Unlocking Value with the Tax Depreciation Shield

- Ryan McDowell

- Aug 4, 2025

- 11 min read

Reading Time: 7 min | Good for: Novice (A), Informed (B)

TL;DR: Key Investor Takeaways

The Shield Defined: The tax depreciation shield is a powerful, IRS-approved strategy that allows real estate investors to deduct a portion of a property's cost from their taxable income each year, creating a "paper loss" that generates real cash savings.

Why It Matters: This non-cash expense directly lowers your tax bill, increasing after-tax cash flow and boosting key return metrics like cash-on-cash return and IRR. It's a primary reason sophisticated investors allocate capital to real estate.

Supercharging Returns: Strategies like cost segregation and bonus depreciation can dramatically accelerate these deductions, pulling massive tax savings into the early years of an investment and freeing up significant capital.

Investor Action: Partner with a sponsor who proactively uses these tax tools. Ask them how they approach cost segregation and depreciation to ensure your investment is fully optimized from a tax perspective.

What Is a Tax Depreciation Shield and Why Does It Matter?

What if you could turn a profitable real estate investment into a "paper loss" that actually saves you real money on your taxes? That's not a fantasy—it’s the power of the tax depreciation shield.

For any serious real estate investor, the tax depreciation shield isn't just another line item on a spreadsheet. It’s a core component of building wealth. In fact, it's one of the biggest tax advantages in commercial real estate, letting you shelter income that would otherwise get hit with high tax rates.

Think of it as a non-cash expense that generates very real cash savings.

The idea behind it is simple. The IRS understands that buildings, like any physical asset, wear out over time. To account for this natural decline, they let property owners deduct a slice of the property's cost basis each year. Even if your beautifully maintained apartment building is going up in market value, the tax code still grants you this "paper loss." This deduction then chips away at your net taxable income.

The Real-World Impact on Your Bottom Line

This isn't just theory; it has a direct and tangible effect on your annual returns. A lower taxable income means you write a smaller check to the government, leaving more cash in your portfolio at the end of the year. That extra cash can then be reinvested, used for other deals, or distributed back to you, accelerating your wealth-building journey.

The benefits are straightforward and powerful:

Increased After-Tax Cash Flow: By shielding rental income from taxes, you simply keep more of what your property earns.

Enhanced Investor Returns: A lighter tax load directly boosts key metrics like your cash-on-cash return and internal rate of return (IRR).

Improved Capital Efficiency: The cash you save can be put back to work, fueling faster growth or strengthening your investment's financial footing.

Novice Lens: Why It MattersThe tax depreciation shield is what transforms a profitable real estate deal into an incredibly tax-efficient one. It’s a major reason why high-net-worth individuals and family offices pour so much capital into real estate—the tax savings can be just as valuable as the rent checks themselves.

Depreciation Concepts for Real Estate Investors

This table breaks down the core components of real estate depreciation, comparing different methods and highlighting their primary benefits for investors.

Concept | What It Means for You | Typical Schedule (U.S.) | Primary Investor Benefit |

|---|---|---|---|

Cost Basis | The total amount you paid for the property, including acquisition costs, minus the value of the land. | N/A | The starting point for all depreciation calculations. |

Straight-Line Depreciation | Deducting an equal amount of the property's value each year over its "useful life." | 27.5 years (residential)39 years (commercial) | Predictable, steady tax deductions year after year. |

Cost Segregation | An engineering study that separates property components (e.g., carpet, appliances) into shorter depreciation schedules. | 5, 7, or 15 years for certain components. | Accelerates depreciation deductions into the early years of ownership for a massive upfront tax benefit. |

Bonus Depreciation | An incentive that allows you to deduct a large percentage (currently 80% in 2024) of the cost of certain assets in the first year. | Varies by year based on tax law. | Maximizes tax savings immediately, freeing up significant capital. |

Understanding these different layers of depreciation is the first step toward building a truly optimized real estate portfolio. Working with a sponsor who knows how to pull these levers effectively ensures your investments are working as hard as possible for you. To go even deeper, check out our **ultimate guide to real estate tax benefits**, which covers more strategies every investor should know.

How the Tax Depreciation Shield Creates Real Value

Let's move past the theory and talk about what this means for your bottom line. The tax depreciation shield is one of the most powerful tools in real estate for boosting after-tax returns, and it works its magic even while your property is gaining market value. It’s a bit counterintuitive, but the IRS lets you deduct a portion of your property’s cost basis over a set period, creating a "paper loss" that directly lowers your tax bill.

The concept is simple but incredibly effective. The depreciation you claim is a non-cash expense, meaning you didn't actually spend that money this year. Yet, it shields your very real cash income from being taxed. This directly boosts your after-tax cash flow.

The Core Calculation for Tax Savings

At its heart, the value of this shield is a straightforward formula every investor should get comfortable with. It puts a hard number on the cash savings you get from this non-cash expense.

Tax Savings = Annual Depreciation Expense × Your Marginal Tax Rate

So, if your property gives you a $50,000 depreciation deduction and you're in the 37% federal tax bracket, your direct federal tax savings for the year is $18,500. That’s real cash that stays with you instead of going to the IRS, all thanks to an on-paper deduction. This powerful mechanism allows investors to lower their taxable income through depreciation, which represents the wear and tear on an asset. As the Corporate Finance Institute notes, this non-cash charge provides a recurring tax benefit.

A Practical Walkthrough of the Shield in Action

Let's ground this with a clear, practical example to see how the numbers play out for an individual investor.

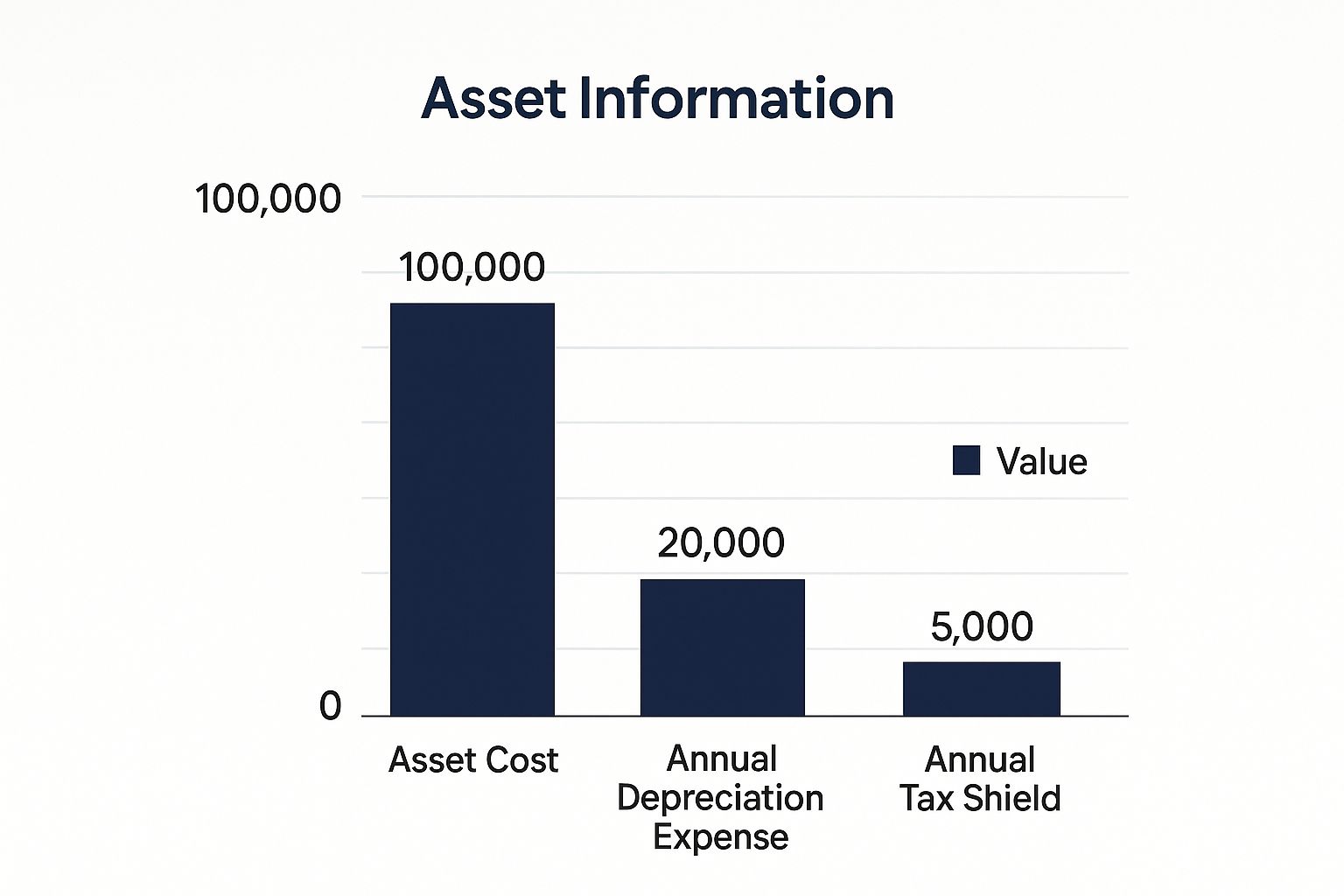

Imagine you and a few partners purchase a commercial office building. We'll use simple numbers to make it crystal clear.

Purchase Price: $5,000,000

Land Value (Non-Depreciable): $1,100,000

Improvement Value (Depreciable Basis): $3,900,000

Under U.S. tax law, commercial properties are depreciated over 39 years using the straight-line method.

Step 1: Calculate Your Annual DepreciationFirst, we figure out the yearly amount you can deduct.

Calculation: $3,900,000 (Improvement Value) / 39 years

Annual Depreciation Expense: $100,000

This $100,000 is the non-cash expense you can write off each year to lower the property's taxable income.

Step 2: Apply the Shield to Your Real IncomeNow, let's watch how this impacts your tax bill. Let's say the property is performing well and generating positive cash flow.

Net Operating Income (NOI): $250,000

Depreciation Deduction: -$100,000

Taxable Income: $150,000

See what happened? Without the tax depreciation shield, your entire $250,000 of income would be taxable. By applying the depreciation, you've effectively shielded $100,000 of real income from taxes.

Step 3: Count Your Cash SavingsThe final step is turning that shielded income into actual cash savings. We'll assume a combined federal and state marginal tax rate of 40% for the investors.

Tax Savings Calculation: $100,000 (Shielded Income) × 40% (Tax Rate)

Annual Tax Savings: $40,000

In this scenario, the tax depreciation shield puts a cool $40,000 back into the investors' pockets every single year. This is cash that would have otherwise been handed over in taxes, proving just how critical depreciation is for boosting an investment's true financial performance. It’s not just an accounting trick; it’s a foundational piece of any well-structured real estate investment.

Supercharge Your Returns with Cost Segregation

While standard depreciation is a solid, reliable tax benefit, savvy investors know there's a way to put the tax depreciation shield on steroids. The secret to unlocking this next level of value is a strategy called cost segregation.

This isn't just some accounting trick. Cost segregation is a detailed, engineering-based study that breaks down a commercial property into its individual components. Instead of treating the whole building as one big asset depreciating over 39 years (or 27.5 for residential), this analysis identifies specific parts you can write off much, much faster.

Unpacking the Power of Faster Write-Offs

A cost segregation study essentially sorts a property’s assets into different buckets, each with its own depreciation timeline as defined by the IRS. This allows you to pull a huge chunk of your depreciation deductions into the first few years of ownership, creating a massive upfront tax shield.

Think about everything in a commercial building that isn't part of the core structure. This can include things like:

5-Year Property: Carpeting, specific types of lighting, and cabinetry.

7-Year Property: Office furniture and appliances.

15-Year Property: Land improvements like paving, landscaping, and exterior signs.

By reclassifying a slice of the building's cost into these shorter-term categories, you can claim much larger depreciation expenses in years one through five. This front-loading of deductions slashes your taxable income right when you need it most.

The Bonus Depreciation Amplifier

The perks of cost segregation get even better when you pair it with a powerful tool in the tax code: bonus depreciation. This rule lets investors deduct a huge percentage—currently 80% in 2024—of an asset's cost in the very first year.

Any asset with a lifespan of 20 years or less usually qualifies. That means all the 5, 7, and 15-year property you just identified in your cost segregation study can potentially be written off immediately.

Investor Take: Imagine identifying 25% of a $10 million property's value as short-life assets. That's $2.5 million in components. With 80% bonus depreciation, you could generate a staggering $2 million tax deduction in the first year alone—on top of the regular depreciation for the rest of the building.

This one-two punch of cost segregation and bonus depreciation is a true cornerstone of any advanced real estate tax strategy. Strategically deferring taxes is also a key companion to other powerful strategies, which you can learn about in our detailed **guide to the 1031 Exchange**. At the end of the day, cost segregation is a numbers game that proves how smart tax planning can push your investment returns far beyond the norm.

Deal Lens: A Value-Add Multifamily Acquisition

Theory is great, but let's see how these tax strategies actually perform in the wild. To really show the financial punch of a well-executed depreciation strategy, we'll walk through a hypothetical value-add multifamily deal. This is exactly where a sharp sponsor can create serious value that goes way beyond simple rent increases.

Picture this: Stiltsville Capital acquires an underperforming 100-unit apartment complex for $10 million. The property is in a solid location but is tired. Our plan involves a capital improvement program to modernize units, allowing us to push rents to market rates.

The real key, though, is how we handle the tax side. Instead of just taking the standard depreciation schedule, we immediately commission a cost segregation study right after closing. This engineering-based analysis is the linchpin of our strategy to maximize the tax depreciation shield for our investors.

Breaking Down the Numbers

A cost segregation study meticulously dissects the $10 million purchase price (after backing out the land value) and reallocates chunks of it to shorter-lived asset classes.

Let's say the study finds that 25% of the building's cost basis—or $2.5 million—can be reclassified as 5-year and 15-year property (new appliances, flooring, cabinetry, paving, etc.). The other 75% ($7.5 million) remains as 27.5-year residential property. Under 2024 tax rules allowing for 80% bonus depreciation, we can immediately write off a massive portion of those reclassified assets. This creates an enormous paper loss in Year 1, dramatically shielding our investors’ distributions from taxes.

Investor Take: A proactive sponsor doesn't just manage a property; they use the tax code as a tool to actively create value. By front-loading deductions through cost segregation, we generate substantial tax savings in the early years. This directly boosts cash-on-cash returns and the project's overall Internal Rate of Return (IRR).

Comparing the Scenarios

The difference between a standard approach and an accelerated one is night and day. The table below models the dramatic impact on after-tax cash flow for our investors. It’s a simplified look, but it nails the core concept.

Depreciation Impact on a $10M Multifamily Asset (Illustrative)

Metric | Scenario A: Straight-Line | Scenario B: Accelerated (Cost Seg) | Impact |

|---|---|---|---|

Year 1 NOI | $500,000 | $500,000 | Same operating performance |

Year 1 Depreciation | ~$272,727 | ~$2,272,727 | 8.3x more depreciation |

Year 1 Taxable Income | $227,273 | ($1,772,727) | Creates a massive paper loss |

Taxes Due (37% rate) | $84,091 | $0 | $84,091 in direct tax savings |

After-Tax Cash Flow | $415,909 | $500,000 | 20% higher return for investors |

As you can see, the accelerated strategy completely wiped out the tax liability in the first year. This move put over $84,000 in tax savings directly back into our investors' pockets, significantly boosting their returns right out of the gate. This is the tangible power of using the tax depreciation shield to its absolute fullest potential.

Checklist: Questions to Ask a Sponsor About Depreciation

When evaluating a real estate deal, don't just focus on the property. Dig into the sponsor's tax strategy. Here are the questions you should be asking:

Do you perform cost segregation studies? If so, when? The answer should be "Yes, immediately after acquisition."

What percentage of the cost basis do you typically reclassify to shorter-lived assets? This shows their experience and aggressiveness.

How do you handle the land value allocation? A savvy sponsor will have a defensible strategy to maximize the depreciable building value.

What is the plan for depreciation recapture upon sale? Look for proficiency with 1031 exchanges to defer taxes.

How does the phase-out of bonus depreciation affect your underwriting for this deal? Their models should reflect the current 80% rate and its future decline.

Can you show me how depreciation impacts my projected after-tax returns in the model? They should be able to clearly walk you through the numbers.

Risk & Mitigation

Every investment carries risk. A disciplined sponsor identifies them upfront and has a clear plan to mitigate them.

Risk: Tax Law Changes. Congress can alter depreciation rules, reducing the shield's value. * Mitigation: We stay abreast of legislative changes and model multiple tax scenarios. The fundamental value of depreciation is a long-standing principle of tax law, providing a durable, if sometimes changing, benefit.

Risk: Aggressive Cost Segregation. An unsupported allocation could be challenged by the IRS. * Mitigation: We only use reputable, third-party engineering firms to conduct studies, creating a defensible, audit-ready report.

Risk: Depreciation Recapture. Selling a property can trigger a large tax bill on the accumulated depreciation. * Mitigation: We build our strategy around the 1031 Exchange, allowing investors to defer recapture taxes by rolling proceeds into a new deal, preserving capital for continued growth.

Understanding these dynamics is essential when **navigating the challenges confronting commercial real estate investors** today.

Final Thoughts: The Shield as a Core Strategy

The tax depreciation shield isn't just a minor perk; it's a foundational pillar of successful real estate investing. By converting a non-cash expense into hard-dollar tax savings, it directly enhances your annual returns and accelerates wealth creation.

However, unlocking its full potential requires more than just owning a property. It demands a proactive, sophisticated sponsor who understands how to use tools like cost segregation and bonus depreciation to their maximum effect. A well-structured real estate investment, anchored by a disciplined tax strategy, can be a prudent and resilient component of your long-term wealth plan.

At Stiltsville Capital, we believe that optimizing the tax implications of an investment is as important as optimizing its operations. If you're ready to see how these sophisticated strategies can be applied to your portfolio, we invite you to explore a partnership with us.

Information presented is for educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy securities. Any offering is made only through definitive offering documents (e.g., private placement memorandum, subscription agreement) and is available solely to investors who meet applicable suitability standards, including “Accredited Investor” status under Rule 501 of Regulation D. Investments in private real estate involve risk, including loss of capital, illiquidity, and no guarantee of distributions. Past performance is not indicative of future results.

Comments