How to Leverage Real Estate: A Guide to Amplifying Investor Returns

- Ryan McDowell

- Dec 9, 2025

- 11 min read

Reading Time: 8 min | Good for: Novice Investors (A), Family Offices (B)

TL;DR: Key Takeaways on Leveraging Real Estate

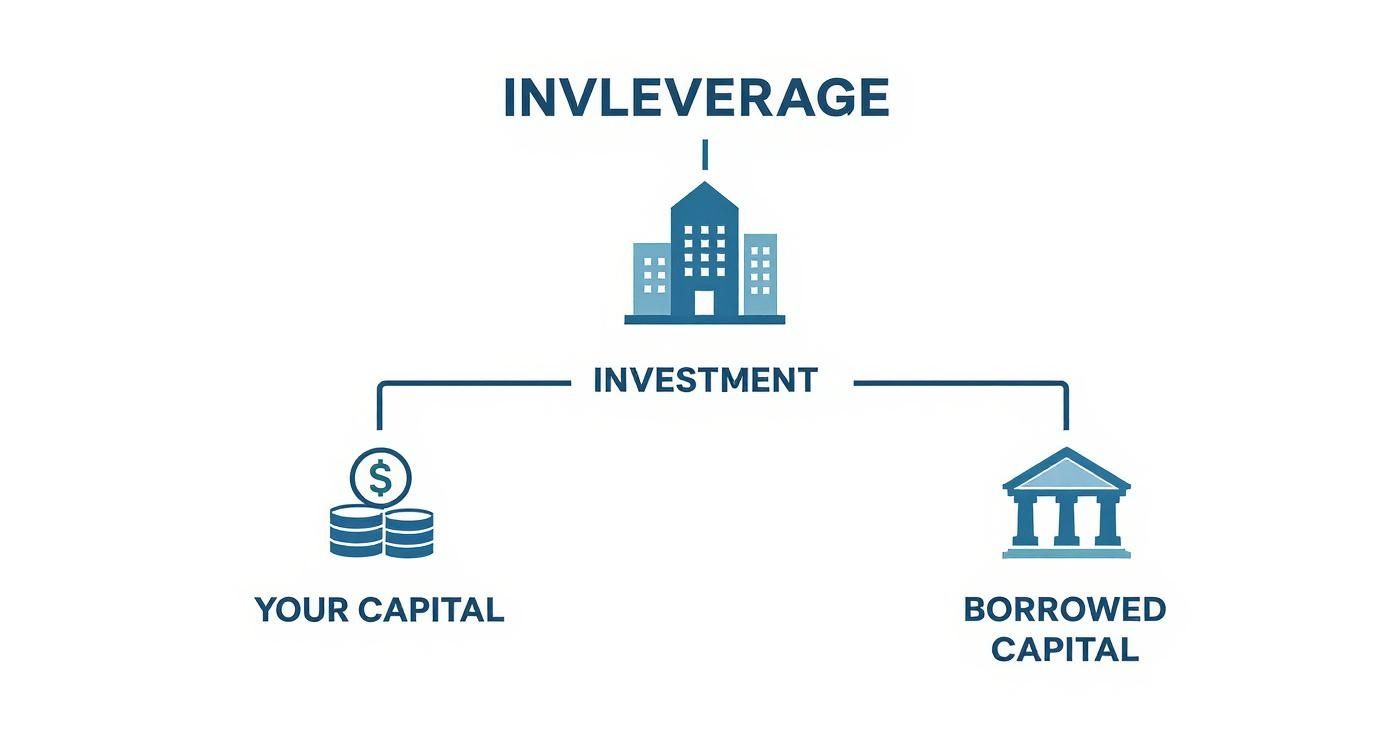

What It Is: To leverage real estate means using borrowed capital (debt) to buy a property, allowing you to control a large asset with a smaller amount of your own money.

Why It Matters: This strategy amplifies your potential returns on equity. A small increase in property value can translate into a much larger gain on your invested capital.

The Trade-Off: Leverage is a double-edged sword. It magnifies gains but also magnifies losses with the same force, making disciplined underwriting non-negotiable.

Who Should Care: For family offices and high-net-worth investors, understanding how a sponsor uses leverage is critical to evaluating the risk and reward of any passive real estate deal.

For seasoned investors, family offices, and institutions, leverage isn't just a way to finance a deal; it's the engine that drives wealth creation in commercial real estate.

Think about it: with leverage, an investor can take $3 million of their own capital to control a $10 million property. This immediately magnifies the investment's upside and completely changes its return profile. Instead of sinking all your capital into one unleveraged property, you can spread that same equity across several properties, building a more diversified portfolio. To really get a feel for how leverage juices potential gains, it’s worth understanding the nuts and bolts of how to calculate ROI.

Market Why-Now: The Shifting Debt Landscape

A sharp understanding of leverage is more critical than ever. As traditional bank lending has become more conservative, a significant opportunity has emerged.

Market Signal Box* The Data: Non-bank lenders, like private credit funds, now account for nearly half of all commercial real estate debt origination in the U.S., a significant increase from just a decade ago, according to data from CBRE (as of late 2023).* Interpretation: This structural shift means sponsors with deep relationships in the private credit market have a distinct advantage in sourcing flexible, customized financing.* Investor Take: Partnering with a sponsor who can navigate this new landscape is key. Access to the right debt at the right terms can be the deciding factor in a deal's success.

This creates a window of opportunity for passive investors. For those who know how to navigate this landscape, the returns can be exceptional. The core benefits are clear:

Amplified Returns: A small increase in a property’s value can create a much larger return on your actual equity investment.

Increased Deal Capacity: Your capital goes further, allowing you to invest in multiple assets and diversify risk.

Tax Advantages: The interest paid on mortgage debt is generally tax-deductible, which can provide a healthy boost to net cash flow.

Leverage is what separates modest real estate holdings from institutional-grade portfolios. It’s the disciplined use of debt that unlocks an investment's full power, turning a good property into a standout performer in a long-term wealth strategy.

Understanding The Mechanics Of The Capital Stack

To master leverage, you must understand how a real estate deal is structured. We call this the capital stack—think of it as a layered cake where each layer represents a different source of money with a specific risk profile and claim on profits.

This hierarchy determines who gets paid first when things go well and, more importantly, who takes the first loss if they don't. Knowing this pecking order is what separates a solid deal from one built on a shaky foundation.

You’re combining your own funds with borrowed capital to control a much larger, more valuable asset than you could on your own.

Novice Lens: What is the Capital Stack?Think of it like a line for repayment. The people at the front of the line (senior debt) have the least risk and get paid first. The people at the back of the line (common equity) have the most risk but also get the biggest potential reward if the investment is a home run.

Senior Debt: The Foundation

At the bottom of the stack is the most secure layer: senior debt. This is the primary mortgage, usually from a bank. Because senior debt holders are first in line to be repaid in a foreclosure, they have the lowest risk.

Risk Level: Lowest.

Return: Fixed interest payments. Lenders do not share in the property's appreciation.

Key Metric: Lenders focus on the Loan-to-Value (LTV) ratio, often capping it at 65-75% for a stable property to ensure there's a protective cushion of equity below them.

Mezzanine Debt and Preferred Equity: The Middle Layers

Moving up, you find more creative—and more expensive—forms of capital like mezzanine debt and preferred equity. These fill the gap between the senior loan and the investors' equity. They are second in line to get paid but come before the common equity partners. This financing often carries higher interest rates and is key to funding value-add or development projects. If you want to go deeper, check out our detailed guide to mezzanine financing.

Common Equity: The Top Slice

At the very top is common equity. This is the "skin in the game"—the money put up by the deal sponsor (the General Partner, or GP) and passive investors (the Limited Partners, or LPs). It's the riskiest position because equity holders are the last to get paid.

But with high risk comes the highest potential reward. After all debt is paid, common equity holders receive everything that's left, which is where the magic of leverage creates outsized returns.

Risk Level: Highest.

Return: Highest potential, from both cash flow and the final sale. It has uncapped upside.

Key Concept: This is the "first-loss" capital—the investment that absorbs losses first.

How Leverage Magnifies Returns and Risks

Leverage is the fulcrum of real estate investing. Think of it like a see-saw: a small force on your end—your equity—can lift a much heavier object on the other—the property’s total value. This amplification is how fortunes are made, but it's also where discipline becomes non-negotiable.

Leverage works because you borrow capital at one cost (the interest rate) and invest it in an asset generating a higher return. That "spread" flows directly to you, the equity investor. Of course, this is a double-edged sword: it magnifies gains when a property performs well and magnifies losses with the exact same force when it underperforms.

Deal Lens Example: Leverage in Action

Let's walk through a simplified example for a value-add multifamily property acquired for $10 million.

Scenario 1: The All-Cash Purchase (No Leverage)

You buy the property using $10 million of equity. After improvements, you increase the Net Operating Income (NOI).

Your Initial Equity: $10,000,000

Annual Net Operating Income (NOI): $600,000

Cash-on-Cash Return: ($600,000 / $10,000,000) = 6.0%

After five years, you sell the property for $12 million. Your profit is a respectable $2 million.

Scenario 2: The Prudent Leveraged Purchase

Now, let's use a common institutional structure: 70% debt and 30% equity.

Your Initial Equity: $3,000,000

Loan Amount (70% LTV): $7,000,000

Annual Debt Service (at 5% interest): $350,000

The property still generates $600,000 in NOI. But now, we pay the lender first.

Cash Flow After Debt: ($600,000 NOI - $350,000 Debt Service) = $250,000

Cash-on-Cash Return: ($250,000 / $3,000,000) = 8.3%

Your cash-on-cash return jumps significantly. When you sell for $12 million, you repay the $7 million loan, leaving $5 million. Since your initial equity was $3 million, your profit is the same $2 million.

Investor Takeaway: In both cases, the deal made a $2 million profit. But in the leveraged scenario, you achieved that same profit with only $3 million of your own capital at risk, not $10 million. This dramatically increases your return on equity and frees up your capital for other investments.

Illustrative Example: Leverage Impact on Investor Returns

This table shows how outcomes change based on the financing structure.

Metric | All-Cash Purchase (No Leverage) | Leveraged Purchase (70% LTV) |

|---|---|---|

Purchase Price | $10,000,000 | $10,000,000 |

Investor Equity | $10,000,000 | $3,000,000 |

Loan Amount | $0 | $7,000,000 |

Sale Price (Gain Scenario) | $12,000,000 | $12,000,000 |

Total Profit (Gain Scenario) | $2,000,000 | $2,000,000 |

Return on Equity (Gain) | 20% ($2M / $10M) | 66.7% ($2M / $3M) |

Sale Price (Loss Scenario) | $9,000,000 | $9,000,000 |

Total Loss (Loss Scenario) | ($1,000,000) | ($1,000,000) |

Return on Equity (Loss) | -10% (-$1M / $10M) | -33.3% (-$1M / $3M) |

The table makes it clear: leverage acts as a multiplier. But just as a 20% unleveraged gain became a 66.7% leveraged gain, a 10% unleveraged loss became a much more painful 33.3% loss. This is the risk that must be respected and rigorously underwritten. As you can discover more insights about global private markets at McKinsey.com, an experienced sponsor never forgets these lessons, always balancing the pursuit of amplified returns with robust downside protection.

Strategic Approaches to Leveraging Your Portfolio

Successful real estate investing means thinking like a portfolio manager. A sophisticated investor doesn’t just ask, "How much can I borrow?" They ask, "What is the optimal leverage for this asset and my overall goals?" The answer always depends on the strategy and risk profile.

A fully leased office building with long-term tenants has predictable cash flow, so lenders are comfortable with higher leverage—perhaps 65-75% LTV. In contrast, a ground-up development project is entirely speculative. Lenders will be far more cautious, often capping loans at 50-60% of the project cost.

Positive, Negative, and Neutral Leverage

The test of whether debt is helping or hurting comes down to the relationship between the property’s capitalization (cap) rate and the loan's interest rate.

Positive Leverage: The goal. The property’s cap rate is higher than your loan's interest rate. Every borrowed dollar earns more than it costs.

Negative Leverage: The danger zone. The interest rate is higher than the cap rate. Borrowing money actually reduces your return.

Neutral Leverage: The cap rate and interest rate are the same. Debt neither helps nor hurts your equity return.

Sourcing The Right Capital Partner

Today’s financing world looks very different than it did a decade ago. As traditional banks have tightened their belts, an opportunity has opened up for private credit funds and alternative lenders to fill the gap.

An experienced sponsor knows how to navigate this complex market to find debt that fits the business plan. For a deeper look at the mechanics, it’s worth reviewing resources on commercial real estate lending practices. Ultimately, understanding the full spectrum of financing options is what separates the pros. Our own guide to commercial real estate financing options for investors can provide more context.

Identifying and Mitigating Key Leverage Risks

Confidence with leverage comes from understanding its risks inside and out. A seasoned sponsor spends as much time stress-testing what could go wrong as modeling what could go right. This realistic perspective separates sustainable wealth creation from a speculative gamble.

Risk & Mitigation Table

Every leveraged deal comes with a core set of risks. The best sponsors have a playbook ready for each one.

Risk: Interest Rate Volatility * Mitigation: For floating-rate loans, sponsors purchase interest rate caps or execute swaps. These act as insurance policies, putting a ceiling on the rate and protecting cash flow from market volatility.

Risk: Refinancing Hurdles * Mitigation: This is managed from day one with conservative underwriting. Sponsors project future interest rates and exit cap rates with plenty of cushion and build strong relationships with a wide network of lenders.

Risk: Default and Foreclosure * Mitigation: Top-tier sponsors insist on a healthy Debt Service Coverage Ratio (DSCR), creating a buffer between the property's income and its debt. They also set aside capital reserves to cover unexpected vacancies or repairs.

Global interest rate trends are a huge factor in how investors use leverage. To get a deeper sense of these global dynamics, you can read the full global real estate outlook from DWS.com.

Recourse vs. Non-Recourse Loans: A Critical Distinction

For any passive investor, one of the most important lines of defense is the type of loan the sponsor uses.

Recourse Loan: If the deal fails, the lender can come after the borrower's other personal or business assets—not just the property.Non-Recourse Loan: The lender's claim is limited only to the property used as collateral. Your other assets are safely walled off.

Virtually all institutional-quality commercial real estate is financed with non-recourse debt. For high-net-worth individuals and family offices, this is non-negotiable. It isolates risk to a single deal and protects an investor's broader wealth.

Actionable Investor Checklist: Questions to Ask a Sponsor

When evaluating a deal, use these questions to probe a sponsor’s approach to leverage:

Is the debt recourse or non-recourse to the limited partners?

Is the interest rate fixed or floating? If floating, what is your hedging strategy?

What are your underwriting assumptions for exit cap rates and interest rates at refinance?

What is the target Debt Service Coverage Ratio (DSCR) for this property?

What do your capital reserve policies look like?

Can you walk me through your downside-scenario stress tests for this deal?

Partnering With Experts for Smart Leverage

Leverage is a professional's tool. Wielding it effectively takes deep market knowledge, sophisticated financing relationships, and a rigorous approach to risk that only comes from years in the trenches.

The good news is you don't have to become a full-time real estate operator to get the benefits of this powerful strategy. For high-net-worth individuals and family offices, the goal is to capture the upside of leverage without the immense operational burden.

The Sponsor's Role in Managing Leverage

Partnering with a seasoned sponsor is the most effective way to do this. An expert team acts as your fiduciary, navigating the complexities of debt markets on your behalf. This partnership provides several advantages:

Institutional Deal Flow: Access to off-market opportunities with strong fundamentals that can justify the use of leverage.

Superior Financing Relationships: A good sponsor secures favorable, non-recourse loan terms from a network of trusted lenders.

Proactive Risk Mitigation: They implement sophisticated hedging strategies and maintain robust capital reserves to protect the investment.

This strategic alignment allows you, the investor, to focus on your bigger-picture wealth objectives while your capital is put to work in meticulously underwritten assets. It transforms leverage from a source of operational complexity into a seamless component of your portfolio. For investors who want to dig deeper into this model, our guide to investing with a private equity real estate firm offers a more detailed perspective.

Real Estate Leverage FAQs

What is a good Loan-to-Value (LTV) ratio?

There’s no single magic number. For a stable, core asset with predictable cash flow, 65-75% LTV is common. For a riskier development or opportunistic deal, a more conservative 50-60% LTV is typical. A smart sponsor balances boosting returns with maintaining a healthy cushion against a downturn, ensuring the property’s income can easily cover debt payments.

What is the difference between recourse and non-recourse debt?

This is crucial. With a recourse loan, a lender can pursue a borrower’s other personal or business assets if the deal fails. With a non-recourse loan, the lender's claim is strictly limited to the property they financed. Institutional-quality deals almost always use non-recourse debt to insulate investors' personal wealth from the risk of any single investment.

How do rising interest rates affect leveraged real estate?

Rising rates can impact a leveraged deal in two main ways. First, for floating-rate loans, interest payments increase, which reduces cash flow to investors. Sponsors mitigate this with tools like interest rate caps. Second, higher rates make refinancing more expensive and can push market cap rates up, which may reduce a property's sale value. Experienced sponsors stress-test their models for rising rate scenarios from day one.

At Stiltsville Capital, we believe well-structured real estate assets can be a prudent, resilient component of a long-term wealth strategy. Our entire approach is built on a disciplined use of leverage, focusing on non-recourse debt and obsessive risk management to protect and grow investor capital. To see how our strategies can fit into your own portfolio goals, schedule a confidential call with our team.

Information presented is for educational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy securities. Any offering is made only through definitive offering documents (e.g., private placement memorandum, subscription agreement) and is available solely to investors who meet applicable suitability standards, including “Accredited Investor” status under Rule 501 of Regulation D. Investments in private real estate involve risk, including loss of capital, illiquidity, and no guarantee of distributions. Past performance is not indicative of future results.

Comments