How to Invest in Apartments: A Guide for Accredited Investors

- Ryan McDowell

- Aug 9, 2025

- 15 min read

Reading Time 8 min | Good for: Novice Investors, Family Offices, UHNWI

TL;DR: Key Takeaways

Three Paths to Invest: You can invest in apartments through Direct Ownership (high control, high effort), publicly-traded Real Estate Investment Trusts (REITs) (liquid, no control), or Private Placements (Syndications), which offer a balance of passive involvement with access to institutional-grade deals.

Why Apartments Now: A persistent structural housing shortage combined with a cultural shift towards renting creates strong, predictable demand. According to research from Hines, developed economies face a 6.5 million unit housing deficit, pushing more households into the rental market.

Sponsor Quality is Paramount: In passive investing, your most critical decision is choosing the right sponsor. Their experience, transparency, and alignment of interest (i.e., co-investing their own capital) are the best mitigants against execution risk.

The Goal is Passive Income & Equity Growth: The core strategy involves acquiring properties, increasing their Net Operating Income (NOI) through smart management and value-add improvements, and then realizing that value through a strategic sale or refinance.

Next Step: For accredited investors considering a passive allocation, the next step is to understand the due diligence process and speak with experienced sponsors.

So, you're looking to get into apartment investing. Smart move. But where do you even start? It really boils down to three main ways to play the game: buying properties yourself, joining a group deal (what we call a syndication), or simply buying shares in a Real Estate Investment Trust (REIT). Each route offers a completely different mix of control, capital required, and personal time commitment.

This guide is your roadmap. Whether you're dipping your toes into real estate for the first time or you're a family office principal seeking institutional-quality deals, we'll break it down. Our goal is to pull back the curtain on the entire process—from finding the deal to cashing the final check—so you can make your next move with total confidence.

The Three Core Investment Pathways

Investing in apartments isn't a one-size-fits-all deal. The best path for you will hinge on your capital, your tolerance for risk, and frankly, how much you want to be bothered with the day-to-day grind.

Let's look at the main options:

Direct Ownership: This is the roll-up-your-sleeves approach. You buy a property, either solo or with a few partners, and you’re on the hook for everything. Financing, leaky faucets, finding tenants, and eventually selling—it’s all on you. You get maximum control, but it demands a serious commitment of time, expertise, and capital.

Passive Syndication (Private Placement): Here, you pool your capital with other investors and a seasoned operator (the "Sponsor") to acquire a much larger property than you could alone. As a passive investor, or Limited Partner (LP), your role is to provide capital. The Sponsor handles the heavy lifting. This is a primary path for accredited investors who want a piece of professionally managed, large-scale deals without becoming a landlord.

Real Estate Investment Trusts (REITs): Think of REITs as mutual funds for real estate. These are massive companies that own, and often operate, huge portfolios of properties, including apartments. Buying a share of a publicly-traded REIT is as easy as buying a stock, offering excellent liquidity. The trade-off? You have virtually no control or direct connection to the underlying assets.

To give you a clearer picture, here's a high-level look at how these investment pathways stack up against each other.

Apartment Investment Pathways At a Glance

Investment Pathway | Level of Control | Typical Capital Outlay | Investor Role | Best For |

|---|---|---|---|---|

Direct Ownership | High | High | Active (Landlord/Manager) | Experienced investors who want full control and have significant capital. |

Syndication | Low | Moderate | Passive (Capital Provider) | Accredited investors seeking access to larger deals without management duties. |

REIT | None | Low | Passive (Shareholder) | Beginners or those prioritizing liquidity and diversification over control. |

Each path has its place. The key is aligning the strategy with your personal financial goals, available time, and how hands-on you truly want to be.

Why Apartments Are Such a Compelling Asset Class

The appeal of apartment investing isn't just hype; it's backed by powerful economic and demographic forces. The biggest factor? A massive, ongoing housing shortage running headlong into a cultural shift toward renting.

It’s a simple supply-and-demand story. Research from Hines.com shows that developed economies are short an estimated 6.5 million housing units (as of their 2023 report). This structural gap creates a serious affordability problem, pushing a huge portion of households—over 80% in many major economies—into the rental market.

This dynamic creates a steady, predictable stream of demand for apartments. For investors, that translates into a resilient, income-producing asset class that’s hard to beat, especially when positioned as an inflation hedge within a diversified portfolio.

Sourcing and Underwriting Winning Apartment Deals

Finding a genuinely great apartment deal isn't about getting lucky. It’s a disciplined process that sharply separates seasoned investors from the rest of the crowd. While anyone can find a property on a public listing, the real gems—the most compelling opportunities—are often found off-market. These deals come from deep, trusted relationships with brokers and our own proprietary data analysis.

We spend years cultivating these networks. The goal is to become the first call for a broker who has a quiet listing. Why? Because they know we can perform—that we have the capital and expertise to close deals quickly and reliably. This kind of access is a massive advantage for our investors, allowing us to bypass the intense bidding wars of the open market.

The Numbers That Truly Matter

Once a potential deal lands on our desk, the real work begins. We call this underwriting. It’s the rigorous financial deep-dive we use to project a property's future performance and decide if it meets our strict investment criteria. This is so much more than plugging numbers into a spreadsheet; it's about building a credible, data-backed story of future value.

The entire foundation of a solid underwriting model is the Net Operating Income (NOI). You can think of it as the property's total income (from rent, fees, etc.) minus all its day-to-day operating expenses, but before factoring in debt service (mortgage payments) or taxes. A healthy, growing NOI is the engine that powers both cash flow to investors and the property's overall value.

Novice Lens: Why NOI Matters Think of NOI as the property's annual profit from its core business: renting apartments. A higher NOI means a more profitable building, which is exactly what we're all looking for. It's the purest measure of the asset's performance.

From that foundational NOI, we stress-test the deal with a few critical metrics:

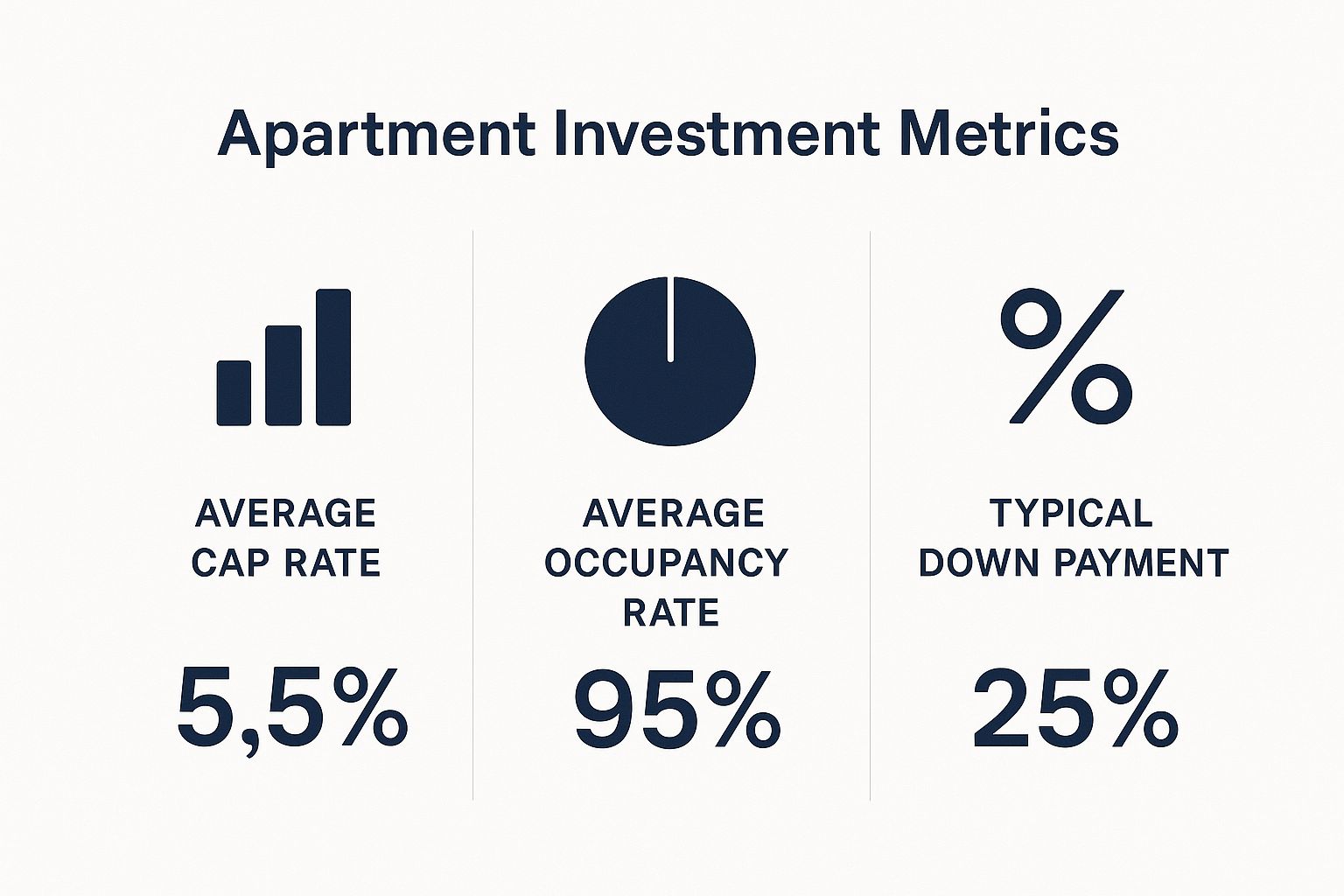

Capitalization Rate (Cap Rate): This is the NOI divided by the purchase price. It shows the unlevered annual return you'd get if you bought the property with all cash. A lower cap rate usually signals a less risky, more desirable property in a prime location.

Internal Rate of Return (IRR): This is the big one. IRR is a more sophisticated metric that calculates the total annualized return over the entire life of the investment. It accounts for your initial investment, all cash distributions received, and the final profit from the sale. It’s a powerful tool because it factors in the time value of money, letting us accurately compare different opportunities.

Market Signal Box (Q2 2024)

The Data: Global investment in the living sector is on the rise, with rental growth rates hitting approximately 4.6% in early 2024, according to JLL.

Our Interpretation: Despite higher interest rates, the fundamental supply/demand imbalance for rental housing remains firmly in place. Persistent housing shortages and the expectation of lower borrowing costs on the horizon should continue to attract capital to quality multifamily assets.

Investor Take: Focus on sponsors who can execute in any rate environment and create value at the property level, not just rely on market appreciation. For a deeper dive, you can explore the JLL global market outlook.

Deal Lens Example: A Value-Add Acquisition in Action

Numbers on a page are one thing; seeing them work in the real world is another. Let’s walk through a simplified, illustrative case study of how smart underwriting uncovers hidden potential.

Imagine we find a 100-unit apartment building for sale for $10 million. It's an older property, and it's been poorly managed for years. As a result, rents are about 20% below market, and operating expenses are bloated.

The Starting Point: The current NOI is just $450,000. At a $10 million purchase price, that gives us a 4.5% entry cap rate. Not bad, but not great. Our analysis shows that by investing $1 million ($10,000/unit) in smart renovations (new kitchens, updated bathrooms, modern common areas), we can justify raising rents to market levels over the next 24 months.

The Game Plan: On top of the renovations, we’ve identified $50,000 in annual savings by bringing in professional management and implementing energy-efficient upgrades.

The Payoff (Year 3): After executing our value-add plan, the stabilized NOI is projected to jump to $650,000. In this submarket, a renovated, well-managed property like this now trades at a 5.0% exit cap rate.

The Exit: Based on our new, higher NOI and the market cap rate, the property's value has increased to $13 million ($650,000 NOI / 0.05 cap rate). After subtracting our total cost of $11 million (purchase plus renovation), we've created $2 million in equity for our investors.

This is the essence of a value-add strategy. It's about seeing the potential that others miss and having the operational expertise to bring that value to life.

Structuring Your Investment and Securing Financing

How an apartment investment is structured is every bit as important as the property itself. This is where returns are amplified and, crucially, where your capital is protected. For a passive investor, understanding the deal structure isn’t just a good idea; it’s non-negotiable. It dictates exactly how and when you get paid.

The architecture of any large apartment deal is the capital stack. Picture a layered cake of funding. Each layer represents a different type of capital with its own risk profile and potential reward. The bottom is the safest layer, and as you move up the stack, both the risk and potential returns climb.

Understanding the Capital Stack

A well-balanced capital stack is the signature of a disciplined sponsor. It's composed of two key ingredients: debt and equity.

Senior Debt: This is the primary mortgage on the property, usually from a bank or an agency lender like Fannie Mae or Freddie Mac. As the most secure piece of the stack, lenders in this position are paid back first. Their risk is lowest, and so is their return (the loan's interest rate).

Mezzanine Debt or Preferred Equity: Sometimes, there’s a gap between the senior loan and the common equity. Mezzanine financing or preferred equity can fill this, acting as a hybrid of debt and equity. It’s riskier than the senior loan but safer than common equity, typically offering a fixed return and getting paid out before common equity investors see a dime.

Common Equity: This is your slice of the pie. It’s the capital contributed by the sponsor (GP) and passive investors (LPs) like you. It's the highest-risk, highest-reward layer. Equity investors are paid last, after all lenders are made whole, but you also share in the property's upside and profits at sale. For a deeper look, check out our comprehensive guide to commercial real estate financing options.

If you’re just starting, remember that your spot in the stack determines your spot in the payout line. As a common equity investor, you’re betting on the sponsor's ability to execute the business plan and generate profits that exceed all debt obligations.

The Private Placement and Your Protections

For most accredited investors in syndications, the investment vehicle is a private placement, typically structured under Regulation D of the Securities Act. A common structure is the 506(c) offering, which lets sponsors advertise the deal publicly—as long as they take reasonable steps to verify that every investor is accredited.

The most important document you'll receive is the Private Placement Memorandum (PPM). It’s dense, but it's your best friend. This document lays out every detail: the property, the business plan, all potential risks, the sponsor's fee structure, and the distribution waterfall.

Advanced Lens: The Distribution Waterfall The real meat of the PPM is the distribution waterfall, which dictates the order and proportion of profit splits between Limited Partners (LPs) and the General Partner (GP/Sponsor). A common structure is: 1. Return of Capital: All LPs get 100% of their initial investment back. 2. Preferred Return ("Pref"): LPs receive a preferred return (e.g., an 8% cumulative annual return) on their outstanding capital. This is a hurdle the sponsor must clear before sharing in profits. 3. The Split ("Promote"): After the pref is paid, remaining cash flow is split. A 70/30 or 80/20 split (LP/GP) is standard. This "promote" or "carried interest" is the sponsor's main incentive to outperform.

Look for the sponsor's "skin in the game"—how much of their own money they've put into the deal. A significant co-investment, typically 5-10% of the total equity, is a powerful sign that their interests are truly aligned with yours. They only make money if you do.

Mastering Due Diligence as Your Investor Shield

So, you’ve found a deal where the numbers on the pro forma look great and the financing structure seems solid. Now what?

This is where the real work begins. Proper due diligence is the single most important defense you have against a bad investment. It's the disciplined, methodical process of verifying every assumption before you commit a single dollar of capital.

For passive investors, this deep dive accomplishes two things. First, it validates the property and the sponsor’s financial projections. But just as importantly, it gives you a crystal-clear window into the sponsor’s competence, transparency, and integrity. How a sponsor handles the due diligence process tells you everything about how they'll handle your investment when things get tough.

Your Investor Checklist: Questions to Ask a Sponsor

Your job as a passive investor isn't to personally conduct these audits. It’s to confirm that the sponsor has an institutional-quality process and is transparent in sharing the findings—the good, the bad, and the ugly. A sophisticated sponsor will have these answers and supporting documents ready.

Financial Diligence

Are the pro forma assumptions (rent growth, vacancy) backed by historical performance and third-party market data?

What are the three largest expense line items, and how do they compare against industry benchmarks?

Key Documents: Trailing 12-Month (T-12) Operating Statement; Rent Roll; Third-Party Market Reports (e.g., from CoStar, CBRE).

Physical Diligence

What is the age and condition of the roof, HVAC systems, and plumbing?

Has a Property Condition Assessment (PCA) been conducted by a qualified engineer?

Is there a Phase I Environmental Site Assessment (ESA) to check for contamination?

Key Documents: PCA Report; Phase I ESA Report.

Legal Diligence

Is there a clean title report with no unexpected liens or easements?

Does the property's current use comply with all local zoning ordinances?

Have all tenant leases been reviewed for unusual clauses or concessions?

Key Documents: Title Report; ALTA Survey; Zoning Report.

Sponsor Diligence

Can you provide references from investors in a past deal, especially one that faced challenges?

What is your communication and reporting cadence during the hold period?

What is your firm's full track record—including case studies on home runs and deals that didn't go as planned?

Key Documents: Private Placement Memorandum (PPM); Investor References; Past Deal Track Record.

This framework isn't just about checking boxes. It’s about stress-testing the sponsor’s entire business plan. The answers build confidence not just in the asset, but more importantly, in the team you’re trusting with your capital.

For a more exhaustive breakdown, see our [guide to commercial real estate due diligence](https://www.stiltsvillecapital.com/post/a-guide-to-commercial-real-estate-due-diligence-the-investor-s-playbook).

Driving Value from Acquisition to Exit

Getting a deal over the finish line is just the beginning. The real work—and where the real money is made—starts the day you close. This is the asset management phase, where a sponsor’s skill turns a well-researched business plan into real returns for investors.

Whether the game plan involves ground-up construction, a moderate value-add renovation, or simply running a mismanaged property correctly, this is the most active stage of the investment. It’s all about constant execution, monitoring, and tweaking to boost cash flow and drive up the property's final sale price.

Executing The Business Plan

A professional sponsor hits the ground running with a clear playbook. For a value-add deal, this means systematically renovating units, upgrading common areas, and boosting curb appeal to justify higher rents. This isn’t just spending money; it's a calculated deployment of capital designed for maximum return on investment (ROI).

This hands-on management is what drives the property's Net Operating Income (NOI). Every dollar saved on expenses or gained in rent drops straight to the bottom line, which means better cash distributions for you and a higher valuation for the building.

Monitoring Performance and Reporting to Investors

One of the biggest tells of a quality sponsor is their commitment to transparent and regular communication. You should expect detailed quarterly reports that give you a genuine health check on your investment.

Good reports track the Key Performance Indicators (KPIs) that actually matter:

Physical vs. Economic Occupancy: The percentage of units with tenants vs. the rent actually collected compared to the total possible rent.

Leasing Velocity: For a new or repositioned property, how many new leases are signed each month compared to projections.

Budget vs. Actuals: A clear, line-by-line comparison of real income and expenses against the initial underwriting, with solid explanations for any significant variances.

This kind of transparency is non-negotiable. It builds trust and shows your capital is being managed with discipline.

Investor's Takeaway: Think of the exit as part of the initial plan, not an afterthought. A savvy sponsor underwrites the deal with a clear exit strategy in mind from day one, which informs every decision made during the holding period.

Planning the Exit Strategy

From the moment you buy, the clock is ticking toward the eventual sale. The entire point of a private real estate deal is to realize the value created and return capital—plus a profit—to investors.

Stabilized Sale: The classic exit. Once the business plan is complete and the property has a solid track record of higher, stable income, it’s sold on the open market. The buyers are often more conservative, long-term players (like insurance companies or REITs) who will pay a premium for a de-risked, cash-flowing asset. The new, higher NOI combined with a market cap rate sets the sale price. You can dive deeper into this in our [clear guide to the capitalization rate formula](https://www.stiltsvillecapital.com/post/capitalization-rate-formula-real-estate-a-clear-guide-for-investors).

Portfolio Disposition: If the property is part of a larger group of similar assets, a sponsor might package them for sale. This can attract large institutional buyers and often command a premium.

Strategic Refinance: Sometimes, selling isn't the best move. Instead, a sponsor might refinance the property. After increasing the NOI, they can secure a new, larger loan. This pays off the original debt and can return a significant portion (or even all) of the initial investor equity, while you continue to own a cash-flowing asset.

Your Top Apartment Investing Questions, Answered

Let's address the most common questions we hear from investors, whether they are new to the space or seasoned family office principals.

What is the typical minimum investment for a private deal?

For investors partnering in larger deals through a private placement or syndication, the entry point is more manageable than direct ownership but still represents a significant commitment. Most high-quality sponsors set their minimums between $50,000 and $100,000 for a single deal. This ensures a focused group of committed partners and gives each investor a meaningful stake in a top-tier asset.

How liquid is my capital in a private real estate investment?

This is a critical point to grasp. Unlike a public REIT traded like a stock, private real estate investments are fundamentally illiquid.

When you commit capital to a syndication, you are generally committed for the entire business plan, which typically runs three to seven years. There is no public market to sell your share. While a sponsor may try to facilitate a sale to another investor in a true emergency, this is not guaranteed and may come at a discount.

Risk & Mitigation * Risk: Illiquidity. Your capital is tied up for the life of the project. * Mitigation: The potential for higher, non-correlated returns is your compensation for this illiquidity. Never invest capital you may need for short-term needs.

What are the biggest risks to watch out for?

Beyond broad market risks like recessions or interest rate spikes, the two biggest manageable risks are sponsor risk and execution risk.

Sponsor Risk: This is the risk of partnering with the wrong team. An inexperienced, untrustworthy, or misaligned sponsor is the fastest way to lose money. Your due diligence on the sponsor is even more important than your diligence on the property itself.

Execution Risk: This is the risk that the sponsor cannot deliver on the business plan. Perhaps renovation costs overrun, projected rent growth isn't achieved, or leasing lags. A great sponsor mitigates this with conservative underwriting, deep operational experience, and a significant co-investment that proves their interests are 100% aligned with yours.

How do I know if a sponsor’s fees are fair?

Fees are how a sponsor gets paid for sourcing, managing, and creating value. They are a standard part of syndications, but the structure is what matters. You want a "pay for performance" structure.

Common fees outlined in the PPM include:

Acquisition Fee: A one-time fee for sourcing and closing the deal, typically 1-2% of the purchase price.

Asset Management Fee: An ongoing annual fee for overseeing the property and executing the business plan, often 1-2% of gross revenue.

Promote (or Carried Interest): The sponsor's share of profits, but only after investors receive their initial capital back plus a preferred return. A common, fair structure is an 80/20 split (80% of profits to investors, 20% to the sponsor) after an 8% preferred return hurdle is met.

Be cautious of sponsors with heavy upfront fees. The best align their compensation with your success, meaning their biggest payday comes from the back-end promote—after they’ve delivered fantastic results for you.

Well-structured real estate can be a prudent, resilient component of a long-term wealth strategy. At Stiltsville Capital, we provide accredited investors with direct access to institutional-grade apartment investment opportunities. If you are ready to explore how a professionally managed real estate allocation can fit into your portfolio, we invite you to schedule a confidential call.

Information presented is for educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy securities. Any offering is made only through definitive offering documents (e.g., private placement memorandum, subscription agreement) and is available solely to investors who meet applicable suitability standards, including “Accredited Investor” status under Rule 501 of Regulation D. Investments in private real estate involve risk, including loss of capital, illiquidity, and no guarantee of distributions. Past performance is not indicative of future results. Verification of accredited status is required for participation in Rule 506(c) offerings.

Comments