Limited Partnership in Real Estate: Your Guide to Institutional-Grade Deals

- Ryan McDowell

- Aug 15, 2025

- 17 min read

Reading Time 6 min | Good for: Novice Investors (A), Informed Principals (B)

Ever wondered how massive, institutional-grade real estate deals get done? It's rare for one person or company to have both the deep pockets and the specialized expertise needed to pull off a major property acquisition. That’s where a brilliant structure called a limited partnership (LP) comes into play.

A limited partnership in real estate is a formal team-up between two types of partners: a General Partner (GP) who actively manages the project, and one or more Limited Partners (LPs) who provide the capital. Think of it as a way for investors to access large-scale deals with built-in liability protection, much like owning stock in a company, but with the tangible benefits of real estate.

TL;DR: The Investor's Take

What it is: A legal structure where passive investors (LPs) provide capital to an active expert (the GP) to buy and manage real estate.

Why it matters: LPs gain access to large-scale deals, professional management, and liability limited to their investment amount.

Key takeaway: Your success hinges on the GP's expertise and integrity, making sponsor due diligence the most critical step.

Market Why-Now: The Case for Private Real Estate

Despite market volatility, the appetite for private real estate among sophisticated investors remains strong. According to a 2023 survey by Preqin, a leading alternatives data provider, a significant number of institutional investors and family offices plan to maintain or increase their allocations to real estate over the long term. They are drawn to its potential for income generation, inflation hedging, and portfolio diversification away from public markets. Limited partnerships are a primary vehicle for deploying this capital effectively.

Decoding the Real Estate Limited Partnership

At its heart, the LP structure elegantly solves the classic real estate dilemma: you need significant capital and deep operational know-how, and they don't often live under the same roof. The LP bridges this gap, creating a formal alliance between money and expertise.

This model became a go-to vehicle for pooling capital in the mid-20th century. After some legislative shifts over the years, LPs re-emerged as a dominant force in real estate syndications. To give you an idea of their scale, data reported to the SEC in 2020 showed that limited partnerships accounted for roughly 30% of all pooled vehicle investments in U.S. commercial real estate.

The Two Sides of the Partnership Coin

To really get it, you have to understand the two distinct roles. Imagine a world-class chef wants to open a new restaurant. She has the culinary vision and the skill to run the kitchen, but she needs funding to build it out.

The General Partner (GP): This is your "chef"—the sponsor or operator of the deal. The GP is the hands-on manager who handles the entire lifecycle of the investment. They find the property, perform due diligence, line up the financing, oversee daily operations, and execute the final sale. Because they’re in the driver's seat, the GP traditionally carries unlimited liability, meaning their personal assets could be on the line if things go south (though this is often shielded by structuring the GP as an LLC).

The Limited Partner(s) (LP): These are the passive investors who provide the lion's share of the equity. The LPs are the "diners" who fund the restaurant but don't step foot in the kitchen. Their job is to contribute capital. In return, they get a share of the profits and get to ride on the GP's expertise without getting bogged down in management. And here’s the key: their liability is limited to their investment amount.

**Novice Lens: Why This Matters**For an investor, that distinction is everything. As an LP, your financial exposure is capped. Your personal assets are safe from any project-related lawsuits or debts. This protection is the cornerstone of what makes the limited partnership such a powerful and popular way to invest passively in real estate.

The Foundation of the Agreement

The entire relationship is built on a rock-solid legal document: the Limited Partnership Agreement (LPA). This is the constitution for the investment. It meticulously spells out the rights, responsibilities, and financial breakdown for both the GP and the LPs.

The LPA covers everything from when capital is due and how profits are split (the "distribution waterfall") to voting rights and the GP's fees. For any Limited Partner, this is the single most important document to scrutinize during due diligence. It lays out the exact terms of your investment and is the first step toward getting access to institutional-quality deals.

Want to learn more? Check out our guide to limited partnership real estate and see how it all works.

The General Partner vs. The Limited Partner

In any real estate limited partnership, you'll find two distinct and essential roles: the General Partner (GP) and the Limited Partner (LP). Think of it as a deliberate separation of duties that makes the entire investment tick. The GP is the active manager, the one with boots on the ground, while the LPs are the strategic capital providers.

To really get a handle on how these ventures work, you have to understand the clear line drawn between these two players. Each one is critical to success, but they operate on completely different levels of involvement and responsibility.

The General Partner—often called the sponsor or operator—is the quarterback of the deal. They're the ones bringing the specialized expertise to the table that passive investors simply don't have the time or background to develop. Their work is intense and covers the entire life of the investment, from finding the deal to selling it.

On the other side of the coin, the Limited Partners are the financial muscle. Their main job is to provide the equity needed to buy and improve the property, which allows the GP to get to work and execute the business plan. While it's not a completely hands-off role (diligence is key!), it’s defined by passive participation rather than active management.

For high-net-worth individuals and family offices, this structure is a fantastic way to get exposure to high-quality commercial assets without the headache of day-to-day operations. A deeper look into how to invest in commercial property can shed more light on this effective, passive approach.

The General Partner in The Driver's Seat

The GP is the engine of the entire operation. Their responsibilities are vast and demand deep market knowledge, sharp financial skills, and a ton of operational experience.

Here’s a snapshot of what a GP does:

Sourcing the Deal: They’re out there hunting for undervalued or opportunistic properties that fit a specific investment strategy.

Conducting Due Diligence: This involves exhaustive research into the property’s physical shape, financial health, legal standing, and market position.

Arranging Financing: The GP secures the loans and structures the entire capital stack for the deal.

Executing the Business Plan: This is the day-to-day grind—managing operations, overseeing renovations, negotiating leases, and making sure the property performs at its best.

Investor Reporting: They keep the LPs in the loop with regular, transparent updates on financial performance and project progress.

Managing the Exit: When the time is right, the GP strategically markets and sells the property to maximize returns for everyone involved.

For all this hard work, the GP is compensated through fees and a slice of the profits, often called the "promote" or "carried interest." This structure is designed to align their financial success directly with the success of the limited partners.

The Limited Partner As The Capital Provider

The Limited Partner's role is fundamentally different. As an LP, your primary function is to contribute capital. In exchange, you get ownership equity in the partnership and all the economic benefits that come with it.

Your involvement is passive, but your rights are clearly defined and protected by the Limited Partnership Agreement (LPA).

Key LP Protections: Your liability is strictly limited to the amount of money you invest. This is a crucial legal shield that protects your personal assets from any debts or legal troubles related to the property. You also have legal rights to receive accurate financial reports and to vote on major decisions, like selling the asset, as spelled out in the LPA.

Your time is best spent on the front end, doing your homework—vetting the GP, their track record, and the specific deal itself. Once you’re in, your role shifts to monitoring the investment's performance through the reports the GP provides. It’s the perfect setup for investors who want to add real estate to their portfolio without taking on a second job as a property manager.

General Partner (GP) vs. Limited Partner (LP) At a Glance

To make the distinction crystal clear, here’s a side-by-side comparison of the two roles. This table breaks down exactly what separates the active manager from the passive investor.

Attribute | General Partner (GP) | Limited Partner (LP) |

|---|---|---|

Primary Role | Active Manager & Operator | Passive Capital Provider |

Liability | Unlimited (often shielded by an LLC structure) | Limited to the amount of invested capital |

Decision-Making | Controls all day-to-day operational decisions | No operational control; may have voting rights on major decisions |

Time Commitment | Full-time, intensive involvement | Primarily upfront due diligence; minimal ongoing time required |

Compensation | Asset management fees, acquisition fees, and a share of profits (promote) | A share of profits and cash flow, often with a preferred return |

As you can see, the partnership is a symbiotic relationship. The GP provides the expertise and active management, while the LP provides the necessary capital, creating a powerful team built for success.

How a Real Estate Partnership Comes to Life

Ever wonder how a real estate partnership goes from a simple idea to a tangible, income-producing asset? It’s a journey that demystifies the whole process, turning an abstract legal structure into a concrete investment. It all starts long before a property is even identified, beginning with a General Partner’s strategic vision.

From that initial concept, a series of deliberate steps have to be hit. These milestones build the foundation, create the legal framework, and ultimately get capital deployed into a physical property. This methodical approach ensures everyone is protected and guided by a clear, legally binding roadmap from day one.

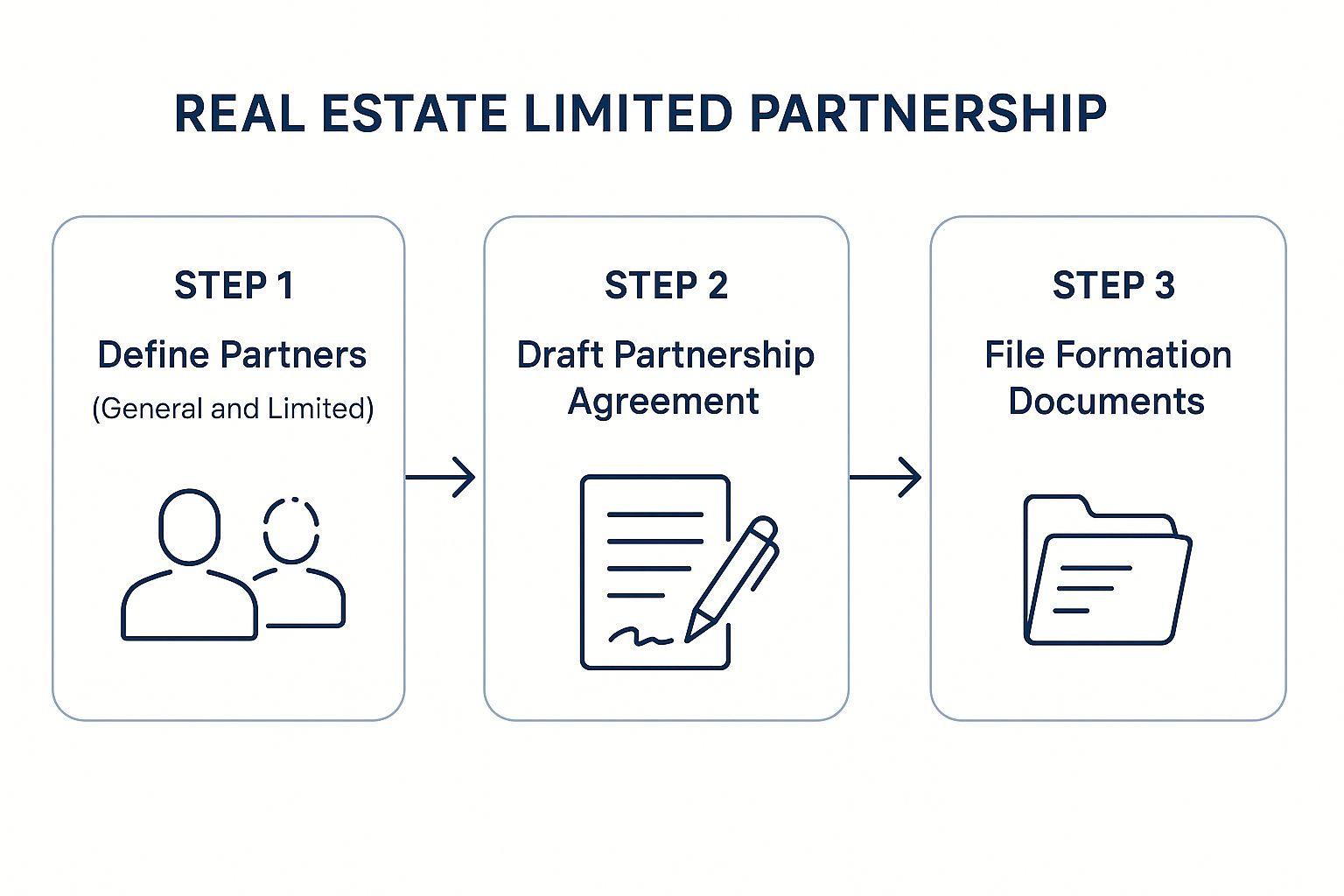

Laying the Legal Groundwork

The first real step is creating the legal entity that will actually own the asset. The GP will typically form a brand-new Limited Partnership (LP) or a Limited Liability Company (LLC) that’s taxed as a partnership. Think of this new entity as a special-purpose container, designed specifically for the target property to keep the accounting clean and shield it from any other assets or liabilities.

Next up, the GP works with their lawyers to draft the single most important document in the entire deal: the Limited Partnership Agreement (LPA). This agreement is basically the constitution for the investment. It spells out every critical detail, including:

The exact roles and responsibilities of the GP.

The rights and protections for the LPs.

The schedule for when investors need to contribute their capital.

The fee structure for the GP.

The specific mechanics of the distribution waterfall—how profits get paid out.

This document is the bedrock of trust and alignment for everyone involved.

Funding the Vision and Acquiring the Asset

With the legal structure in place, the GP shifts into fundraising mode. They put together a comprehensive investment summary or a Private Placement Memorandum (PPM). This is the playbook for the deal, outlining the business plan, financial projections, market analysis, and all the associated risks, which is then presented to potential Limited Partners.

Accredited investors who like what they see will sign a subscription agreement, which is their legal commitment to fund their piece of the deal. Once enough equity has been committed to satisfy the lender and cover the upfront costs, the deal heads to the closing table. The GP finalizes the loan, combines it with the LP equity, and officially buys the property, putting the title in the name of the newly formed partnership.

This infographic breaks down the core steps to formally get the partnership entity set up.

This streamlined process—defining roles, codifying the rules in the LPA, and filing the necessary legal paperwork—creates the official investment vehicle that holds the real estate.

From Operations to Exit

Once the property is acquired, the partnership moves into the operational phase. This is where the GP executes the business plan—maybe it’s renovating the property, leasing up vacant space, or bringing in better management to cut costs. Throughout this entire period, the GP is on the hook for providing regular, transparent reports to the LPs on how the property is performing.

The final stage is the exit. After hitting the goals laid out in the business plan, the GP will put the property on the market or look to refinance it.

Investor Takeaway: When a sale or refinance happens, the proceeds flow back into the partnership. That cash is then distributed to all the partners according to the waterfall structure defined back in the LPA, completing the investment lifecycle and (hopefully) delivering solid returns to the Limited Partners.

Weighing the Benefits and Risks for Investors

Every investment is a trade-off. You're constantly balancing potential rewards against the inherent risks, and a limited partnership in real estate is no different. The entire structure is built to give passive investors some incredible advantages, but those perks come with some very real limitations.

Getting a handle on both sides of this coin is absolutely essential. It’s the only way to know if this kind of investment lines up with your financial goals, what you're comfortable risking, and your long-term game plan. For investors looking to get away from the volatility of the stock market, the benefits can be a huge draw. But a smart investor always gives the downsides just as much attention.

The Upside for a Limited Partner

The advantages of coming in as an LP are pretty significant. They all circle back to efficiency, protection, and access to deals you otherwise couldn't touch.

Truly Passive Income Potential: Your job as an LP is simple: provide the capital. The General Partner takes care of everything else—from annoying tenant calls and leaky roofs to the complex accounting and big renovation projects. You get to reap the benefits of real estate cash flow without ever being a landlord.

Limited Liability Protection: This is the bedrock of the whole LP structure. Your financial risk is strictly capped at the amount of your investment. If the project hits a legal snag or runs into financial trouble, your personal assets are completely shielded from creditors. That's a level of protection you just don't get in a general partnership.

Access to Institutional-Grade Deals: Let's be real—most of us can't single-handedly fund a massive apartment complex or a high-tech data center. These deals require millions in equity. The limited partnership model is all about pooling capital, giving individual investors a seat at a table they could never get to on their own.

Professional Management and Expertise: You're not just buying a piece of a building; you're tapping into the GP's years of experience, market know-how, and industry connections. You're basically hiring a specialist whose own financial success is tied directly to yours through the profit-sharing agreement.

The Inherent Risks and Downsides

Now for the other side. It's just as important to have a clear-eyed view of the risks. These aren't necessarily deal-breakers, but you need to go into any deal with your eyes wide open.

A limited partnership in real estate is specifically designed to create certain risk and return profiles. For instance, LPs in apartment buildings have historically seen low vacancy rates, often under 5% in good markets, which helps drive income. Plus, the pass-through tax status means investors can use depreciation to offset that income. As a result, LPs in stable properties have seen average annual returns in the 8–12% range in recent years. You can dig deeper into US housing market trends from JPMorgan for more context.

Investor Takeaway: The risks here are fundamentally different from the stock market. You’re trading away daily liquidity and direct control in exchange for access to private deals with potentially higher, tax-advantaged returns managed by an expert.

Illiquidity of Capital: This isn't like selling a stock. Once your money is in, it's in for the long haul—often 3 to 7 years or more. There’s no active marketplace to sell your LP share, so you have to be comfortable with locking up your funds for the entire project lifecycle.

Lack of Direct Control: As a passive investor, you hand the reins over to the GP. While the partnership agreement gives you some protections and voting rights on major decisions, you can't tell them how to run the property day-to-day. You're a passenger, not the driver.

Reliance on the General Partner: Your investment's success lives and dies with the GP. Their performance, integrity, and expertise are everything. If they mismanage the asset or make a bad call, your returns will take the hit. This makes vetting the sponsor the single most important thing you'll do.

Fees and Promote Structures: The GP gets paid for their work through fees (like for acquiring the property or managing it) and a cut of the profits called the "promote." This is standard practice, but it will reduce your net returns. You absolutely have to understand the fee structure and the distribution waterfall to know what your take-home profit will actually look like.

Putting It All Together: A Deal Lens Example

Theory is great, but nothing makes the concept of a limited partnership in real estate click quite like seeing the numbers in action. Let's walk through a simplified deal to demystify the financial structure and show exactly how a sponsor’s success is directly tied to investor returns.

Imagine Stiltsville Capital (the General Partner) finds "The Sunbelt Lofts," an underperforming 100-unit apartment complex. The game plan is a classic value-add: buy the property, renovate the units, bring in better management, and bump the rents up to market rates over a three-year period.

The Capital Stack: How the Deal Is Funded

The all-in cost to acquire and renovate The Sunbelt Lofts is $10,000,000. The GP then assembles the financing—what we call the capital stack—by layering different sources of money to get the deal done.

Here’s what that looks like:

Senior Debt: $7,000,000 (or 70% of the cost) comes from a traditional bank loan. This is the safest piece of the puzzle and has the first claim on the property if anything goes wrong.

Limited Partner (LP) Equity: $2,700,000 is raised from our pool of passive investors who want in on the deal.

General Partner (GP) Equity: $300,000 is put in by the sponsor. This "skin in the game" is non-negotiable; it's what keeps everyone's interests perfectly aligned.

The total equity in the deal is $3,000,000 ($2.7M from LPs + $300k from the GP). This cash is what covers the down payment and pays for all the planned renovations.

The Distribution Waterfall: Following the Money

Fast forward three years. The GP has nailed the business plan and sells The Sunbelt Lofts for a cool $15,000,000. After paying back the $7,000,000 bank loan and covering transaction costs, we're left with a $5,000,000 profit on top of the original $3,000,000 in equity.

Now, it's time to pay everyone back. This is where the distribution waterfall takes over, dictating the exact order in which money flows back to the partners, all based on the rules laid out in the Limited Partnership Agreement.

Investor Takeaway: The waterfall is structured to protect LPs. It ensures they get their initial investment back, plus a preferred return, before the GP takes a significant cut of the profits.

Here’s how a simple waterfall plays out:

Return of Capital: The first $3,000,000 is returned to all equity partners. LPs get their $2.7M back, and the GP gets their $300k. Everyone is made whole first.

Preferred Return: Next, the LPs receive their 8% annual preferred return, which has been adding up over the three years. This hurdle guarantees LPs get a base-level return before the GP gets promoted.

GP Catch-Up: In some deals, the GP then gets a "catch-up" distribution, bringing their return up to a level proportionate to the final profit split.

The Promote Split: Once those hurdles are cleared, the remaining profit is split. A common structure is 70/30. This means the LPs get 70% of what's left, and the GP earns the remaining 30% as their "promote"—a performance fee for a job well done.

This example clearly shows how the limited partnership model creates a powerful alignment of interests. The GP only gets their big payday after the investors have gotten their capital back and earned a solid preferred return. It’s a win-win.

Your Due Diligence Checklist for Any Sponsor

When you invest as a Limited Partner, you’re putting a huge amount of trust in the General Partner. Your returns—your money—are directly tied to their skills, their integrity, and their ability to get the job done.

This is why digging into the sponsor's background isn't just a box to check; it’s the single most important part of your investment decision. Before you even think about wiring funds, you need to put on your detective hat. A great sponsor won't just tolerate your questions; they'll welcome them and give you clear, honest answers.

This checklist is your game plan for vetting any sponsor behind a limited partnership in real estate. It’s designed to help you get the clarity you need to invest with confidence.

Sponsor Track Record and Experience

A sponsor's past performance is the best crystal ball you have for predicting future results. You have to look past the slick marketing brochures and get into the nitty-gritty of their actual history.

Realized Deals: Ask them for a list of every deal they've ever taken full cycle and sold. How do the final numbers (the IRR and equity multiple) stack up against what they originally promised in their projections?

Performance Under Pressure: How did their properties hold up during the last major downturn, like 2008 or the 2020 pandemic? Did they ever lose investor money or fail to make a preferred return payment?

Relevant Experience: Does their track record actually match the deal they’re pitching now? If they've only ever done multifamily deals in Texas, you need to ask tough questions about a new office development project in Florida.

The Deal Itself and Underwriting

This is where you stress-test the sponsor's story. It’s easy to make a deal look amazing with rosy projections, but your job is to see if those assumptions are anchored in reality.

Investor Takeaway: A sponsor's underwriting is essentially them telling you a story about the future. Your job is to figure out if that story is a grounded, data-driven forecast or just a fairytale. A deep dive into their pro forma is absolutely non-negotiable.

Rent Growth: What are they assuming for rent growth year-over-year? How does that compare to what independent market reports from firms like CoStar or CBRE are saying for that specific neighborhood?

Exit Cap Rate: What capitalization rate are they assuming they’ll sell the property for in the future? A conservative sponsor will project an exit cap rate that is higher than the rate they're buying at, building in a cushion for market risk.

Contingency Budget: How much cash have they set aside for when things go wrong? For a value-add project, you want to see a contingency budget of at least 10-15% of the total renovation cost to cover surprises.

These questions are just the starting point. For a much more detailed playbook, check out our complete guide to commercial real estate due diligence to make sure you're asking everything you need to know.

Your Questions, Answered

When you're exploring the world of passive real estate, a few key questions always seem to pop up. Getting straight answers is the first step toward feeling confident enough to make a move. Let's tackle the practical questions we hear most often from family offices and accredited investors considering a real estate limited partnership.

What’s a Typical Minimum Investment to Get In?

This is usually the first thing people ask, and for good reason—it’s all about access. While there's no single magic number, getting into institutional-quality deals requires a serious commitment.

For private placements like the ones we offer at Stiltsville Capital, a typical minimum investment usually starts around $100,000 and can go up to $500,000 or more, depending on the scale and complexity of the deal. These thresholds ensure we’re bringing together a group of serious, accredited partners who are aligned on the long-term vision.

How Do Profits (and Losses) Actually Get Split Up?

We've talked about the distribution waterfall, but it’s a concept that’s worth hitting again. Profits and losses aren't just split down the middle; they follow a very specific, tiered structure that’s designed to put the Limited Partner first.

The bottom line: The entire structure is built to pay you, the LP, first. Before anyone else sees a big payday, you get your original capital back. Then, you receive your preferred return (think of it as a predetermined annual return). Only after those hurdles are cleared does the General Partner earn their larger share of the profits, known as the "promote." It’s a powerful way to make sure everyone's interests are perfectly aligned.

What Happens If the GP Makes a Bad Call?

This is a huge one. You're handing over the day-to-day control, so what’s your protection? It all comes down to the Limited Partnership Agreement (LPA).

This is the legal playbook that spells out exactly what the GP can and can't do. It covers things like "key man" events (what happens if a critical person on the GP team leaves?) and can even give LPs the right to vote out a GP for things like gross negligence or fraud. But honestly, your best defense is doing your homework on the sponsor’s track record and integrity before you ever sign on the dotted line.

Can I Just Sell My Share If I Need to?

In a word: no. An LP interest is not like a stock you can trade tomorrow. It's an illiquid investment.

There's no public market where you can just list your shares. To exit early, you’d need the GP’s approval and then have to find someone willing to buy your position, which can be a long and difficult process. Investors have to be ready to see their capital through for the entire project lifecycle, which is typically 3-10 years. That illiquidity is the trade-off for getting access to private, high-potential deals that are managed by pros.

At Stiltsville Capital, we believe that well-structured real assets can be a prudent, resilient component of a long-term wealth strategy. If you have more questions about how a limited partnership could fit into your portfolio, we invite you to schedule a confidential call to discuss your goals.

Information presented is for educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy securities. Any offering is made only through definitive offering documents (e.g., private placement memorandum, subscription agreement) and is available solely to investors who meet applicable suitability standards, including “Accredited Investor” status under Rule 501 of Regulation D. Investments in private real estate involve risk, including loss of capital, illiquidity, and no guarantee of distributions. Past performance is not indicative of future results. Verification of accredited status is required for participation in Rule 506(c) offerings.

Comments