opportunities, schedule a confidential call with our team.

Information presented is for educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy securities. Any offering is made only through definitive offering documents (e.g., private placement memorandum, subscription agreement) and is available solely to investors who meet applicable suitability standards, including “Accredited Investor” status under Rule 501 of Regulation D. Investments in private real estate involve risk, including loss of capital, illiquidity, and no guarantee of distributions. Past performance is not indicative of future results.

Comments